New Portfolio Position — BHU

High-quality net-net at 8x P/E and 7% dividend yield

Today, I am back with a new portfolio idea: SUTL Enterprise (BHU-SI). I believe BHU presents an attractive opportunity to own a high-quality business—a growing, high-margin local monopoly—at an undemanding 8x P/E multiple. With the majority of the company’s current market cap covered by net cash, investors are getting the free optionality of significant further growth and/or substantial capital returns to equity holders. While there is no certainty if/when either of these outcomes will materialize, at the current stock price levels the downside is protected while investors are well rewarded to wait, as the company boasts a solid 7% dividend yield.

I came across BHU in this VIC write-up from September. The setup has also been well analyzed on several investment blogs, including The Mikro Kap (here) and Asian Century Stocks (here, paywalled), so I’d highly recommend reading them.

Without further ado, let’s dive right into the investment idea.

SUTL Enterprise (BHU-SI)

Elevator pitch: High-quality net-net trading at 8x P/E and offering a 7% dividend yield.

Current price: S$0.695

Target price: S$1+

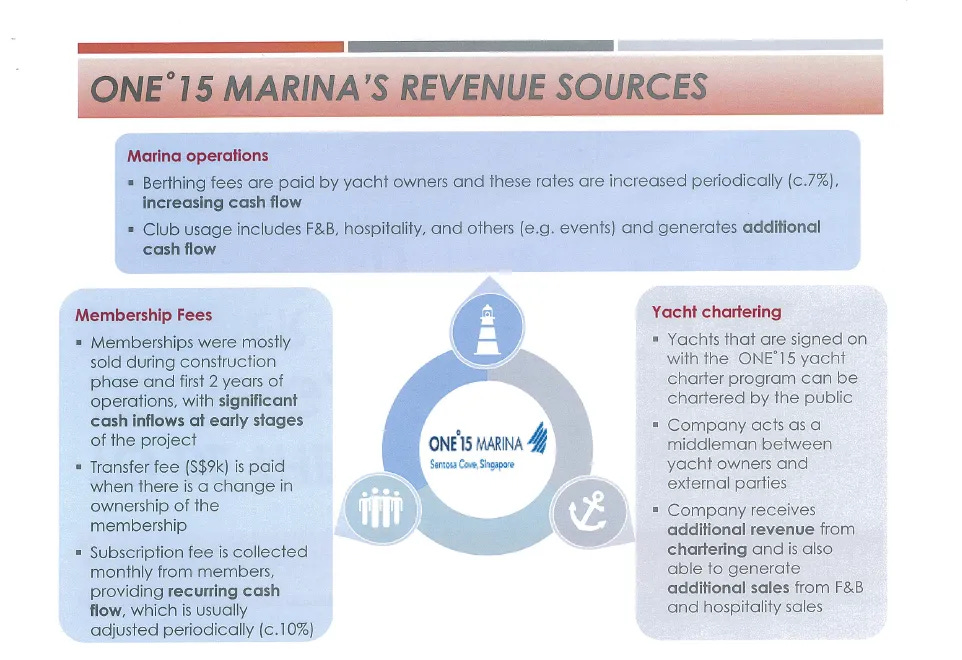

BHU is a S$61m market cap company that operates high-end marinas. The company’s crown jewel asset, accounting for the vast majority of its revenues and earnings, is the One°15 Marina, located on Sentosa Island, Singapore. It is the most prestigious marina in Asia and one of the most renowned globally (i.e., Monte Carlo of Singapore). As shown in the slide from company’s investor presentation below, BHU generates revenues primarily from membership fees (i.e., entrance and subscription fees), along with yacht berthing fees and revenues from other services, including hospitality, food, and customer yacht servicing.

Aside from One°15 Marina, the company operates two marinas in Brooklyn, U.S., and Indonesia. Unlike One°15 Marina, which is owned by BHU, the other marinas are operated under management contracts with third parties. Under these agreements, the third party retains marina ownership, while BHU receives fees for managing day-to-day operations. BHU is also currently developing four marinas in China, Indonesia, and Thailand, similarly under the management contract model.

Let’s establish right away that BHU’s key asset, One°15 Marina, is a high-quality business with strong pricing power. As shown in the slide above, berthing and membership subscription fees have generally been adjusted upward annually by c. 7-10%. To illustrate this point, I would highlight that, just since 2022, berthing fees have increased across the board—for instance, large yacht wet berthing rental rates are up 12% since 2022 (see here and here). Despite the significant price increases, customer demand has remained robust: the marina’s most recently reported occupancy stood at 97%, while management has previously indicated that waiting lists for club memberships were over two years long. So, what explains this strong pricing power? There are several factors:

High-end marinas are effectively monopolies in specific locations, given that only a small portion of certain oceanfront areas are suitable for building marinas. Even if a suitable area is located, the construction of new marinas faces regulatory constraints and potentially prolonged timelines. To illustrate this point, One°15 Marina is the only marina on Sentosa Island and one of a handful of marinas across Singapore. While there are other waterfront berths on Sentosa Island, none can accommodate larger yachts as One°15 Marina can. This limited local supply means yacht owners have no/limited nearby alternatives for docking their yachts.

On the demand side, the number of large yachts in Southeast Asia has grown rapidly in recent years, with a 29% increase in the number of superyachts over the last five years. I would also highlight that yacht owners are, almost by definition, price-insensitive. Even if some were sensitive to price, marina costs are often a relatively small component of overall yacht ownership costs. This explains why One°15 Marina customers generally have inelastic demand for marina services.

The attractiveness of the business is reflected in BHU’s recent operational performance. While the company’s revenues were fluctuating/flat before COVID, since 2020, the company has displayed solid growth, with a 14% sales CAGR from 2020 to 2023, and revenues are currently substantially above pre-COVID levels. Given sizable margins and relatively low maintenance capex requirements, BHU has historically been consistently cash flow generative, with over 15% of the current market cap generated in free cash flow in both 2022 and 2023.

How will the operational performance look going forward? The luxury yacht market (see here) and the number of ultra-high-net-worth individuals in Asia (here) are expected to continue growing rapidly in the coming years. This, coupled with existing waiting lists reflecting the already present demand-supply imbalance, suggests that the company’s topline is likely to continue growing in the coming years.

At this point, it would not be unreasonable to think that a business with these characteristics—a growing local monopoly with strong pricing power—should trade at around a 20x P/E multiple. Yet, at the current stock price levels, BHU is trading at only 8x TTM P/E, with 90% of the current market cap in net cash. I think there are two ways to frame the opportunity the market is presenting to investors:

Investors are essentially not paying for the high-quality, cash flow-generative operating business.

Investors are getting the operating business at a low valuation and paying zero for the company’s net cash. This cash is likely to either be reinvested into further growth or returned to equity holders.

To elaborate on the second point, I must note that there is no certainty regarding if/when the company’s growth projects will bear fruit in terms of higher growth, or if/when the company will initiate large capital returns. Nonetheless, at the current stock price levels, the downside is protected while investors are well-compensated to wait, given BHU’s solid 7% dividend yield.

So, that’s the investment thesis in a nutshell. Now, as with every investment, I think it is worth addressing the question: why is the market offering us this opportunity? Aside from the more obvious explanation that BHU is a relatively illiquid Singapore-listed company, I believe there are two other key factors at play:

Key asset risk. BHU’s One°15 Marina asset is held under a government leasehold, which expires in 2034. Given that Sentosa accounts for the vast majority of the company’s revenues, failure to renew the leasehold would lead to a massive deterioration in operational performance.

Capital allocation risk. BHU is a Singapore-based company largely owned by the controlling Tay family (which holds 54% of the outstanding shares). So, the market might be pricing SUTL as a typical cash-rich Asian micro-cap stock, where management is unlikely to return the cash to equity holders. A related risk is that management, with its history of pursuing growth projects, could waste net cash on value-destructive acquisitions.

While these risks are definitely worth considering, I believe there are solid counterarguments to each of them.

Starting with the One°15 Marina leasehold renewal: as highlighted in the VIC write-up, a leasehold renewal seems likely, given that BHU has been a strong operator of the asset, with the marina consistently ranked as one of the best globally. This suggests that the government may be incentivized to keep the marina running smoothly. Additionally, the government might prefer that the marina remain operated by a Singaporean entity, rather than a foreign one. Negotiations between the two sides appear to already be underway, as during this year’s AGM, BHU’s management stated that it is in discussions with the government to renew the leasehold. So, I would expect an announcement regarding the potential leasehold renewal in the coming quarters or years, which would likely be a significant catalyst for the stock. Even if the parties fail to reach an agreement on renewal (unlikely, in my opinion), I would note that BHU’s discounted cash flows from One°15 Marina would still exceed the company’s current market cap, and that’s before assigning any value to the company’s current net cash.

As for the capital allocation risk, it’s important to note that management has a track record of failed growth projects, including a JV project in Malaysia that was eventually shut down after negatively impacting earnings since 2019. However, in recent years, BHU’s management has scaled back its growth plans and initiated several shareholder distributions. For example, the company pursued stock buybacks in 2020 (S$0.4m) while also initiating a large special dividend in 2021 (S$9m). Last year, BHU significantly raised the regular dividend, from S$1.7m in 2022 to S$4.4m (S$0.05 per share, or a 7% yield) in 2023. Given the materially improved capital allocation in recent years, I believe the risk of value-destructive acquisitions is low, and I would instead expect increasing shareholder distributions in the coming years.

Hi Idea Hive, thanks for sharing your research on SUTL. We looked at SUTL Enterprise in July 2023 and decided to pass primarily because we worked out that SUTL Enterprise only had 14 years (back then) left for its lease of One Marina 15. The company paid S$32 million in 2006 for the land lease, and it would be profitable to renew at the same rate it got the land for back in 2006. But Singapore has seen some serious inflation in land prices, so by the time the lease-renewal comes up for One Marina 15, it's likely going to be *much higher* than S$32 million. So, we think most of the cash that SUTL Enterprise has on the balance sheet is probably locked up for a long time in anticipation of the lease renewal and has very little chance of being returned to shareholders.

Another more minor worry we picked up was that SUTL Enterprise is only a small part of the the Tay family's overall business empire which is the SUTL Group. We thought it was possible that SUTL Enterprise may not receive full management-attention.

Just our 2 cents - happy to hear your thoughts!

Just checked on Bloomberg and the ticker I'm seeing for SUTL Enterprise Ltd is SUTL (in Singapore) and SUTLF (on US exchanges). I'm not seeing it listed under BHU or BHU-SI on any exchange. Am I missing something?