Latest Thoughts on SMC

A discussion of Q2 results, valuation and potential catalysts

Summit Midstream Corporation (SMC) — initial post here, last update here

In this post, I’m sharing a quick update on Summit Midstream given several recent developments, including 1) the recently completed C-Corp conversion and 2) the subsequent Q2’24 results. Note that after the conversion, the stock is now trading under the new ticker “SMC.”

For those unfamiliar with the investment thesis, SMC is a natural gas gathering-focused MLP that recently divested several non-core assets. After these divestitures, the company is trading at c. 6x estimated 2024 EBITDA, which is significantly below the 8x+ multiples where peers are trading and the 10x+ multiples for comparable industry transactions. Several near- to medium-term catalysts could help the stock re-rate, including a potential dividend reinstatement and/or a company sale.

Starting with the C-Corp conversion, which was completed on August 1. As you will recall from my previous updates on SMC, the conversion is expected to lead to increased trading liquidity and potential index inclusion, both of which could put upward pressure on the stock price. While SMC’s share price surged to over $40/share on the day of the conversion, this increase was short-lived, as the stock has since retraced to around pre-conversion levels. However, I don’t think this suggests that the reorganization has failed to catalyze a stock re-rating; it will likely take some time for the substantial influx of new institutional/index investors to fully materialize. So I’d expect the C-Corp conversion to create upward pressure on the stock price over the coming months.

Moving on to the Q2 results, company’s performance was broadly in line with management’s expectations and previous trends. During the quarter, the company generated EBITDA of $43m, which was roughly in line with Q1’24 and Q2’23. This stable performance was driven by company’s ex-Double E assets (Barnett, Piceance, and Rockies), which mostly displayed flat average daily throughput.

As for the outlook, management reiterated its 2024 EBITDA guidance of $170m-$200m. The company expects strong performance in the Rockies and Barnett segments for the remainder of the year (see the quote below), driven in part by “a more supportive natural gas price environment forecast for late 2024 and 2025.”

But perhaps the more important takeaway from the earnings report is that SMC continues to ramp up its crown jewel asset, Double E.

As a reminder, Double E is a natural gas transmission asset located in the Delaware Basin (part of the Permian Basin). Double E has a transmission capacity of 1.35 Bcf/d, with over 1 Bcf/d already committed under long-term contracts, a large portion of which is expected to come from the anchor customer, Exxon Mobil.

During Q2, Double E’s average daily throughput increased from 467 Bcf/d in Q1 to 549 Bcf/d. This marks yet another quarter where SMC has rapidly grown the volumes transmitted through Double E. For reference, average daily throughput stood at 386 Bcf/d in Q4’23 and 327 Bcf/d in Q3’23.

Double E’s EBITDA contribution is still admittedly insignificant (see the table below, Double E is included under the Permian segment). However, given the already contracted capacity, I’d expect the asset’s EBITDA generation to continue growing rapidly in the coming quarters/years. During the conference call, management highlighted that it expects to fill up the contracted capacity “in the near term” while also stating that it is in “advanced discussions” to sign contracts for the remaining capacity (see the quote below).

The continued ramp of Double E is a strong positive for the investment thesis. SMC’s management has previously stated that at full capacity, company’s share of Double E’s EBITDA would be $45m, implying a near doubling of SMC’s current EBITDA. Note that the company has the option to expand Double E’s capacity to 2 Bcf/d. SMC’s management expects this potential expansion to increase the asset’s EBITDA contribution to $60m.

So that’s my take on the Q2 earnings. I believe the earnings release supports the investment thesis as it shows that 1) the ex-Double E business continues to display stable operational performance, and 2) SMC continues to ramp up volumes at Double E, its crown-jewel asset.

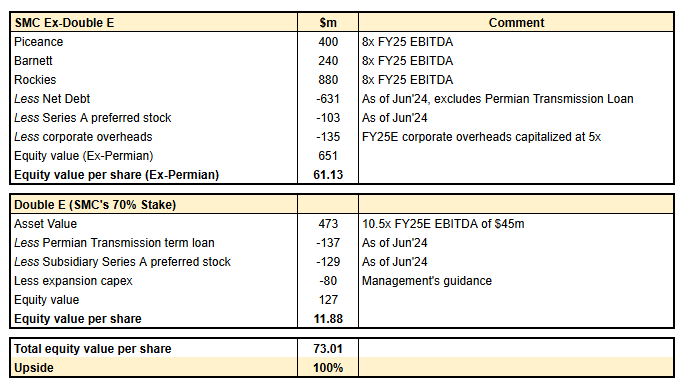

Let’s now briefly discuss where we stand from the valuation perspective. As shown in my updated SOTP valuation table below, SMC continues to trade at a wide discount to its estimated equity value excluding Double E (c. $61/share). I’d note that the 8x multiples used for the valuation of ex-Double E assets are at the lower end of peer valuations. Nonetheless, even with conservative 7x multiples, the equity value excluding Double E would stand at $43/share, or c. 20% above the current stock price levels.

As for Double E, applying a 10.5x multiple (in line with comparable industry transactions) to the estimated EBITDA at full current capacity would imply an incremental equity value to SMC of c. $130m or $12/share. This indicates that the value of SMC’s stake in Double E could potentially cover a significant portion of company’s current market cap.

In addition to the expected positive impact of the C-Corp conversion, another potential catalyst could help the shares re-rate: a potential dividend reinstatement. Last month, SMC refinanced its capital structure by issuing new debt totaling $1.1bn due in 2029, leaving the company with no significant near- to medium-term debt maturities. As I noted in my previous update on SMC, this will bring the company one step closer to a potential dividend reinstatement. During the conference call, management highlighted that the other hurdle to reinstating distributions is reaching a leverage target of 3.5x versus 4.4x as of Jun’24 (see the quote below). With continuing cash flow generation, I’d expect the company to reach this target over the coming months, allowing it to reinstate both common and preferred distributions.

Given the significant potential upside and several near- to medium-term catalysts, I continue to like the SMC investment setup and have thus maintained my position.

nicely done. Are the preferred listed? Thanks.