January Portfolio Review

An overview of Idea Hive portfolio positions

With January in the books, I am sharing the monthly portfolio review. This post provides an overview of the Idea Hive portfolio, including key information on each position, such as elevator pitches and performance to date. The article also covers recent updates on each portfolio name and their impact on the underlying investment theses. The aim of this post is to quickly recap the latest developments for each idea and highlight why the portfolio names continue to present attractive investment opportunities.

Let’s dive right in.

Portfolio Review

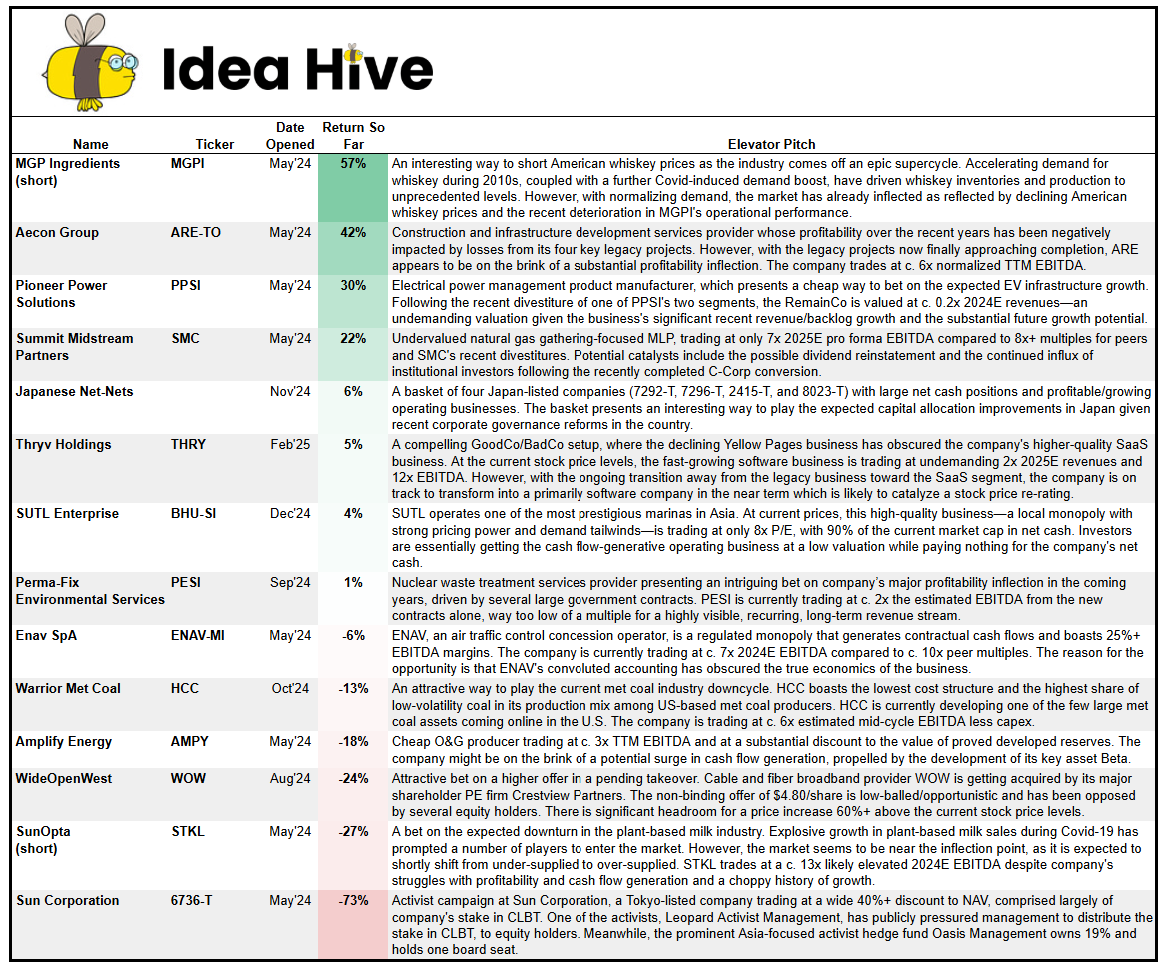

Here’s the Idea Hive portfolio as of February 5:

Over the past month, I introduced a new idea to my portfolio, THRY, and closed one position, MON-V. As for the other portfolio ideas, several important developments took place in January, most notably AMPY’s large acquisition and ARE securing a major contract.

To quickly touch on portfolio performance, the same three positions remain the top performers: MGPI short (+57%), ARE-TO (+42%), and PPSI (+30%). On the negative side, I would mention 6736-T, currently down 73%. This significant negative return is explained by the divergence in stock price movements between CLBT (up 18% since the beginning of January) and 6736-T (down 1%), along with the high sensitivity of returns for hedged positions to CLBT share price movements (e.g., a 15% decline in CLBT would imply a break-even for my position).

Which portfolio names are the most actionable right now? I’d highlight ARE-TO and WOW as my highest-priority ideas. In my view, both setups have the strongest likelihood of near-term catalysts materializing, including a potential definitive buyout agreement for WOW and an imminent several legacy project completion for ARE.

Portfolio Idea Updates

Below is a list of recent updates and thoughts on active and recently closed Idea Hive portfolio positions.

MGP Ingredients (MGPI)

There have been no material updates from MGPI over the last month, though I would highlight this WSJ piece on the American whiskey industry. The article confirms ongoing industry challenges, with sales volumes down 4% through three quarters of 2024, the largest decline in a decade. While MGPI's share price has continued to drift lower over the last month and the stock is now down over 50% since the write-up levels, I continue to believe there is substantial further upside for short positions, as the company is currently trading at multiples above its replacement cost. A potential re-rating from the current enterprise value of $1bn to the tangible book value of $0.3bn—still above where MGPI traded before the industry upcycle—would imply a potential downside of c. 70%. I will be waiting for MGPI’s FY24 results, likely to be released later this month, to assess the company’s operational performance in Q4 and any commentary from management on the broader American whiskey demand and supply dynamics.

Aecon Group (ARE-TO)

Highlighting several developments at ARE. During January, the company announced 1) that a JV, of which ARE is a part, was awarded a contract for the refurbishment of a nuclear generating station, and 2) that one of the design-build model projects has reached the commercial/implementation phase. These are positive developments, as they will significantly boost ARE’s backlog, from C$6bn as of Sep’24 to around C$10bn as of Q1’25, while also increasing the company’s exposure to the nuclear end-market. Despite the positive announcements, ARE’s share price has drifted lower recently, likely partially driven by the potential US tariffs on Canada, which might have a negative impact on ARE’s fixed-cost projects and broader construction project demand going forward. Nonetheless, considering the recent 30-day tariff implementation pause, I think that at this point, it is too early to determine if the levies will be implemented, and, if so, what the impact on ARE might be. The stock remains cheap, trading at 5x TTM normalized EBITDA, significantly below the 10x+ multiples at which its peers trade. A near-term catalyst that might help close the valuation gap is the anticipated completion of the legacy projects. Two of the three remaining projects, Finch LRT and Eglinton LRT, are expected to be completed this quarter, which will leave the company with the sole remaining Gordie Howe International Bridge project (expected to be finalized in Q3’25). Getting past the legacy projects will position ARE to finally display its normalized earnings power, which might spark a valuation re-rating closer to peer multiples. ARE is set to report Q4 earnings on March 5, which is when I would expect the company to provide an update on the legacy projects.

Pioneer Power Solutions (PPSI)

In mid-January, the company announced another contract win, this time a $1.3m e-Boost order, expected to be delivered in Q2’25. Despite further evidence that PPSI’s e-Boost product line is gaining market traction, the shares have sold off over the last month, and the RemainCo is currently valued at only 2.4x 2025E EBITDA and 0.2x revenue multiples. These are way too low multiples considering the e-Boost business’s impressive recent growth (100% guided in 2024) and further growth runway given the rapid expansion of the EV market and the anticipated launch of the new product HOMe-Boost. I would remind you that the company has recently announced a pilot program with a Fortune 100 retailer, which, judging by this tweet, appears to be Amazon. A potential large partnership agreement with Amazon could provide a massive boost to the company’s topline/EBITDA, and yet I’d argue that at the current price levels, we are not paying for this optionality. With the investment thesis intact and substantial upside potential, I continue to find the setup compelling and have maintained my position.

Summit Midstream Partners (SMC)

SMC’s share price is up 12% since the beginning of January, with no material news or announcements from the company. Despite the slight share price run-up, SMC remains cheap, trading at 7.3x 2025E EBITDA pro-forma for the Tall Oak acquisition, compared to 8.5x+ multiples for its peers and 10x+ multiples seen in comparable industry transactions. What makes SMC interesting is that there are several catalysts that might help close the valuation discount, most notably, a potential dividend reinstatement, which management has hinted might materialize in 2025. This would likely be a significant catalyst, as the stock would attract a dividend-focused investor base. Other potential catalysts include the continuing ramp-up of SMC’s crown jewel asset, Double E, and the continuing influx of institutional investors following the C-Corp conversion completed last year. Given SMC’s high leverage, even a relatively modest, say 0.5x, multiple re-rating would imply a 30%+ upside from the current stock price levels. With SMC trading at a low multiple and several catalysts on the horizon, I continue to like the setup.

EXITED: Montero Mining and Exploration (MON-V)

Last week, Montero finally provided more information on the arbitration funding and litigation costs. The company expects to receive C$21m in net settlement proceeds after funding and legal costs, which implies funding/legal costs of C$18m, or C$4m higher than I previously estimated. Management has noted that it "is considering a return of capital distribution to shareholders," but the exact amount has not been provided. Assuming the company will retain C$5m for admin and other costs, the potential distribution would come out at C$17m, which is right in line with the current market cap. Given the narrow margin of safety, I have exited my position at C$0.32/share. While there is a chance that my estimates are too conservative and that I might be leaving some upside on the table, I think it is prudent to close my position given the uncertainty regarding capital allocation and the size of potential shareholder distributions—especially in light of the recent exit of activist Jeremy Raper.

Thryv Holdings (THRY)

In case you missed it, I shared a pitch on Thryv this week. I think THRY presents a compelling GoodCo/BadCo setup, where the legacy Yellow Pages business has obscured the rapid growth and solid economics of the company’s other segment—the higher-quality SaaS business. However, with the ongoing transition away from the declining legacy business toward the SaaS segment, the company is on track to transition into a primarily software business in the near term, likely this year. Once this happens, I expect the market to finally start perceiving THRY as a software business—this should drive a significant stock price re-rating, with potential multi-bagger upside.

SUTL Enterprise (BHU-SI)

There have been no updates from BHU over the last month, and the stock is trading just above the write-up levels. The investment thesis remains unchanged: BHU is a high-quality business trading at just 8x P/E, with 90% of the current market cap in net cash. This implies that investors are effectively paying nothing for the cash-flow-generating operating business or getting the operating business at a low valuation while paying zero for the company's net cash. I would expect an update from the company regarding the One°15 Marina lease renewal in the near/medium term — this could spark a stock price re-rating.

Perma-Fix Environmental Services (PESI)

Nothing material to update on PESI other than the recent new COO appointment and the company approving 2025 incentive plans for the CEO and CFO. The PESI investment thesis remains pretty simple: With reasonable assumptions, PESI is likely to generate around $100m in annual EBITDA from the two Hanford site-related contracts starting in 2026, compared to the current EV of c. $150m. I believe that sub-2x EV/EBITDA multiple is far too low a multiple for a highly visible, recurring, long-term (10+ years) revenue stream. I would expect PESI to re-rate to a more appropriate multiple, say 8x, when the company begins fulfilling these contracts, likely in the back half of 2025. Aside from the Hanford site opportunity, what also makes PESI interesting are other growth optionalities, most notably PFAS and the West Valley award. While I have no conviction that these opportunities will turn out to be successful growth avenues, I think that at the current stock price levels, investors are not paying for them.

Enav (ENAV-MI)

Eurocontrol has recently released the en-route/terminal tariffs for the 2025-2029 period. The key takeaway is that the tariffs have turned out to be slightly lower than previously expected, with sell-side downgrading its estimates of ENAV’s EBITDA by low/high teens for the period. ENAV's stock price has declined by 16% since early January. While the lower-than-expected tariffs are a negative, I think this is far from a thesis-breaking development. The company remains cheap, trading at 7x 2025E EBITDA adjusted for the cash owed to the company by airlines. This valuation is too low, considering that ENAV is a regulated monopoly generating contractual cash flows and boasting 25%+ EBITDA margins. The valuation is also substantially below other European airport operators, which are trading at 10x+ multiples. I think the stock is poised for a re-rating closer to peer valuations as the company continues to receive COVID- and inflation-related accruals.

Warrior Met Coal (HCC)

Highlighting the recent announcement from the Chinese government regarding 15% tariffs imposed on U.S. coking coal imports. The tariff implies that U.S. producers will need to discount prices and/or reduce production to remain competitive compared to exports from Australia. I’d regard this as a slight negative for HCC. China is one of the company’s three key markets in Asia (c. 40% of HCC’s sales come from Asia). Nonetheless, here I would highlight HCC's position as the lowest-cost and highest-quality metallurgical coal producer in the U.S., which will provide the company significantly more flexibility for price cuts compared to its U.S.-based peers. As for the broader met coal industry overview, met coal producers continue to operate in a downcycle market, with a slight decline in met coal prices over the last month. While I would expect these conditions to persist in the near term, I continue to expect a recovery in met coal prices over the medium term, given that at current met coal prices, marginal producers—primarily U.S.-based ones, excluding HCC—are operating at or near break-even levels. HCC is currently trading at c. 6x my estimated mid-cycle EBITDA less capex, before accounting for the potential contribution from the company’s development-stage Blue Creek asset. I will be waiting for HCC’s earnings, scheduled for February 13, to assess the company’s operational performance and management’s commentary on the industry outlook/impact of tariffs.

Amplify Energy (AMPY)

The major update from AMPY in January was the acquisition of oil assets in the DJ and Powder River Basins. If I had to grade the acquisition, I would give it a C-/D+. While the merger will increase the company's scale, implying a lower relative corporate overhead burden, I would be hard-pressed to call the acquisition positive from a value accretion perspective. The assets will be acquired at 0.88x PV-10 value, while AMPY trades at 0.65x PV-10, with limited geographic synergies. But perhaps more importantly, the acquisition indicates that a company sale is off the table for now. The market seems to agree with my evaluation of the merger, with AMPY shares down 9% since the announcement. Despite the seemingly negative news, I continue to find AMPY attractive, given how inexpensive the core business is and the Beta development optionality. With reasonable assumptions, Beta’s value alone could equal the company’s current enterprise value, suggesting massive upside optionality for which we are currently paying very little. I will be eagerly waiting for AMPY’s Q4 results, likely to be released in early March, for updates on the Beta drilling program and core business operational performance.

WideOpenWest (WOW)

The waiting game continues, as nine months have passed since the non-binding takeover bid without a definitive agreement announcement. The prolonged timeline is starting to spook the market, as WOW's stock price has fallen by 12% over the last month, with the spread to the takeover bid now at 13%. I think that, at the current stock price, the market might be pricing in a significant chance that the transaction could fall through. Using the pre-announcement level ($3.79/share) as the deal-break price and assuming a potential price bump to $6/share, the implied deal closing probability is around 20%. I think this probability is too low, given that there have been no indications that takeover negotiations have ended, alongside Crestview and DigitalBridge’s strong reputations and clear interest in acquiring cable assets. I would note that my downside scenario price estimate might be overly conservative, considering that the share prices of several of WOW’s peers, including CHTR and ATUS, have risen more than 30% since the non-binding offer was made. Given the skewed risk/reward, I continue to like the setup and have maintained my position.

SunOpta (STKL)

Nothing material to update on STKL. The company is expected to report Q4 results in late February/early March, at which point I intend to assess the company’s operational performance. Until then, I continue to believe that STKL remains an attractive short opportunity. With ongoing post-Covid demand normalization and new supply entering the industry in the near term, it is likely that the industry will soon shift from undersupplied to oversupplied. This is expected to drive a deterioration in STKL’s pricing and, thus, topline/margins in the coming quarters. The real detractor to the short thesis so far has been strong performance in the foodservice (i.e., coffee shop) channel, offsetting evident weakness in retail. While this is puzzling, it seems that the rapid growth in the foodservice channel has been driven largely by market share gains and new product launches. Given STKL’s already dominant position in the plant-based milk market and broader consumer weakness, I think that the recent foodservice growth might not be sustainable.

Sun Corporation (6736-T)

There has been some divergence in CLBT and 6736 share price movements over the last month, with a rally in CLBT’s stock price compared to flatness in 6736-T’s stock price, pushing the discount to NAV up to 49% currently. I think the market might be getting concerned that Sun Corp’s management has yet to announce any measures to address the discount to NAV, despite the fact that the activist investors have been on the company’s shareholder register for over 6 months now. While I share this concern, given the presence of three mostly reputable activists and the fact that Sun Corp’s management has indicated it would be open to “considering various measures to enhance Sun shareholder value,” I continue to believe that some form of value realization is likely in the near term. As for the most likely forms this value realization might take, I think the most likely options are 1) a distribution of Sun’s stake in CLBT to equity holders or 2) an outright sale of CLBT to a third party.

Active Portfolio Ideas

Below you can find links to the initial pitches and latest update posts for each active portfolio idea.

MGP Ingredients (MGPI) — initial post here, last update here

Pioneer Power Solutions (PPSI) — initial post here, last update here

Summit Midstream Partners (SMC) — initial post here, last update here

Japanese Net-Nets — initial post here

Thryv Holdings (THRY) — initial post here

SUTL Enterprise (BHU-SI) — initial post here

Perma-Fix Environmental Services (PESI) — initial post here, last update here

Warrior Met Coal (HCC) — initial post here, last update here

Sun Corporation (6736-T) — initial post here, last update here

Closed Portfolio Ideas

Below you can find links to the initial pitches and latest update posts for closed portfolio ideas.

Re-SUTL "I would expect an update from the company regarding the One°15 Marina lease renewal in the near/medium term", what's the basis for that prognosis?