High-Quality SaaS Business at a Discount

Revealing a new portfolio idea

In this post, I am excited to share a new portfolio idea: Thryv Holdings (THRY). I believe THRY presents a compelling GoodCo/BadCo setup, where the declining Yellow Pages business has obscured the rapid growth and solid economics of the company’s other segment—the higher-quality SaaS business. However, with the ongoing transition away from the legacy business toward the SaaS segment, the company is on track to transform into a primarily software company in the near term, likely this year. Once this happens, I would expect the market to start perceiving THRY as a higher-quality SaaS business—this should drive a significant stock price re-rating, with potential multi-bagger upside.

The setup has been well analyzed by several funds and investors, including Laughing Water Capital (latest thoughts here), Greystone Capital (here), and Inflexio Research (here), so I would highly recommend reading their analysis.

Now, let’s dive right into the investment idea.

Thryv Holdings (THRY)

Elevator pitch: A fast-growing, profitable SaaS business hidden within the shell of a declining legacy business.

Current price: $17.67

Target price: $38+

THRY is a $743m market cap company that operates two segments: Marketing Services and SaaS.

Marketing Services (62% of revenues). This segment houses THRY’s legacy Yellow Pages business. For those unfamiliar, Yellow Pages are business directories that list companies, typically categorized by industry or service type. While THRY’s Yellow Pages are published primarily in the form of printed books containing business contact information, the company also operates digital directories such as YellowPages.com. The segment generates revenue primarily from ads placed within print and digital Yellow Pages, with print titles published on a 12- to 24-month cycle. The Marketing Services segment also includes a Search Engine Marketing business.

SaaS (38% of revenues). This segment includes THRY’s small and medium-sized business-focused business management software, Thryv. The software helps SMBs conduct their day-to-day operations, including appointment scheduling, customer relationship management, document management, and email marketing, among other functions (see the chart below). For example, regarding appointment scheduling, Thryv provides an online booking system that allows customers to see open time slots in real time and make payments when booking a reservation. Then, once a booking is made, the system sends email and SMS reminders. THRY organizes its software offerings into several so-called centers, including the core offering, Business Center (includes appointment scheduling, CRM, invoice creation, and other services), as well as Marketing Center (social media marketing automation) and Command Center (integration of different email/social media accounts into a single inbox). The software is sold on a monthly subscription basis, with most clients subscribing with an initial minimum six-month upfront commitment.

It’s not difficult to see the GoodCo/BadCo dynamics at THRY, given the differences in the two segments’ business models and growth prospects. While Marketing Services revenue comes largely from contracted but lumpy and discretionary advertising fees, SaaS generates recurring, sticky, and largely non-discretionary subscription revenues. In terms of growth prospects, Marketing Services is clearly a secularly challenged business, as the phone book/directory industry is expected to continue declining with the advent of the internet and its largely older target demographic. The SaaS business, meanwhile, is a vastly different story, as the majority of SMBs still do not use business management software and instead often rely on sticky notes and/or Excel. So, I think it’s safe to say that SaaS is a significantly higher-quality business than Marketing Services.

Aware of these dynamics, THRY’s management has, in recent years, been pursuing a business transition—migrating customers away from the Yellow Pages business to the SaaS segment while reallocating cash flow from the legacy segment to fund software growth. I would highlight here that Marketing Services has served as a cheap customer acquisition channel for the SaaS business, given that nearly all small businesses using Yellow Pages are potential customers for THRY’s software.

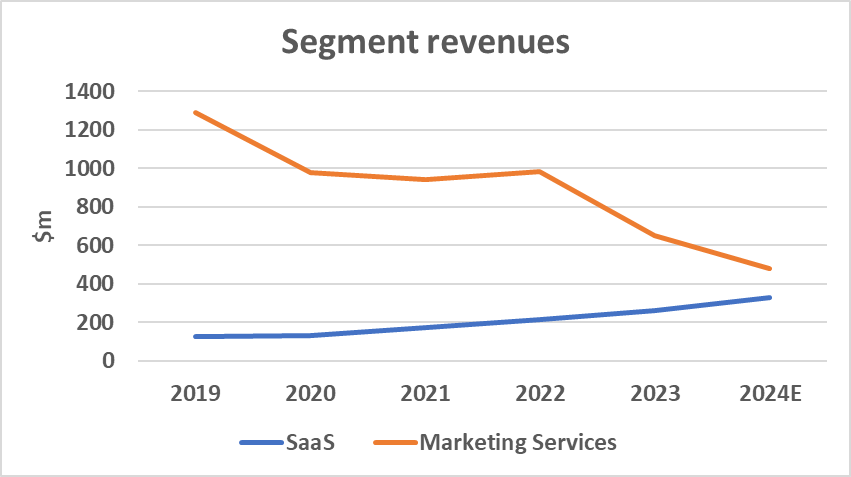

How has the transition been going so far? While the Marketing Services business has unsurprisingly experienced a rapid revenue decline in recent years, the SaaS segment has shown consistent and rapid 20%+ growth, albeit noticeably smaller in absolute terms (see the chart below). The revenue mix has shifted significantly, with SaaS’s share of total sales growing from 9% in 2019 to 38% through the first three quarters of 2024 and 48% in Q3’24. And this shift will continue in the coming years. At the December 2024 analyst day, THRY’s management projected SaaS revenue growth of 18–20% in 2025 and 20% over the medium term. Meanwhile, Marketing Services revenue is expected to decline by 35% in 2025, with the segment anticipated to be fully phased out by 2028. So, this means THRY is likely to become a primarily software-focused business this year and a pure-play SaaS company within 3 years.

So, the situation here is that THRY is a significantly different business than it was just a few years ago, and we are only several years away from the full transition to a pure-play higher-quality SaaS company. The key question, then, is this: Is THRY’s business transformation already reflected in its current valuation?

Well, I think this is what makes THRY interesting: despite the ongoing business transformation, the market has failed to appropriately value THRY’s growing, recurring revenue-generating SaaS business. To see how undervalued SaaS currently is, let’s turn to the valuation of the SaaS segment. THRY’s EV currently stands at 1040m. Given that the legacy business is in run-off mode and management is likely to reinvest its cash flow into the growth segment, I am valuing the Marketing Services business at zero. This means the company’s EV is effectively the valuation of its SaaS segment. Here’s what the SaaS business is expected to generate in 2025:

$471m in 2025E revenue. This estimate is based on management’s 2024 revenue guidance ($331m at the midpoint) and the projected 2025 revenue growth rate (19% at the midpoint). The 2025E revenue estimate also includes $77m in expected revenue from the Keap acquisition, announced in late 2024.

$81m in 2025E EBITDA. This assumes 15% EBITDA margins (in line with management’s "mid-teens" guidance) and $10m in synergies from the Keap acquisition.

So, at the current share price, THRY’s SaaS business is valued at 12.9x 2025E EBITDA and 2.2x 2025E revenue. While these may not seem like extremely low multiples, I consider this valuation undemanding for several reasons:

The SaaS segment is a fast-growing business (consistently achieving 20%+ revenue growth in each quarter since 2021) that generates recurring, sticky, and non-discretionary revenue. The business is capital-light, with 70%+ gross margins, and boasts strong customer retention (NRR of 100%+).

The valuation is also attractive on a relative basis. The closest publicly traded comps, HUBS and TTAN, are currently trading at substantially higher 12x and 15x FY24 revenue multiples. While HUBS and TTAN may warrant a premium over THRY’s SaaS business due to their focus on higher price point sub-segments and much larger size (market caps of $40bn and $9bn, respectively), THRY’s SaaS segment has actually been growing faster than its peers, as highlighted by company’s management (see the slide below).

So, I think it’s fair to say that THRY’s SaaS business is trading at an undemanding valuation based on this year’s revenue and EBITDA.

And these valuation multiples could decline rapidly in the coming years as the SaaS business continues to grow. THRY’s management has guided for $1bn in revenue by 2027, with 20% EBITDA margins. This would imply that the SaaS business is currently valued at a low 5.2x 2027E EBITDA multiple. Looking further ahead, by 2032, management expects the business to generate $4bn in revenue with 20%+ EBITDA margins. While I don’t have high conviction that the company will hit these revenue and EBITDA targets, several aspects suggest that it is likely to at least partially meet these goals: (1) the opportunity to grow user count and ARPU and (2) THRY management’s track record. Let’s discuss both points in order.

Starting with the opportunity to grow user count and ARPU. The client base is likely to grow as the company 1) continues converting legacy Yellow Pages customers and 2) acquires new clients. THRY’s management has highlighted that around half of new SaaS customers come from the legacy business, while another third comes from referrals. The Yellow Pages business had 251k clients compared to 96k SaaS clients as of September 2024. So, with a 20% conversion rate, the SaaS customer base would grow by more than 50%. I would note that the assumed conversion rate is below my estimate of Yellow Pages’ recent-quarter conversion rate of c. 30%. As for acquiring new customers, I would highlight the massive TAM (estimated at 5m SMBs in the US), given that most SMBs still do not use business management software. An important factor here is that THRY targets a specific niche—small SMBs with 5-25 employees—where it does not compete directly with much larger players like HUBS, TTAN, and CRM.

As for ARPU growth, THRY has plenty of opportunities to upsell its products. While the proportion of clients with two or more offerings has increased recently, it remained low at 12% as of September 2024. With new offerings being introduced (Reporting and Workforce Centers launching this year), I’d expect continued growth in the number of customers with multiple center subscriptions.

So, given the significant growth potential in both client count and ARPU, I’d expect SaaS growth to continue.

Another equally interesting aspect is THRY’s management track record. THRY’s management has so far met or exceeded each of its revenue and EBITDA guidance targets for the SaaS business since the IPO in 2020. I would highlight that as of Q3’24, THRY fully met its previous medium-term guidance for the SaaS business, which was set in 2020 (see here, p. 16). These points suggest that THRY’s management is either conservative in its guidance/targets and/or has strong visibility into anticipated revenue growth. Another factor that gives some confidence in management’s targets is its track record of growing similar companies. THRY’s CEO was previously the chairman of Cambium Learning Group, a SaaS business acquired in 2018 at a share price c. 15 times higher than its level when he assumed the role in 2013. He also served as CEO of Yellowbook from 1993 to 2011, during which time the company’s revenues grew from $38m to over $2bn.

Again, there’s no certainty that management’s medium/long-term revenue and EBITDA targets will be met. However, at the current stock price, achieving those targets is not necessary for the investment to work. Assuming the company continues growing at a 20% rate through 2027 (below the 24–29% growth rates recorded over the last four quarters) and maintains 20% EBITDA margins, this would imply $136m in 2027E EBITDA, or a 7.6x multiple. So, even if the company only partially meets its targets, the stock appears undervalued at current levels.

Let’s now quickly discuss why the opportunity exists. I think the key reason the market is missing this opportunity is that THRY screens poorly due to its overall revenues being flat or declining in recent years. Another factor is that the majority of THRY’s revenues still come from the Marketing Services business, so the company is classified as a Communication Services business rather than a software company. However, as THRY transitions to a primarily SaaS business, likely later this year, it will probably be reclassified as a software company. This should put the stock on the radar of software-focused investors, potentially catalyzing a significant stock price re-rating.

Where could THRY shares re-rate to once that happens? While I think peer revenue multiples of 12x+ are out of reach, even a much lower multiple would still imply significant upside. At a 4x 2025E revenue multiple, still 3x+ below the peer multiples, THRY shares would be worth around $38 per share, implying 100%+ upside from current levels.

So, that’s an overview of the investment thesis. What follows is a quick discussion of several noteworthy risks.

Recession. THRY’s SaaS offering focuses on small and medium-sized businesses, which are more vulnerable to operational performance deterioration in the event of a recession. As a result, there is a risk of a significant slowdown in SaaS revenue and new client growth if an economic downturn occurs. While this is a risk, I would note that around half of THRY’s customer base is made up of recession-proof businesses, such as home and personal services, including plumbers, electricians, and salons (see the quote from the May 2024 conference call below).

Our clientele are simply far more resilient to economic impact than the typical just broader small business. What do I mean by that? We deal with dirty businesses, not a lot of -- not a whole lot of white collar. We have 50% of our clients are people like roofers, plumbers, service-based contractors, service industry, right? They are people that if you have a leaky roof, you're calling a roofer. If you have a clogged toilet, you're calling a plumber. You just find a way to afford it because you have to. Even things like dentists, veterinarians and attorneys, which are the other subsets that we sell a lot of, these are services that you simply need. So they're a little bit more resilient to economic impact.

M&A risk. Another risk is management pursuing value-destructive M&A. To finance the recent Keap acquisition, the company completed an equity offering at a price 20%+ below the trading levels at the time. That said, I would note that, judging by the anticipated profitability and merger synergies ($10m EBITDA synergies vs $80m acquisition price), the Keap merger appears to have been executed at an accretive valuation for THRY. This, coupled with management’s sizable ownership stake (12%) and a solid track record of growing similar businesses in a shareholder value-accretive fashion, suggests that a value-destructive acquisition is unlikely.

SaaS growth slowdown. There’s a risk that SaaS segment growth could slow once the company exhausts its legacy Yellow Pages customer list. THRY’s management has highlighted that around 50% of new customers have come from Yellow Pages, with the number rising to 80% when including referrals from legacy customers. Nonetheless, as noted above, the company has a substantial growth runway as the majority of SMBs still do not use business management software. Another consideration is that even if the company does not add any new customers beyond the legacy customer list, we would still see significant 50%+ growth in the number of SaaS clients under conservative conversion assumptions.

No position, but I also like the idea. Wrote it up on my page over a year back. Just tough to gauge when that re-rating kicks in… but I believe it will, nevertheless.

Dollar based net retention rates are 100%, wonder if alludes to a degree of customer satisifaction or could that be something else?