Post-Earnings Updates on Two Ideas

Updates on AMPY and STKL

With earnings season in full swing, I’m sharing updates on two portfolio names, Amplify Energy (AMPY) and Sunopta (STKL). The update on AMPY is highly positive, whereas I’d consider the recent earnings from STKL more mixed, but nonetheless I believe the investment thesis remains on track.

Amplify Energy (AMPY) — initial post here, last update here

Let’s start with AMPY.

For those unfamiliar with the setup, here’s an excerpt from my recent deep dive on the company, summarizing the investment thesis:

AMPY is an oil and gas producer that presents an attractive way to invest in the energy space. The company is currently trading at approximately 5x EBITDA and 10x FCF. These are undemanding multiples for an O&G company with low-decline and long-reserve-life assets that have consistently generated cash flow in recent years. The company is also trading approximately 50% below the estimated value of its proven developed reserves. Beyond its current production and proven reserves, AMPY’s cash generation might be on the cusp of an inflection point due to the recent development of its key world-class oilfield asset, Beta. If successful, new well drilling at Beta could create incremental value multiples above the current share price.

AMPY recently reported Q2’24 results. There were three key aspects from the earnings release that need to be highlighted:

The company continues to display steady operational performance, with management slightly raising guidance for this year.

The Bairoil divestiture process is ongoing, with the company reporting interest from multiple third parties.

AMPY successfully completed the drilling of a new well at Beta, with production exceeding company’s previous expectations.

While all of these aspects support the investment thesis, the most significant positive development was the success of the new well drilling at Beta. I will expand on that a bit more.

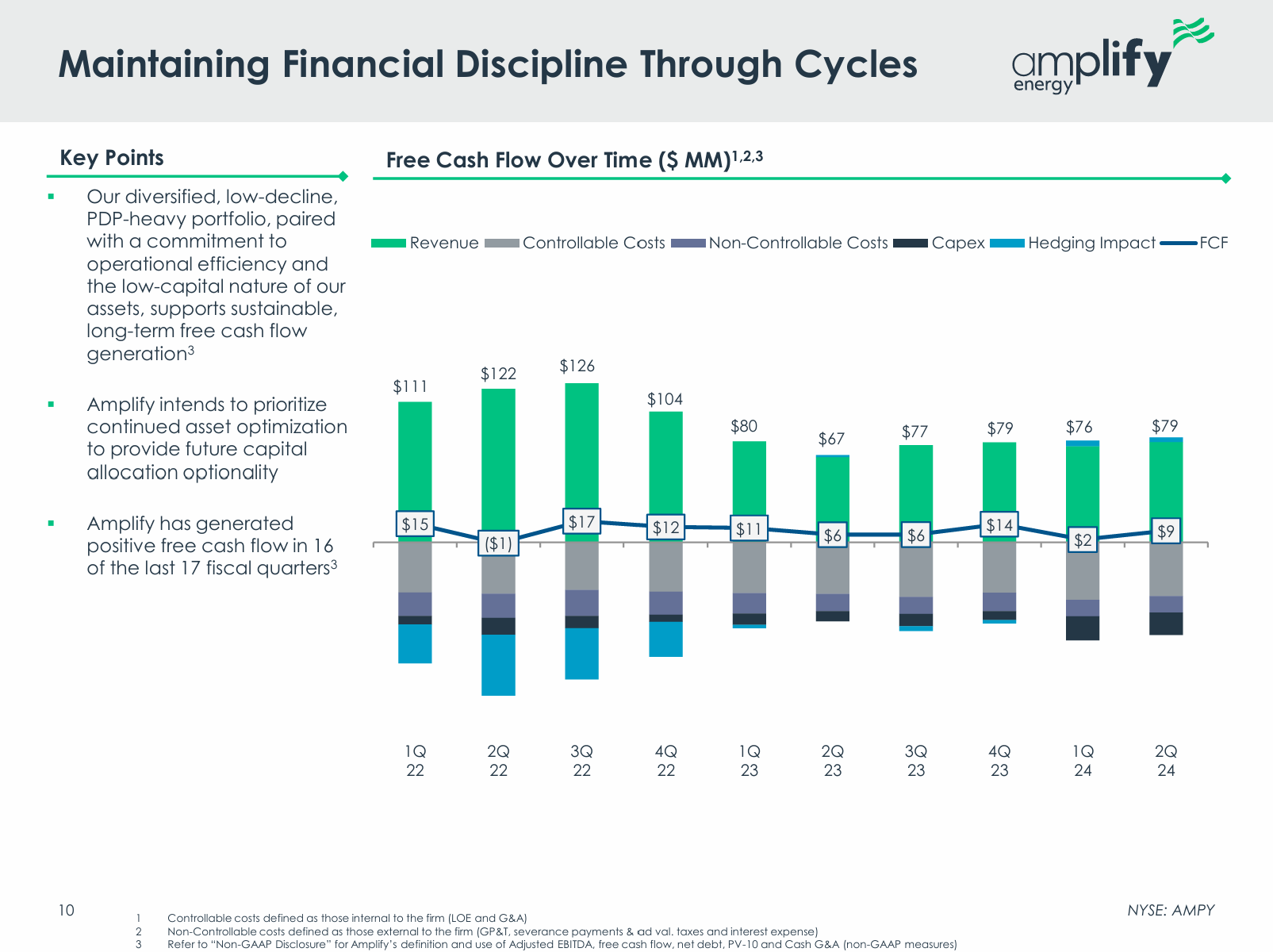

But first, let’s take a quick look at the operational performance. Q2 was another solid quarter for AMPY, given steady production volumes across most of company’s assets. AMPY continues to generate significant cash flows/EBITDA, with $9m in quarterly FCF ($32m TTM) and $31m in EBITDA ($100m TTM). Both are pretty sizable for a sub-$300m market cap (c. $400m EV) company.

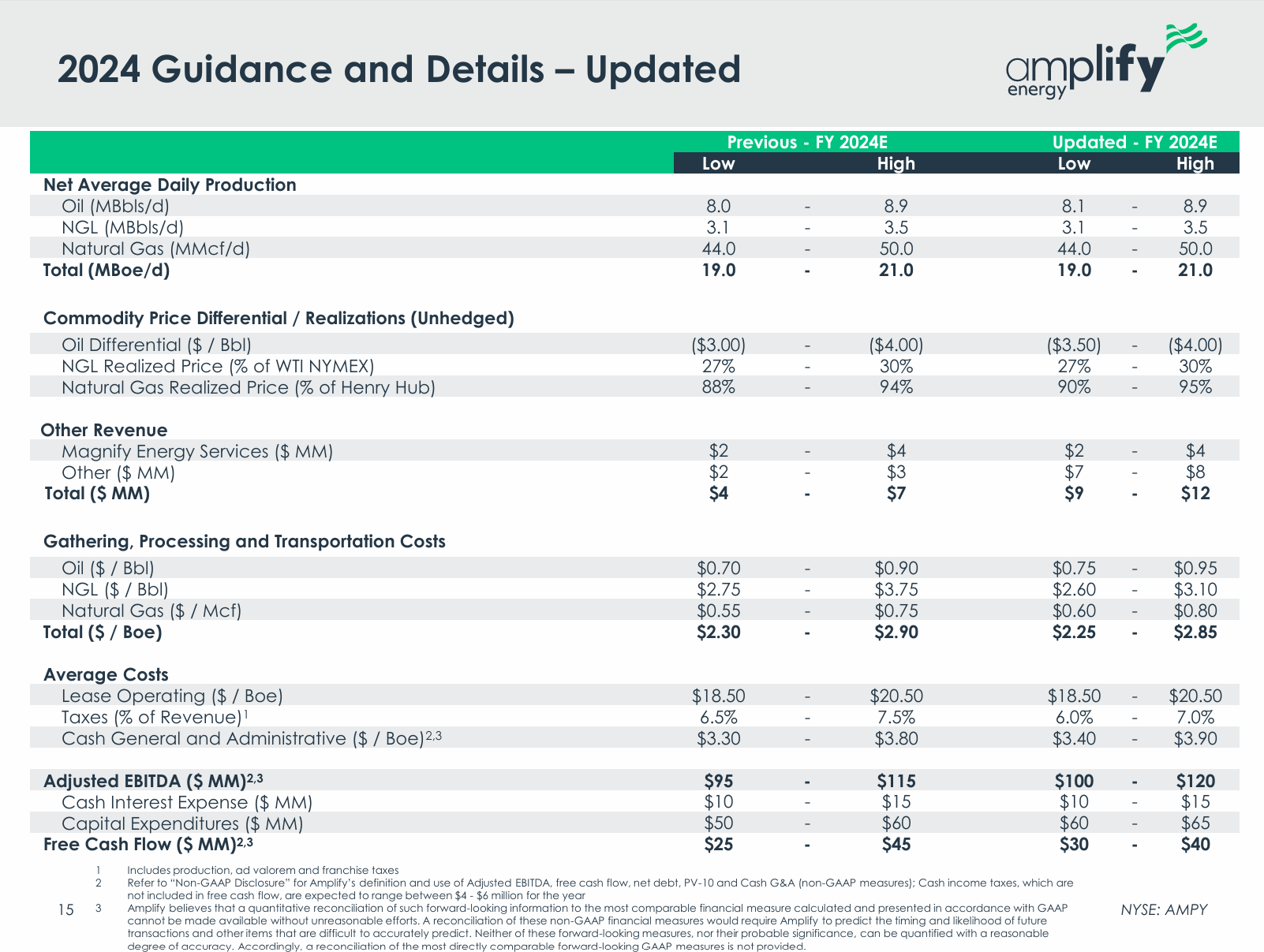

As for the outlook, management has raised its 2024 EBITDA guidance due to stronger-than-expected Q2’24 performance. Note that the company has high visibility into its projected EBITDA/cash flow generation, given that the majority of oil and natural gas production for the coming years is hedged. AMPY now also expects slightly higher capital expenditures due to participation in drilling activities in two non-operated assets, which are expected to provide incremental cash flows in early 2025.

Moving on to the potential Bairoil divestiture. In the earnings release, management provided an update, stating that the process is ongoing as the company has received multiple bids “for an outright sale and partial monetization.” While no further details regarding the divestiture process and timeline were shared, AMPY’s management previously stated that the monetization was expected to be completed “over the summer.” This suggests that we might see the process conclude in the coming weeks.

You might recall from my deep dive on AMPY that potential monetization, even at a steep 50% discount to Bairoil’s PV-10 value, would imply net proceeds of c. $70m. This would allow the company to either pay down the majority of its net debt and/or pay out a large special dividend. During the conference call, management confirmed that dividends and stock buybacks are both “certainly on the table” if/when the Bairoil asset is sold/monetized (see the quote below).

But the big news from the earnings release was related to new well drilling at Beta.

As a quick refresher, earlier this year, AMPY initiated a new well drilling program, intending to drill four new wells this year. In May, the company reported equipment issues related to the drilling of the first well, which had been delayed until late this year.

Together with its Q2 earnings, AMPY announced that it successfully completed the drilling of another well "on time and under budget." The drilling results were significantly above management’s previously outlined expectations. The company reported peak production rates of 730 bpd, with production "in excess of" 650 bpd after two months. This is substantially above the initially guided 350 bpd for the first year of production. Meanwhile, total capital costs were $4.2m, compared to the initially estimated $5m-$6m per well. AMPY's management now expects the well to pay out in approximately four months, compared to the previously guided payback period of one year.

The company intends to drill two wells in Q3 before returning to the drilling of the first well (which faced equipment-related issues) “later this year.” During the conference call, AMPY’s management highlighted that it might accelerate the pace of new well development in 2025, pending further new well drilling results this year (see the quote below).

I think this is a very positive development for the investment thesis, for several reasons:

Successful new well drilling indicates that the previous equipment-related issues have been resolved and are unlikely to reoccur.

More importantly, the drilling results highlight the incremental FCF generation potential of the new wells, now even higher than expected previously.

Let me expand a bit on the second point. Company’s reported capital costs per well and guided payback period suggest that the company could generate around $32m in first-year FCF if four new wells are drilled. Assuming successful near-term drilling results, the company might opt to expand the development program to 12 wells per year, the maximum capacity allowed by the current infrastructure. In this scenario, investors might potentially be looking at $200m+ in incremental annual FCF several years down the road, or around half of company’s current market cap/EV. Needless to say, such incremental FCF would imply a multi-bagger upside from the current stock price levels.

AMPY shares have jumped significantly (by 16%) since the earnings release, reflecting the market’s positive reaction to the Beta development progress. However, I still do not think the c. $40m increase in AMPY’s market cap is large enough given the improved Beta development potential. I’d expect a further stock re-rating as AMPY continues to successfully drill new wells while the market becomes increasingly aware of the FCF inflection potential.

With the investment thesis working out well so far, I continue to think that AMPY presents a compelling investment opportunity, and I have maintained my position.

Sunopta (STKL) — initial post here, last update here

Let’s move on to another portfolio name, Sunopta.

For those unfamiliar with STKL, here's a high-level summary of the "short" investment thesis shared in the last update:

STKL offers a way to bet on the anticipated downturn in the plant-based milk industry. Historically under-supplied, the market saw explosive growth in demand during the pandemic, prompting a significant increase in production capacity. The crux of the investment thesis is that, with the increased production capacity and normalizing demand, supply is expected to finally outstrip demand. This is likely to lead to lower prices and negatively impact producers’ growth and margins.

A few days ago, STKL reported its Q2 earnings.

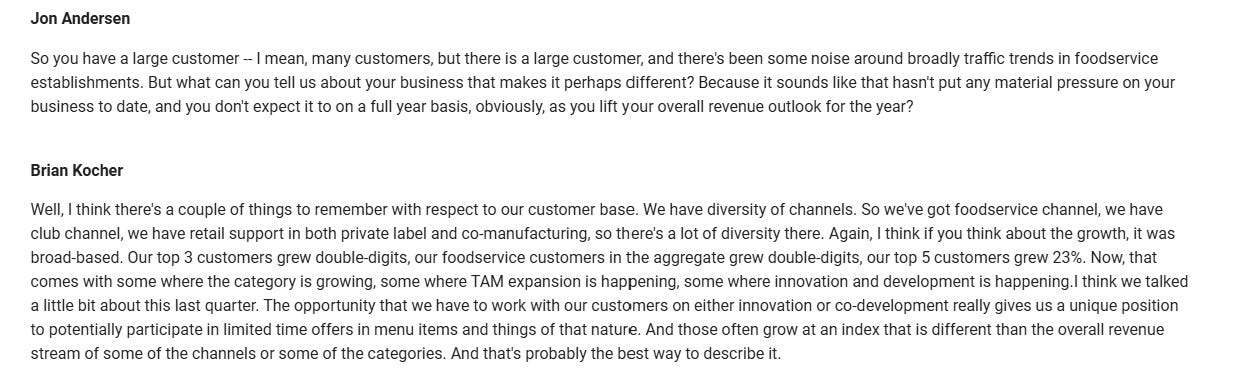

Let’s dive into the operational performance. During the quarter, STKL displayed solid performance driven by significant product volume growth (+27% year-over-year). This was largely propelled by continued strong demand in the foodservice (i.e., coffee shop) channel, despite broader weakness in the channel (see the exchange from the conference call below). As you might recall from my previous posts, management has repeatedly described foodservice as much larger and more important than the remaining retail/tracked channel. Strong performance in foodservice has led to strong growth across key financial metrics, with STKL’s revenues and EBITDA up 21% and 12%, respectively.

During the conference call, STKL highlighted a positive outlook for the remainder of this year, expecting mid-single-digit growth for plant-based milks in the U.S. across all channels. The company has raised its 2024 revenue guidance, while the EBITDA target was reiterated (see below).

So a quick look at the key quarterly financials/outlook indicates that the earnings were solid, with strong volume growth seemingly indicating robust demand for plant-based milk. STKL's share price has jumped by 13% since the earnings release, reflecting the market’s positive view of the results.

However, there are several other details from the earnings release that, in my view, confirm the looming negative industry inflection.

The key point to note is the continued decline in product pricing. As shown in the chart below, STKL’s pricing remained firmly in negative territory during the quarter, following the trend that began in Q1. Given that pricing was consistently high/positive during 2022-2023, this appears to be a clear indication of the ongoing negative industry inflection.

Another notable aspect was the decline in company’s margins across the board (e.g., adjusted gross margins were down from 17% to 16% year-over-year). The fact that STKL suffered from margin decline despite strong volume growth highlights the competitive/pricing pressures faced by the company. The divergence between revenue growth and margin decline was rightly pointed out by one of the analysts during the conference call (see the quote below). Management, in turn, explained this disparity with supply chain inefficiencies that are expected to be addressed with "short-term investments." However, the potential impact of these investments on profitability has not been specified. One interesting data point from management was that the “overall cost per unit” decreased compared to Q2’23. Given the declining gross/EBITDA margins, this might indicate that the cause of the margin weakness lies primarily in pricing rather than on the cost side of operations as argued by management.

On a quick tangent, STKL peer OTLY’s recent Q2’24 results seem to confirm the short thesis. As you might recall from my posts, OTLY and STKL are the two largest players in the plant-based milk markets in terms of revenue and capacity. While OTLY’s North American revenues grew at a solid 10% clip in the quarter, the growth was largely driven by volume, with pricing up by only 1.4%. Note that OTLY produces primarily oat milk, a category that has been growing significantly faster than other plant-based milk subsegments (as opposed to almond milk for Sunopta). So, high exposure to oat milk has likely been a tailwind for OTLY’s pricing. My point here is that the pricing pressure faced by two of the largest plant-based milk producers suggests the industry might be on the cusp of a negative inflection.

And it seems that pricing pressures will only intensify going forward, given that additional supply is slated to enter the industry in the near term. During the conference call, STKL’s management reiterated plans to bring on additional supply capacity in H2’24. Aside from the recently completed oat extraction expansion at the Modesto, California facility, new capacity is expected to come from the continued ramp-up of the third manufacturing line at the Midlothian, Texas plant (see the quote below).

While the potential supply capacity increase from the Modesto plant expansion has not been detailed, as I noted in my deep dive on STKL, the third manufacturing line in the Midlothian facility might bring on c. 100m liters of annual capacity. As you might recall, total industry demand was estimated at 1,278m liters annually, while total supply (excluding the Midlothian third line) was around 1,150m liters. Given the anticipated Midlothian Line 3 ramp-up, coupled with OTLY’s expansion of its Millville facility (around 100m incremental liters, expansion was announced last year), I’d expect the industry to tip solidly into oversupply by the end of 2024.

So, that’s my read of the earnings release. I continue to believe that, despite solid revenue and volume growth, the investment thesis is on track as we are likely close to (or possibly beyond) the point of negative inflection in the industry.

Let's now quickly reassess where we stand from a valuation perspective. STKL is currently trading at 14.4x TTM and 11.2x 2024E EBITDA. I continue to believe that 2024 EBITDA ($90m vs. $70m TTM) is not representative of the company's normalized earnings power, as its topline is likely to be pressured in the coming quarters/years due to an impending industry inflection. But even on the likely elevated 2024E EBITDA, the valuation multiple seems too high for a business that has consistently struggled with profitability and cash flow generation, has a choppy growth history, and operates in an industry expected to face a downturn. A more reasonable multiple, say 9x, would imply a share price target of around $4.3/share, suggesting 30%+ upside for short positions.

With the investment thesis intact, I think that STKL remains an attractive short investment opportunity and is a "Maintain" for now.