Enav (ENAV-MI) — initial post here

Today, I’m sharing an update and my latest thoughts on ENAV, as the company released its H1’24 results yesterday.

For a quick recap of the investment thesis, here’s how I summarized the setup in my initial post published in May:

ENAV is a €2.2bn market cap company that operates a perpetual concession to provide air traffic control services in Italy. The company generates fees whenever an airplane flies over Italian airspace and/or takes off or lands at an Italian airport.

At the current share price, ENAV is trading at approximately 7x 2024 EBITDA, adjusted for the cash owed to the company by airlines due to declines in traffic since COVID-19. This is an undemanding valuation for a high-quality business—a regulated monopoly that generates contractual cash flows and boasts 25%+ EBITDA margins. The current valuation is also substantially below the approximately 10x average multiple at which other European airport concession operators and Italian utility companies trade.

The crux of the investment thesis, and the reason for the opportunity, is that ENAV’s convoluted accounting has obscured the true economics of the business, with a mismatch between the company’s cash flows and IFRS earnings. The company’s cash flow generation has lagged IFRS earnings in recent years due to lower than expected traffic because of COVID-19 and higher than expected inflation. However, the key aspect here is that ENAV is contractually set to be reimbursed for these impacts via higher rates in the coming years, which is expected to drive a material improvement in cash flow generation.

Now, on to the H1’24 earnings.

There are several key takeaways from the earnings release:

ENAV continues to perform well operationally, with a positive outlook from management for the second half of the year.

The company continues to receive payments accrued during the COVID (2020-2021) and inflation (2022-2023) years.

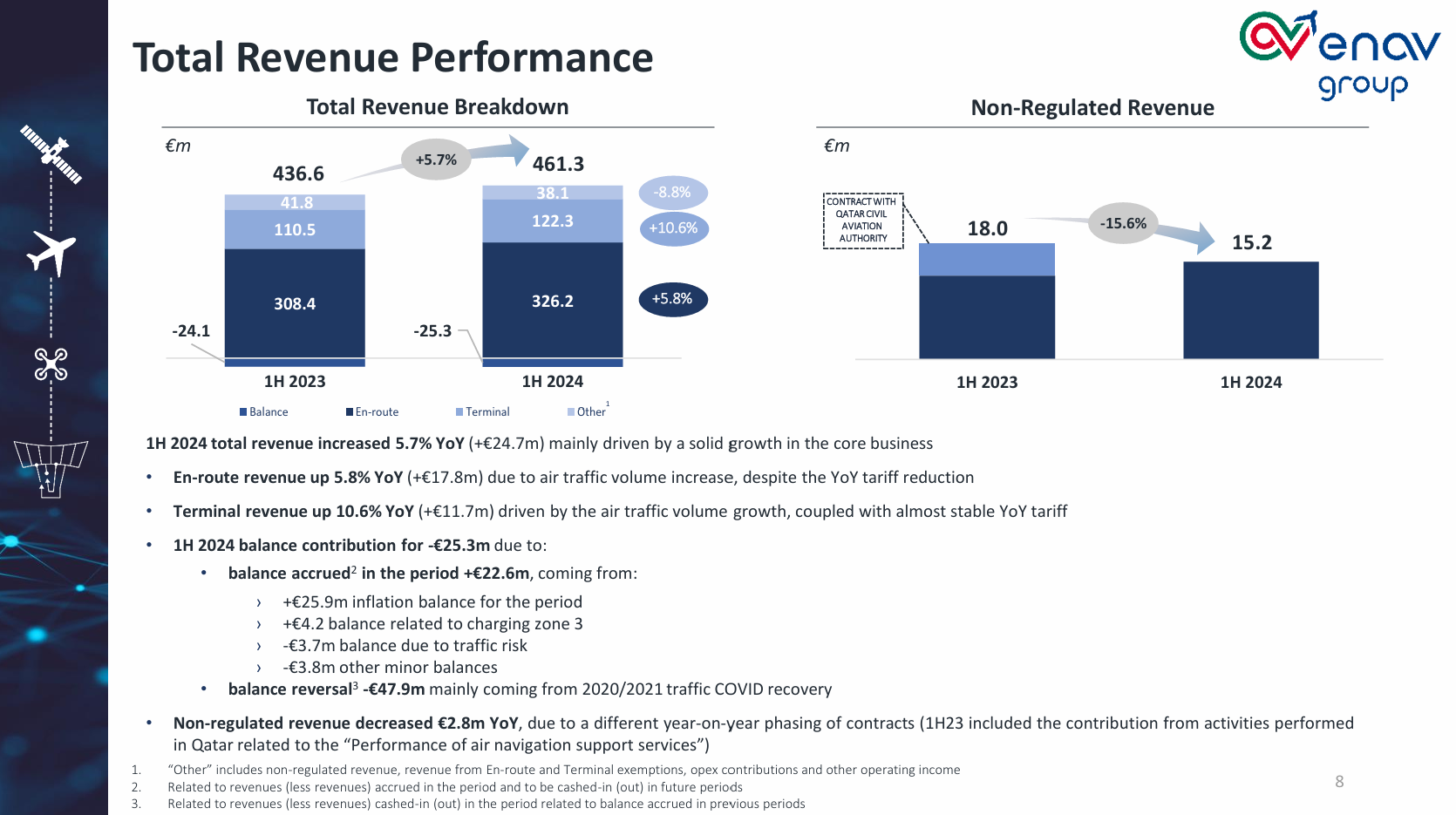

Let’s start with a brief overview of the operational performance. During H1’24, the company displayed solid performance thanks to the continuing growth in air traffic over, to, and from Italy. The slide below indicates the growth in both the number of flights and service units (an amalgam of the size of the airplane, distance flown in Italian airspace, and the popularity of the departing and/or arriving terminal airport) across the two key En-Route and Terminal businesses. Strong travel demand has led to solid performance across both segments, with total revenue and EBITDA both up by 6% (see another slide below).

As for the outlook, management provided a positive outlook for H2’24, highlighting that traffic growth is likely to remain at similar levels for the remainder of 2024 (see the quote below).

Another key takeaway from the earnings release was that the company continues to recover cash accrued during the COVID and inflation years.

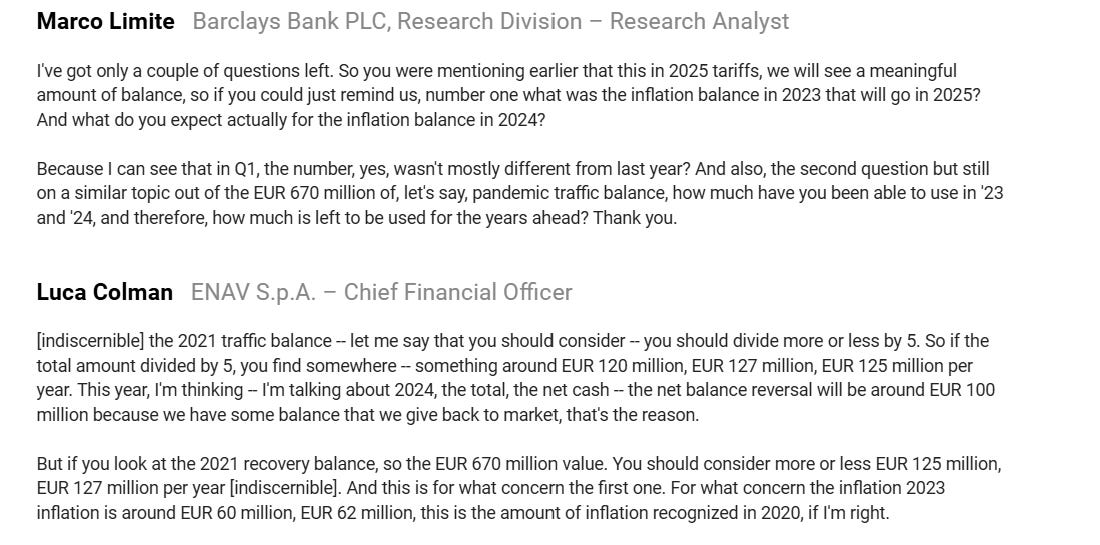

Let’s step back for a moment to better understand the accounting dynamics at work here. As you might recall from my initial post, during 2020-2023 ENAV recorded significant balance accruals related to COVID traffic and inflation risk-sharing mechanisms. These balances were incorporated into the reported revenues and EBITDA; however, no cash flows were received at the time. Subsequently, ENAV recognizes balance reversals once the cash inflows are received. The below quote from the Mar’24 conference call explains these dynamics. Note that the balance reversals have no impact on ENAV’s revenues and EBITDA.

The total COVID-related balance stood at c. €500m as of the end of 2023, to be paid out over five years starting in 2023. Meanwhile, inflation balances in 2022 and 2023 were at €35m and €63m, payable two years after they are recorded (so €35m in 2024 and €63m in 2025).

With this backdrop, let’s now turn to H1’24 balance reversals. The Covid-related cash inflows stood at €48m in H1’24 (see the slide above). The reversals (i.e. cash inflows) were below management’s previously mentioned target of cash inflows from COVID-related accruals of c. €120m-€127m annually. Nonetheless, ENAV has recently stated that the net balance reversal for 2024 is expected at €100m given other offsetting balances (see the exchange from the May’24 conference call below). So, I am inclined to interpret the H1’24 cash inflow from Covid-related accruals as a positive development, showing that the company continues to get reimbursed in line with expectations.

ENAV’s management did not provide any refreshed estimate of COVID/inflation-related reimbursements for this/next year, so I’d expect €100m from COVID accruals to be received this year, in line with management’s previous outlook. Note that this does not incorporate the expected inflation-related accrual recorded in 2022 (€35m). My understanding is that this cash inflow will come only at the end of 2024 given that it was recognized at 2022 year-end. So, I’d expect total cash recovery for 2024 to stand at c. €135m, a pretty significant amount given company’s current EV of €2.4bn.

So that’s a quick overview of the H1’24 earnings and near-term outlook.

Despite the solid operational performance and ongoing cash recovery, ENAV’s share price dropped 4% on the day, though I’d attribute that to the broader market sell-off.

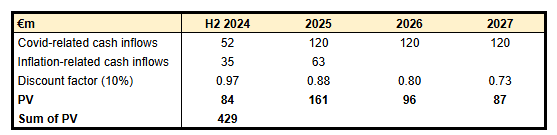

This brings us to the question of ‘where do we stand from the valuation perspective?’. Below is my refreshed estimate of ENAV’s enterprise value:

€1977m market cap.

€424m net debt as of June.

€429m estimated PV of COVID- and inflation-related cash inflows during 2024-2027 at a 10% discount rate (see the table below). Note that the COVID-related cash inflows are estimated based on the low end of management’s annual cash recovery guidance.

This leads to an enterprise value of €1972m.

Company’s guidance (mid-single-digit EBITDA growth in 2024) implies that the company is currently trading at 6.3x 2024E EBITDA while on a TTM basis the multiple stands at 6.6x. I think this is a cheap valuation for a high-quality regulated monopoly business that generates contractual cash flows and boasts 25%+ EBITDA margins. The current valuation is also significantly below European airport operators AENA-MC, ADP-PA, FRA-DE, and FHZN-SW, trading at 10-11x TTM EBITDA multiples. I’d expect ENAV shares to re-rate much closer to peer multiples as the company continues to recover accrued payments and/or the market becomes increasingly aware of the anticipated cash inflows over the coming years. The potential upside seems to be significant, as even a modest re-rating to, say, an 8x multiple would imply 25%+ upside from the current stock price levels.

And there might potentially be other catalysts aside from continuing cash recoveries. ENAV’s management has previously stated that it might raise the dividend once the regulator Eurocontrol sets the rates for the five-year period from 2025 to 2029, so-called RP4 period (see the quote from May’24 below). During the recent conference call, ENAV’s management stated that the RP4 process should be closed by the end of this year or early 2025. This would pave the way for a potential dividend increase and might thus catalyze a stock re-rating.

With the investment thesis on track and significant potential upside, I continue to think that ENAV presents a compelling investment opportunity and have maintained my position.

Why are we using bullshit earnings, as Munger puts it? Depreciation/capex is a real expense and I have no idea how profitable this business, nor whether it's cheap or expensive, without knowing their capital costs.