September Portfolio Review

An overview of active Idea Hive portfolio positions

With September in the books, I am sharing the monthly portfolio review. This post provides an overview of the Idea Hive portfolio, including key information on each position, such as elevator pitches and performance to date. The article also covers recent updates on each portfolio name and their impact on the underlying investment theses. The aim of this post is to quickly recap the latest developments for each idea and highlight why the portfolio names continue to present attractive investment opportunities.

Without further ado, let’s dive right in.

Portfolio Review

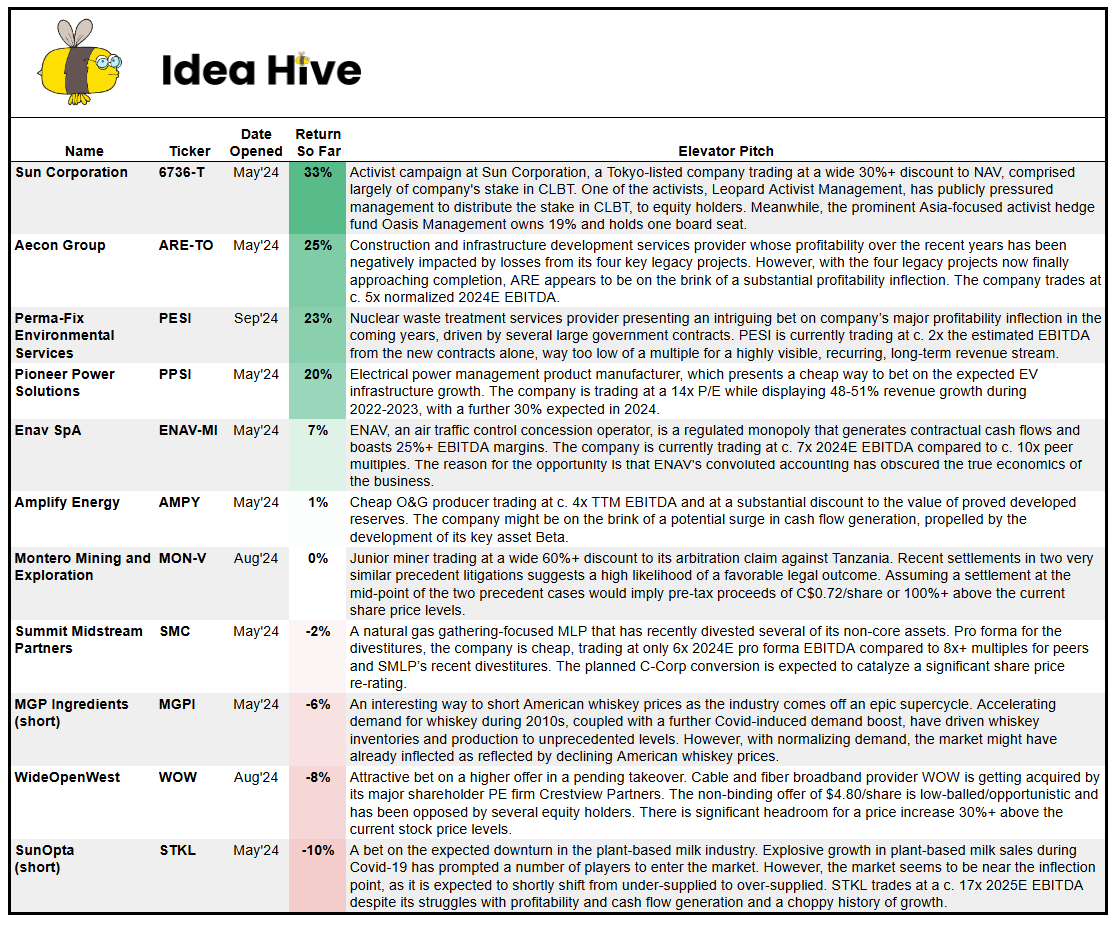

Here’s the Idea Hive portfolio as of October 2:

In early September, I introduced a new idea to the portfolio, PESI. As for the other active portfolio ideas, there were few significant updates during the month. I would highlight the updates on PPSI and WOW, which I covered in an article published in mid-September.

Most portfolio names are currently hovering near their entry price levels. Nonetheless, several ideas have performed well since I added them to the Idea Hive portfolio, including 6736-T (+33% for hedged positions), ARE-TO (+25%), PESI (+23%) and PPSI (+20%).

Portfolio Idea Updates

Below is a list of recent updates and thoughts on active Idea Hive portfolio positions.

Sun Corporation (6736-T)

Sun Corporation’s share price has been on an upward trajectory, despite no recent material updates, and is up 17% over the last month. This, coupled with a flat CLBT share price during September, has reduced the discount to NAV from 59% at the time of the write-up to 31%. Despite the lower margin of safety, I still believe Sun Corporation remains an attractive “discount to NAV + pressure from several activists” setup. With PE firm True Wind Capital recently joining two other activists, Leopard Asset Management and Oasis Management, on Sun’s shareholder register with a sizable 19% stake, I continue to expect some form of value realization that could help close the discount. While True Wind’s playbook is not yet known, Leopard has previously pushed for a distribution of Sun’s stake in CLBT to equity holders. Another option might be an outright sale of CLBT to a third party. Either scenario would likely imply a 30%+ upside from current levels.

Aecon Group (ARE-TO)

ARE’s legacy projects are moving towards completion. I would highlight Komrade Kapital’s recent update on ARE, which discusses the ongoing progress in two of ARE’s three remaining legacy projects: Finch LRT and Eglinton LRT. Both projects have recently seen a significant ramp-up in driver training, a key remaining milestone before completion. With these two projects expected to be completed in late 2024-early 2025, ARE will inch closer to showcasing its normalized earnings power. While there is still a chance that ARE might record additional write-downs related to the remaining Gordie Howe International Bridge project (expected to be completed in Q3 2025), these impairments are likely to be one-off and much smaller than previous ones, as previously indicated by management. While ARE share price has continued to rise recently, the company remains cheap, trading at 4.9x TTM normalized EBITDA, significantly below the 9x+ multiples at which its peers trade. Aside from the completion of the legacy projects, another potential catalyst for closing this valuation gap could be the ramp-up of the ongoing share buyback program, as the stock repurchases since August have so far been rather underwhelming (c. 0.02% of outstanding shares bought back). I will be waiting for Q3 2024 results, scheduled for October 31, to update the normalized EBITDA estimate and company’s valuation.

Perma-Fix Environmental Services (PESI)

Highlighting my write-up on PESI from early September. Despite the increase in share price since I published the pitch, I continue to think that the setup remains highly attractive. Given the contracted and expected volumes of nuclear waste from the decommissioned Hanford site that PESI will treat, company’s annual revenues are likely to more than triple starting in 2026. With reasonable incremental margin assumptions, the company is likely to generate c. $110m in annual EBITDA, compared to the current EV of c. $200m, from Hanford-related contracts alone. I believe that 2x EV/EBITDA is far too low a multiple for a highly visible, recurring, long-term (10+ years) revenue stream. I would expect PESI to re-rate to a more appropriate multiple, say 8x, when the company begins fulfilling these contracts, likely in the back half of 2025.

Pioneer Power Solutions (PPSI)

PPSI continues to make progress on the restatement of its financials. In mid-September, the company filed its Q1 2024 financials and stated that it expects to file the Q2 report “in the coming weeks.” This expected filing will finally bring the company current with its financials after a series of historical restatements, starting from Q1 2022, due to revenue and cost recognition errors. As for the reported Q1 results, the quarter was mediocre, with revenues flat year-over-year, though this was not unexpected given previously indicated order timing and production capacity constraints in the e-Bloc business. While Q2 is likely to be stronger, I am not confident in a marked improvement in operational performance given the same order timing and capacity issues. Nevertheless, after a weaker Q1 and possibly Q2, PPSI is well-positioned for substantial revenue and earnings growth in H2 2024 and 2025. This seems reasonable, given that PPSI’s customer order backlog stood at $46m as of March, while in late/post-Q2, the company announced over $20m in new customer orders (compared to $41m in TTM and $52-$54m in 2024E revenues). So, while PPSI reiterated its 2024 guidance in the press release, given the large backlog, there’s a good chance the revenue outlook may prove overly conservative. PPSI’s share price has jumped since the latest announcement and the stock currently trades at a 15x 2024E P/E compared to a 12x multiple at the time of the write-up. Nonetheless, given the likely conservative guidance and the ample growth runway for company’s key product lines, I think this valuation is modest.

Enav (ENAV-MI)

There have been no material updates on ENAV over the past month. The investment thesis remains unchanged: ENAV is an undervalued air traffic concession operator poised for a re-rating as it is reimbursed for the negative impacts of 1) traffic declines due to COVID in 2020-2021 and 2) higher-than-expected inflation in 2022-2023. Adjusted for the cash owed to the company by airlines, ENAV is currently trading at 6.8x 2024E EBITDA. This valuation is too low considering that ENAV is a regulated monopoly generating contractual cash flows and boasting 25%+ EBITDA margins. It is also significantly below the average multiple of c. 10x for other European airport concession operators and Italian utility companies. I’d expect ENAV shares to re-rate much closer to peer multiples as the company continues to recover accrued payments. Even a modest re-rating to, say, an 8x multiple would imply 20%+ upside from the current stock price levels.

Amplify Energy (AMPY)

Nothing new to update on AMPY aside from some stock price volatility driven by the recent decline in crude oil prices. I continue to believe AMPY presents a compelling setup. The company is cheap trading at 3.4x 2024E EBITDA and 7.5x FCF. I would highlight that the majority of AMPY’s forward sales are hedged (over 70% and 55% of 2024 and 2025 oil production, respectively), so short-term oil price fluctuations will have only a marginal impact on near-term profitability and cash flow generation. Most importantly, the setup remains catalyst-rich, given the potential Bairoil asset divestiture and new well drilling at Beta. I would expect the company to announce the Bairoil divestiture in the coming months/quarters. A potential divestiture at a 50% discount to Bairoil’s PV-10 value would allow AMPY to repay the majority of its net debt and/or initiate a large capital return. As for the new well drilling at Beta, if the program continues in line with recent results, the Beta development might alone be worth more than AMPY’s current EV. I believe the market currently ascribes minimal value to the Beta development, and so I would expect a stock re-rating if/when the FCF generation potential becomes more certain.

Montero Mining and Exploration (MON-V)

I recently came across several interesting bearish arguments against Montero on the Special Situation Investments blog. I would highly recommend reading the discussion on the blog, which includes my refreshed thoughts on the setup. To summarize, the pushback revolves around the basis for the claim in the precedent IDA litigation and its implications for MON’s pending arbitration against Tanzania. Analysis of IDA’s award suggests that Montero’s claim of C$90m might be overly optimistic, as the ‘claim / sunk cost’ ratio is higher than that applied in IDA’s litigation. Assuming the tribunal applies the same multiple as in the IDA case, I arrive at a ‘realistic’ claim value of C$43m. This implies that MON is currently trading at a 62% discount to the ‘realistic’ claim, compared to an 82% discount to the C$90m claim. While the risk-reward is less compelling, I still believe MON remains an attractive setup. Accounting for potential litigation funding fees, MON is trading at a 40% discount to the ‘realistic’ claim value, while IDA settled broadly in line with its initial claim value. The IDA precedent, along with MON being represented by the same legal team, provides some confidence that there remains significant upside in a base case scenario. MON’s insiders and equity holders seem to agree, as indicated by the recent placement anchored by activist Jeremy Raper and a sizable options package granted to management above current stock price levels.

Summit Midstream Partners (SMC)

SMC recently announced the acquisition of Tall Oak’s natural gas midstream assets for $155m in cash and stock, with the total consideration around $450m. My earlier prediction that management would be highly selective with acquisitions, given their solid track record, has proven accurate. The transaction seems value-accretive, priced at 5.6x 2025E EBITDA (estimated at $80m) for what will likely be one of SMC’s higher-quality assets, with an average customer contract life of c. 13 years. Most importantly, the acquisition will reduce SMC’s net leverage from 4.4x to 3.8x, positioning the company to finally initiate capital returns. In the press release, management has suggested that they will “consider returning capital to shareholders, for example, through preferred dividends, common dividends, and/or share buybacks starting in 2025.” On a pro forma basis, SMC remains cheap, trading at 7.1x 2025E EBITDA, compared to peer multiples of 8x-10x. I would expect this valuation gap to narrow, driven by the potential dividend reinstatement and/or stock buybacks coupled with the continuing influx of institutional investors following the recent C-Corp conversion. With SMC trading at a low multiple and several catalysts on the horizon, I continue to like the setup.

MGP Ingredients (MGPI)

There have been no updates from MGPI over the last month, though I would highlight that in late August, branded alcoholic beverage peer Brown Forman reported a sizable 5% decline in whiskey sales in the most recent quarter. Another interesting data point is that 2023 marked the first time this millennium that American whiskey consumption in the U.S. declined in volume terms (although consumption in dollar terms was up slightly due to ongoing premiumization trends). I think these are further indications that the industry might be on the cusp of a negative inflection, amidst historically high supply and normalizing consumer demand following the pandemic-driven boom. The potential upside, if this negative inflection materializes, could be significant. A potential re-rating from the current EV of $2.1bn to the tangible book value of $0.3bn—still above where MGPI traded before the industry upcycle—would imply potential upside of 80%+. With the investment thesis intact and large potential upside, I continue to believe MGPI is an attractive short opportunity.

WideOpenWest (WOW)

We recently saw another positive valuation reference point for WOW’s pending takeover with VZ’s acquisition of DSL/fiber broadband provider FYBR. I discussed the transaction and its implications for WOW’s valuation in mid-September. The transaction valued FYBR at 8.8x 2024E EBITDA (compared to WOW’s current valuation of 5.2x TTM EBITDA). While comparison is not entirely straightforward, given FYBR's mix of legacy DSL and fiber assets, the transaction directionally highlights the value of WOW’s fiber assets. Valuing WOW’s fiber asset at a slight discount to the implied valuation of FYBR’s fiber assets suggests an incremental value of $3.80/share (versus the offer price of $4.80/share). So, if the buyer consortium does not increase the offer for the existing business but simply pays up for WOW’s fiber assets, we could potentially see an improved offer 50%+ above current stock price levels. Despite the positive valuation reference point, WOW stock has barely reacted and remains roughly in line with the write-up levels. Considering the ample headroom for a higher offer, I would expect both sides to come to terms on a price bump, likely in the coming weeks or months.

SunOpta (STKL)

STKL has jumped by nearly 20% over the last month, with no news or announcements from the company, and is currently up 27% since the earnings release in August. Despite the market’s optimism, I continue to believe that STKL remains an attractive short opportunity. With ongoing post-Covid demand normalization and new supply entering the industry in the near term, it is likely that the industry will soon shift from undersupplied to oversupplied. This is expected to drive a deterioration in STKL’s pricing and, thus, topline/margins in the coming quarters. I intend to reassess the setup after STKL and peer OTLY release their Q3’24 results, likely in early November. For now, I continue to think that STKL remains a compelling short and thus have maintained my position.

List of Active Portfolio Ideas

Below you can find links to the initial pitches and latest update posts for each active portfolio idea.

Sun Corporation (6736-T) — initial post here, last update here

Perma-Fix Environmental Services (PESI) — initial post here

Pioneer Power Solutions (PPSI) — initial post here, last update here

Montero Mining and Exploration (MON-V) — initial post here

Summit Midstream Partners (SMC) — initial post here, last update here

MGP Ingredients (MGPI) — initial post here, last update here

Can't believe this is a free substack.

Great review post, clear and easy to understand. Thanks