New Portfolio Idea — WOW

Attractive bet on a higher offer in a pending takeover

In this post, I’m back with a new portfolio idea: WideOpenWest (WOW). I believe WOW presents one of the more intriguing special situation plays currently available in the market. The company is in the process of being acquired by its largest equity holder. The current takeover proposal is evidently lowballed, leaving plenty of room for a price increase. The situation has been well-analyzed in public letters from several of WOW’s equity holders, including LB Partners (here) and Andrew Walker (here and here), so I’d highly recommend reading them.

Without further ado, let’s dive in.

WideOpenWest (WOW)

Elevator pitch: Attractive bet on a higher offer in a pending takeover.

Current price: $5.62

Target price: $10+

WideOpenWest is a $465m market cap cable and fiber broadband provider operating across six states in the U.S. Midwest and Southeast regions. The company provides internet, TV, and phone services via its 1) legacy hybrid fiber-coaxial (HFC) and 2) fiber-to-the-home (FTTH) networks. WOW operates as a cable/fiber overbuilder, meaning it constructs and operates infrastructure in areas with incumbent cable providers.

The investment opportunity centers around WOW’s major shareholder Crestview Partners’ attempt to acquire the company. In May, WOW received a takeover bid at $4.80/share from a buyer consortium comprising Crestview (which holds a 39% stake) and the digital infrastructure investment firm DigitalBridge. In response, WOW has formed a special committee of independent directors to evaluate the bid.

The transaction is highly unlikely to proceed under the current terms. LB Partners, the largest minority shareholder with an 8% stake, and Andrew Walker have both opposed the offer, arguing that it is opportunistic and significantly undervalues the company. A materially higher bid from the buyer consortium will likely be required to appease WOW’s special committee and/or equity holders. With WOW shares currently trading 17% above the offer level, the market seems to be expecting a price bump from the bidder consortium.

There are several arguments for why the takeover proposal is lowballed and why there is significant headroom for a price increase above the current stock price:

The current bid values WOW substantially below relevant industry transactions, including WOW’s own asset divestitures, and peer valuations.

The offer undervalues WOW on a replacement cost basis.

The acquisition bid is opportunistic, coming as WOW is likely on the cusp of an operational performance inflection.

Let’s discuss these in order.

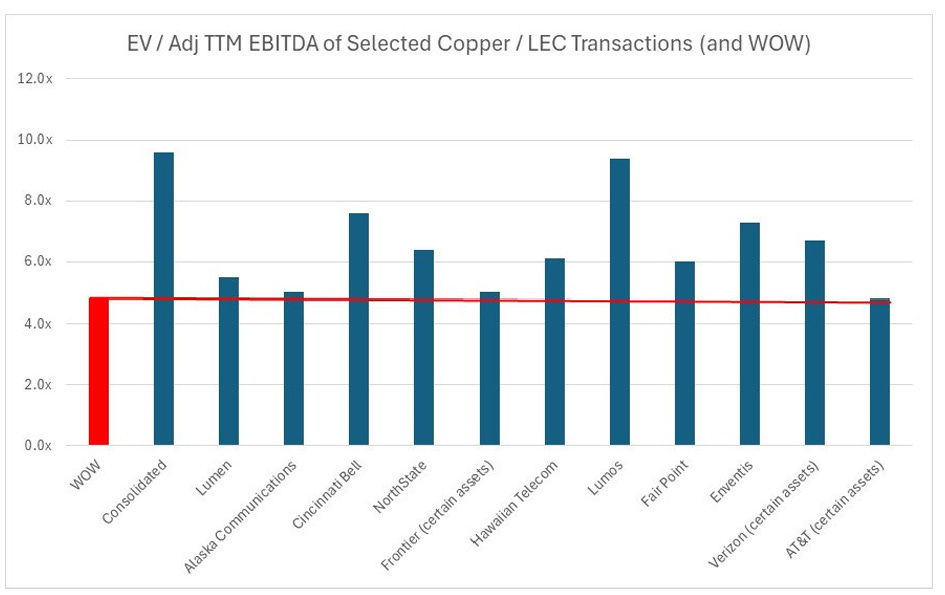

Starting with the valuation compared to industry transactions, Crestview’s bid values WOW at 5x TTM EBITDA. As illustrated in the chart below, this is at the low end of the industry transaction range of 5x-10x. It should be noted that these transactions primarily involved lower-quality copper/DSL assets compared to WOW’s HFC/fiber cable infrastructure. A particularly interesting case is the pending acquisition of copper/fiber telecommunications provider CNSL by its major shareholder, Searchlight Capital, at a 70% premium, valuing the target at 9.6x TTM EBITDA. Why is this interesting? Several reasons:

CNSL has been burdened by a significantly higher debt load (compared to WOW) amid ongoing capital expenditures for its fiber expansion program.

CNSL has been operating a declining legacy copper business, in contrast to WOW’s generally stable and cash-flow-generative HFC business.

So, despite the fact that WOW and CNSL are not direct comps, this precedent directionally illustrates WOW’s undervaluation at the current offer price.

The offer’s valuation is also significantly below the c. 11x EBITDA multiples at which WOW sold several of its fiber assets back in June 2021 and November 2021. Now, you might be thinking, "The industry backdrop/multiples have significantly deteriorated since 2021, so those divestiture multiples might now be irrelevant." And I'd agree—it is highly unlikely that WOW could fetch a similar multiple in the current environment. However, it is worth noting that at the time of the divestitures, WOW indicated that the sold assets were of lower quality compared to the remaining markets, given their significantly lower penetration rates. Considering this, I'd argue that the discrepancy between the valuations of the current offer and WOW's divestitures is too wide.

On the relative valuation front, WOW is currently trading below the 6-7x EV/EBITDA valuation range of its cable peers—CHTR, ATUS, CMCSA, and CABO (see the table below). WOW admittedly deserves a slight discount to its peers, given that it is a cable/fiber overbuilder. This means WOW must offer lower prices and/or higher speeds compared to competitors to convince customers to switch, generally leading to lower penetration rates. Nonetheless, I think that the current valuation discount to peers is too wide. As pointed out by LB Partners, at the time of WOW’s asset divestitures in June 2021, CHTR was trading at 11.3x EBITDA, a much smaller 0.3x premium to where the divestitures were completed. So, peer valuations support the view that at the current and offered prices, WOW is undervalued.

The offer’s undervaluation is also evident when considering WOW’s asset value. Crestview’s bid values WOW at $680 per passing (both HFC and FTTH). This is substantially below comparable transaction ‘EV/home passed’ valuations (e.g., CNSL was acquired at around $2,500/passing) and is close to the low end of WOW’s own network build-out costs. WOW’s management has highlighted that the company has been spending c. $1,050/passing in its greenfield investments (both HFC and fiber), while the cost of edge-outs has ranged from $650 to $750 per passing. For quick background, greenfield investments refer to building new infrastructure from scratch, while edge-outs refer to expanding an existing network into adjacent areas. It’s important to note that these edge-out and greenfield cost estimates provided by WOW’s management do not include the full costs of connecting the end customer’s home to the network. So, I think it is fair to conclude that the current offer values WOW below its replacement cost.

But that’s not all—I have yet to discuss another intriguing aspect of Crestview’s offer: its opportunistic timing. The bid came just days before Q1 2024 earnings, which I’d consider a potential inflection point for the business. To understand this, let’s briefly review several headwinds the company has faced in recent quarters/years:

Last year, the company’s operational performance in its core business suffered due to poorly managed price increases. This, coupled with intensifying competition from fixed wireless operators, led to a significant decline in subscribers. In Q3 2023, WOW announced a significant decline in its total broadband customer base (approximately 4,000 vs. about 500,000 total subscribers), with management guiding for “triple” Q3 losses in Q4. This spooked the market, causing the share price to nearly halve following the Q3 earnings announcement. The stock has barely recovered since then up until the recent takeover bid.

In recent years, WOW has made significant capital investments in its fiber build-out (c. $180m or >$2/share spent since the program’s start in 2022). This expansion program temporarily elevated net debt levels and led to negative cash flows, as it typically takes several years for fiber assets to mature.

However, it seems that these headwinds are now likely behind the company and so WOW might be on the brink of an inflection.

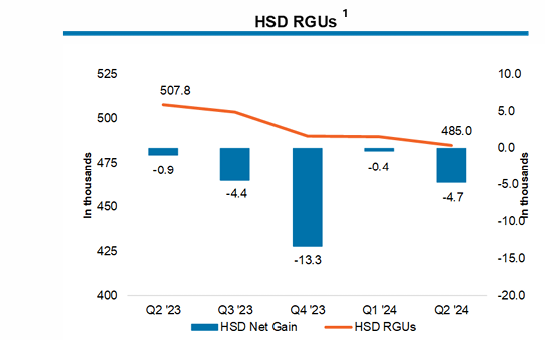

On the operational performance front, WOW’s management has taken steps to address issues related to the legacy business, including updating the pricing plans in February. The new, simplified pricing plans appear to have improved customer retention. As illustrated in the chart below, Q1 and Q2 results show stabilization in the number of subscribers. Note that the decline in subscriber count in Q2 was largely driven by the ending of the Affordable Connectivity Program (ACP). Notably, during the Q2 conference call, management stated that there has been a “softening of any competitive impact from fixed wireless.”

As for the fiber build-out, the majority of WOW’s near-term capital expenditures have already been incurred. WOW spent $43m and $10m on greenfield build-out capex in Q1 and Q2, respectively, compared to the $60m guidance for 2024. With the expected decline in capex and WOW’s fiber assets maturing, the company is in a solid position to generate significant cash flows in H2 2024 and beyond.

So, while Crestview’s bid came at a sizable premium to pre-announcement levels, I think it’s fair to suggest that WOW’s stock would have risen substantially since the Q1 results without the takeover bid. This implies that the offer might effectively be coming at a minimal or even no premium. As further evidence that the pre-announcement price might not be a relevant reference point, CHTR is up 31% since Crestview’s bid announcement. As argued by Andrew Walker in this open letter, peer performance has been driven by factors applicable to WOW (e.g., slowing competitive pressure from fixed wireless players and a manageable ACP roll-off).

So, that’s an overview of the key arguments for why the current bid is lowballed and opportunistic. Given these points, coupled with pressure from several equity holders, I believe there is a strong likelihood of the buyer consortium making a substantial price bump.

What could be the potential upside here? One way to estimate a higher offer is to simply add the incremental value of WOW’s newly built fiber assets, given that these assets have yet to meaningfully contribute to the company’s profitability. Conservatively valuing these assets at cost and leaving the remaining business at the current offer valuation would imply a price target of around $7/share, or 25% above the current share price. But let’s assume the improved bid values WOW’s existing business at a slightly higher, 5.6x EBITDA multiple, which is one turn below CHTR’s valuation. This, coupled with valuing the fiber assets at cost, would imply a potential bid of $8.8/share, or 50%+ above the current stock price.

One point of pushback against this thesis is the “no deal” risk. Given the wide discrepancy between the current bid and WOW’s intrinsic value, it is possible that the company/special committee and the buyer consortium might fail to reach an agreement on a takeover bid. It should be noted that, unlike in the CNSL setup, WOW has already completed the vast majority of its fiber build-out program, meaning the company might simply decide to remain a standalone entity if the eventual offer bump is not substantial enough.

However, I think the “buyers walking away” risk is minimal. For one, the buyer consortium comprises large, highly reputable, and experienced industry players. Crestview is a large private equity firm ($10bn in AUM) that has previously made investments in the cable space, including in CHTR (stake acquired in 2009). Meanwhile, DigitalBridge is among the largest digital infrastructure-focused private equity firms ($80bn in AUM), focusing on cell towers, data centers, and fiber networks. This, coupled with Crestview’s multi-year involvement with WOW (stake acquired in 2015), indicates that the consortium is highly aware of WOW’s underlying value and is thus unlikely to walk away due to the need to bump the offer by several hundred million dollars. As an indication of this, during a recent investor conference, DBRG’s CEO indirectly hinted at the cheapness of WOW in the context of fiber industry multiples:

I think in the last panel you heard this disconnect between private M&A multiples and public M&A multiples. There's a big disconnect there, particularly like in fiber, where you saw private trade, you know, last week that was done at KKR paying like 22x, 24x for a cable business essentially, and a good cable business, mind you. But, and then in the same token, you see some of these public equities in fiber trading for 4 times. That's a pretty big value disconnect. 4x to 22x or 24x—that's about as big of a disconnect as I've seen.

Even in the unlikely scenario where the current bidders decide not to proceed with the transaction, I think there is a chance that WOW might launch a full sale process and potentially attract other interested parties. Why? For one, Crestview’s non-binding offer-related 13D filing does not include the statement that the bidder/major shareholder would oppose any alternative transaction. Another point is that the private equity firm had already initiated WOW’s sale process back in 2022, albeit it did not result in a transaction. These factors could indicate that Crestview might be a willing seller.