Post-Earnings Update on PPSI

The setup remains attractive at the current stock price levels.

In this post, I am sharing a quick update on PPSI, as the company reported Q3 results last week and held a conference call a couple of days ago.

First, for those not familiar with the investment thesis, PPSI is an electrical power management product manufacturer, which presents an attractive way to bet on the expected EV infrastructure growth. Until recently, the company boasted two key product lines: e-Bloc (switchgear systems) and e-Boost (portable fast-charging units for EVs), before the recently announced divestiture of the e-Bloc business. Pro-forma for the segment sale, the remaining e-Boost business is valued at c. 0.6x 2025E revenues, an undemanding multiple considering the segment’s impressive recent growth and further growth runway.

The key takeaways from the Q3 earnings and the conference call were: 1) e-Boost’s revenue growth has finally inflected, with significant further growth anticipated for 2025, and 2) the company announced a large special dividend.

Let’s start with the special dividend. Along with the Q3 earnings, PPSI announced it will pay out a distribution of $1.50/share, totaling $17m (25% of the current market cap), using the proceeds from the e-Bloc business divestiture. The dividend will be paid on January 7 to PPSI shareholders as of December 17 (record date). This vindicates my previous contention that PPSI’s management, given its track record of announcing large special dividends after asset divestitures, would initiate a large capital return. I would highlight that the capital return was slightly higher than I expected, considering that back in 2019, after the divestiture of the Transformer Business, PPSI announced a distribution of 18% of sale proceeds ($12m special dividend vs. $68m sale proceeds), compared to the pending distribution of 33% of sale proceeds. This is clearly a positive, highlighting management’s willingness to return capital to equity holders.

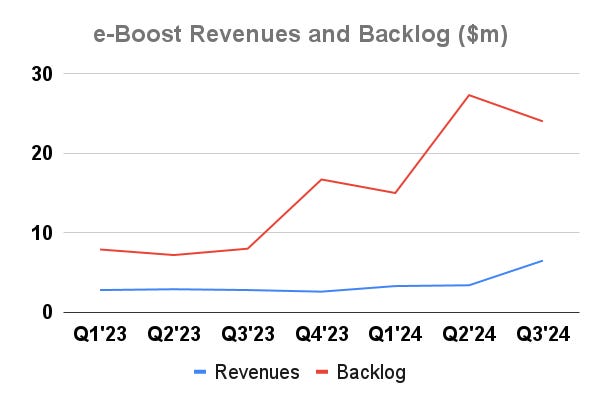

Another, perhaps even more important, positive from the Q3 earnings was e-Boost’s solid operational performance. In the quarter, we finally saw the previously anticipated revenue inflection in the e-Boost business, driven by significant growth in customer orders. The segment generated $7m in revenues compared to c. $3m over the previous six quarters (see the chart below). The sales growth was an impressive 88% sequentially and 130% year-over-year. The significant jump in revenues allowed e-Boost to reach positive operating income (before corporate overheads) for the first time since the product line was launched in late 2021.

PPSI’s management expects Q4 to be even stronger, with $8m to $10m in quarterly revenues, based on the company’s guidance of $21m to $23m in 2024 revenues. Given the company’s significant backlog ($24m as of September 2024) and the fact that we are halfway through Q4, I would expect the company to meet the Q4 and 2024 guidance, barring, of course, any unexpected delays in customer order fulfillment. Just to reiterate the impressive growth rate, I would highlight that the midpoint of management’s 2024 revenue guidance implies 100% year-over-year revenue increase. So, I think it is reasonable to conclude that after flat e-Boost performance in recent quarters/years, the business’s operational performance has inflected.

And 2025 is shaping up to be another year of rapid revenue growth, with management guiding for $27m-$29m in annual revenues, implying 27% year-over-year growth. During the call, management highlighted that around $17m of the 2025 revenues will come from the sale and rental of equipment, while the remaining c. $10m will come from related services and maintenance. Again, considering PPSI’s significant backlog and strong demand outlook, I would expect the revenue target to be met.

Now, at this point, you could argue: "Okay, revenue growth is solid, but what about profitability? After all, PPSI’s e-Boost is still unprofitable given its small scale." Here, I would highlight that the company seems to be on the cusp of reaching profitability. During the conference call, management stated that it expects PPSI to reach profitability in 2025 based on the guided revenues, albeit the company did not provide any profitability estimates. Here’s my attempt to estimate how PPSI’s EBITDA might look in 2025:

$28m in midpoint 2025 revenues.

Less $18m in cost of goods sold. Here, I assume 35% gross margins. While PPSI did not explicitly provide a gross margin target, during the conference call, management mentioned that it generated 35% margins on one of the recent e-Boost orders. While this gross margin is above that of the e-Boost business in Q3’24 (24%), PPSI’s divested e-Bloc segment margins have generally stood at similar levels (e.g., 32% in FY23). I would highlight that e-Boost, in addition to equipment sales, has had a significant service and maintenance revenue component, as opposed to e-Bloc, whose revenues have come mostly from equipment sales. Another aspect is that e-Boost equipment sales include equipment rentals/leases, including via the partnership with SparkCharge. So, I think using 35% gross margins is reasonable until management provides more definitive guidance.

Less $7m in SG&A expenses. This includes 1) e-Boost segment’s SG&A expenses of $4m and 2) $3m in unallocated corporate overhead. The e-Boost segment’s SG&A expenses are in line with those seen in recent quarters while the corporate overhead estimate is based on management’s guidance of 12% of revenues.

With these assumptions, I arrive at $3m in 2025E EBITDA. Pro-forma for the proceeds from the e-Bloc divestiture, the RemainCo is currently valued at $16m, implying a 6x EBITDA multiple. I think this is an undemanding valuation considering e-Boost’s impressive recent growth. I would also highlight that the more mature, slower-growth e-Bloc business was divested at 11x 2023 EBITDA.

And PPSI’s 2025 revenue guidance might prove to be too conservative. Why? Well, I would first note that during the previous conference call in October, PPSI’s management hinted at $32m in 2025E revenues, although management was quick to clarify that this does not represent actual guidance. While this is speculation on my part, it is possible that management could have subsequently provided a more conservative guidance range together with Q3 earnings.

Another reason why the revenue guidance might be conservative is the significant further growth runway for PPSI. Despite the slowdown in EV adoption in the U.S., EVs remain a fast-growing market (see here), so it’s safe to say that demand for mobile charging stations will continue to grow. During the conference call, management highlighted strong demand from the electric bus end-market while hinting that there could be incremental demand from package carriers that have so far been “not so active in making final decisions on charging” (see the quote below). There is also growth potential with the launch of new products. I would note here that PPSI intends to launch HOMe-Boost, an EV fast-charging unit for homeowners, in early 2025. So, overall, I would expect PPSI’s backlog to continue growing, potentially allowing the company to outperform its 2025 guidance.

It's really all of it. Some are repeats. A lot of it is the segment that's being driven by government or quasi-government. So, it's state, city, municipalities, both for electric buses moving the city buses, as we call them, or school bus related, however that particular purchase order comes to us. Those are the big drivers. And I guess the group that's been very active in trying to determine what they do going forward, but not so active in making final decisions on charging is the package carriers. So, the big Alphas, the Amazons, FedEx, DHL, Postal Service, they've taken in a lot of electrical vehicles, vans, truck, every form really have been a big appetite for that. Haven't made so many charging solutions choices. And we see that unfolding stronger for us in 2025, indeed going into '26. Geo, do you want to add or edit anything that I said?

So, these are my quick thoughts on PPSI post-Q3 earnings. The company remains inexpensive pro-forma for the divestiture, trading at below 1x 2025E revenues and c. 6x EBITDA. I think these are undemanding multiples for what is a high-growth business with plenty of growth runway and nearing profitability.

With the investment thesis intact and significant further upside, I continue to think the setup is compelling and have thus maintained my position.

Excellent update!

Are you concerned at all about the hybrid market eroding EV sales?