Latest Thoughts on HCC Post-Q3 Earnings

Despite the recent jump in the share price, the setup remains attractive.

Warrior Met Coal (HCC) — initial post here

In this post, I’m back with my latest thoughts on one of my portfolio positions, HCC, following the company’s Q3 results reported last week.

First, for those unfamiliar with the investment thesis, I would highly recommend my four-part series on the met coal industry. The first article outlines the broader case for investing in the met coal industry, while the second discusses what makes the sector an interesting investment opportunity at this time. The third and fourth posts delve into stock selection criteria and explain why HCC is the most attractive way to play the industry. To summarize, the outlook for met coal producers over the coming decades is favorable, given the limited new supply capacity expected to come online, while demand for met coal will likely grow or remain stable in the years ahead. As for what makes met coal an appealing sector now, the historical relationship between met coal prices at market bottoms and marginal production costs suggests we might currently be at a downturn in the market. Regarding HCC specifically, the company boasts the lowest cost structure and the highest share of low-volatility coal in its production mix. On top of that, HCC is currently developing Blue Creek, one of the few large met coal assets coming online in the U.S.

Here are my key takeaways from HCC’s Q3 earnings:

As expected, price realizations were weak in Q3 as met coal producers continue to navigate a downcycle environment.

The development of Blue Creek is progressing, with work on the first longwall panel starting during the quarter.

Let’s unpack these points in a bit more detail.

Starting with operational performance: as anticipated, HCC experienced weak price realizations during the quarter (down 7% vs. Q2), broadly tracking the decline in the PLV HCC index (see the chart below). This decline was driven by several factors, including softer customer demand, partly due to a weak restocking season in India, and an influx of Chinese steel exports flooding global markets. Here, I would highlight the dumping of Chinese steel that has led to production cuts by steel producers and reduced the prices they are willing to pay for met coal. During the conference call, HCC explained that these excess Chinese steel exports have impacted its key markets—primarily Asia and Europe—since Chinese steel production relies predominantly on domestic and landlocked Mongolian, rather than seaborne, coal (see the quote below). In response to the low met coal price environment, HCC’s management slightly reduced sales volumes during the quarter (down 18% year-over-year).

The consequences of excess Chinese steel also impact our own markets. This is because Chinese steel production predominantly relies on domestic coals and landlocked Mongolian coals, which typically do not impact the global seaborne met coal balance. Along with stable production from Australia, the U.S.A. and Canada, these factors have created the lowest pricing environment for steelmaking coal since June of 2021.

Nonetheless, I would highlight that, despite met coal prices being at multi-year lows, HCC demonstrated solid profitability/cash flow generation during the quarter, posting $78m in EBITDA (vs. $3.6bn EV). In comparison, HCC’s larger peer, AMR, despite producing more than double HCC’s volumes, generated $49m in EBITDA (vs. $3bn EV). A similar analysis of other comps, METC and ARCH, would also show that HCC’s profitability was superior during the quarter. This underscores HCC’s competitive advantages relative to its US-listed peers, namely 1) lower production costs and 2) a focus on higher-realized-price LV coal.

Looking ahead, HCC’s management reiterated its production volume and cost guidance for 2024. While the company expects met coal prices to “improve slightly” in Q4, management anticipates that “the pricing environment will remain under pressure” due to ongoing weakness in steel markets and delayed infrastructure spending in India. During the conference call, management noted that near-term met coal prices are likely to stay “below the averages we’ve seen in recent years” (see the quote below):

We continue to expect our markets to improve over the next quarter or 2, hopefully above cost curve economics, although we believe pricing may remain below averages we've seen in recent years. Improvements in demand are expected to come mainly from India, and a few select countries. China's recently announced stimulus package and actions are notable, but we're cautious in judging the potential to boost demand in our markets and we'll need time to analyze the total impact.

As another indication that the near-term outlook is not too exciting, AMR’s management suggested that we are unlikely to see significant price increases in the near term (see the quote below):

Like I mentioned, I don't want to stick a specific flag in the ground because we're not in the business of projecting prospects for people. We do have our internal thoughts on it. But we're kind of looking at the world -- looking at 2025 being similar to what we've seen the past couple of quarters, probably leaning more heavily in the current environment. There could be some recency bias there, maybe that's given us a little bit of a more pessimistic view of it. But at this point, that's kind of the best we've got to go on. Don't really see anything in Dan's comments to give us a view of a major move upward going into the beginning of next year. We remain hopeful. And I think once we get past the election next week, maybe some things will start taking shape as far as people positioning, seeing where economic activity starts drumming back up in different areas of the world. But for right now, I think we're pretty comfortable saying that next year is going to -- our view is for planning purposes, it's going to look a little bit like what we're currently seeing.

Despite the cautious near-term outlook, I continue to expect a medium-term recovery in met coal prices, driven by a potential rebound in customer demand. As pointed out by METC’s management, this recovery could be supported by a pickup in Indian demand and China’s stimulus measures, which may boost domestic steel consumption and help absorb some of the excess supply (see the quotes below). I would also point you to World Steel Association’s projections, which forecast “moderate growth” in steel demand over the next two years (see the quote from AMR conference call below).

As India continues to develop incremental blast furnace capacity, demand for coking coal imports is likely to grow substantially. The restocking season in India has been disappointing, likely due to below-trend steel production, along with sufficient current coking coal inventories. However, we're anticipating a pickup in Indian demand and buying next year.

[…]

We are closely monitoring the Chinese steel overcapacity issue in the face of lackluster domestic steel demand. Hopefully, the stimulus measures will increase domestic steel consumption enough to absorb some of the excess supply. In turn, this could lead to less steel exports in 2025. Hopefully, this would generate higher finished steel prices globally and improve profit margins throughout the supply chain.

WSA projects a moderate rebound in steel demand in 2025 and the potential for broad-based moderate growth in 2025 and 2026. Important factors that could fuel such growth were identified as the stabilization of China's real estate sector, monetary policies such as interest rate adjustments to spur economic activity and the trajectory of infrastructure spending in major global economies.

While I do not have strong confidence in these projections, there is another, more fundamental reason why met coal prices are likely to recover going forward. As discussed in my second article on the met coal industry, at current met coal price levels, marginal producers—primarily those based in the U.S. (excluding HCC)—are operating at or close to break-even levels. HCC’s management highlighted this dynamic, stating that “current prices are below the global cost curve.”

Why is this important? Well, historically met coal prices have bottomed at marginal producer cost levels during downcycles before recovering, largely driven by supply exiting the market. I wouldn’t expect this time to be different, as prolonged met coal pricing at current levels could lead to mine closures. Here, I would highlight that AMR has recently begun ramping down one of its newest mines, Checkmate Powellton, and plans to idle it before the end of the year, as the mine is uneconomic at current met coal prices. The key point I am trying make here is that current met coal prices are unlikely to be sustainable for an extended period. And I’m not alone in this view—HCC’s management reiterated a similar perspective during the recent conference call:

At these low prices, we believe that several producers of steelmaking coal have not only experienced significant margin erosion, but may also have experienced realizations below their total cash costs, suggesting that the current pricing environment is not sustainable for extended periods of time.

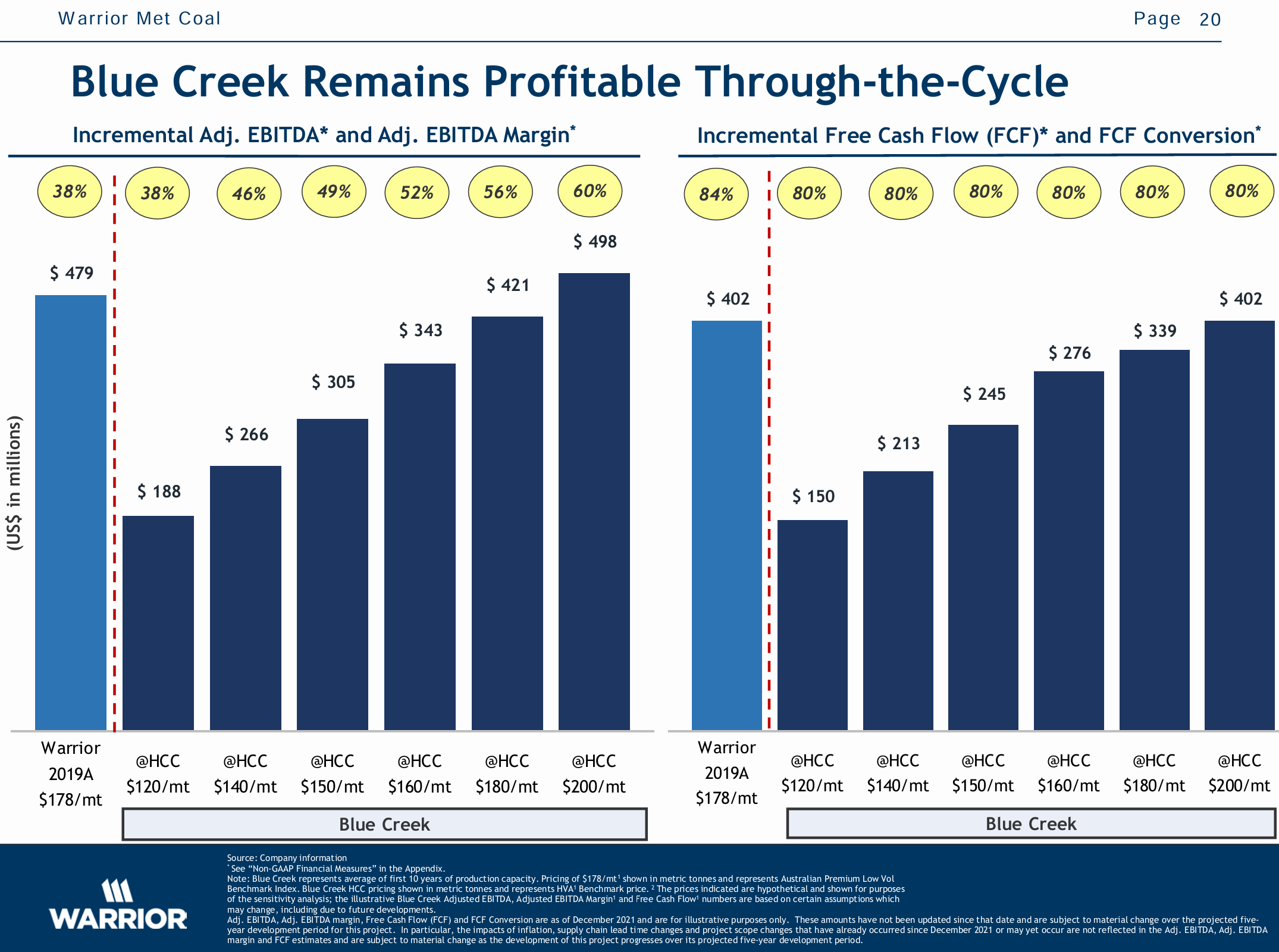

Let’s now turn to a quick update on Blue Creek. By way of background, Blue Creek is HCC’s key growth project—a longwall mine located in the Warrior Basin, Alabama, similar to HCC’s two key operational deposits. Company’s management expects Blue Creek, when fully ramped up in 2026/2027, to rank among the lowest-cost met coal deposits globally, falling below the 10th percentile on the global cost curve. The company has extensively highlighted the asset’s immense cash flow generation potential (see the slide below).

The key update from Q3 earnings is that during the quarter, HCC completed the installation of major components (slope belt, slope car, service cage and raw coal belt) which allowed the company to begin the development of the first longwall panel at Blue Creek. Management reiterated that longwall operations are on track to commence in Q2 2026. Management expects further capital expenditures of c. $90m to $140m related to Blue Creek in Q4, compared to $246m incurred year-to-date.

So, that’s a quick overview of HCC’s earnings. The company, like other met coal producers, operates in a downcycle environment, and I continue to expect met coal prices to return to more normalized levels over the medium term. Even if the downcycle is prolonged (which I consider unlikely), HCC will remain profitable and cash-flow generative, more so than its U.S. peers. What also makes HCC interesting is that the company is developing the large, world-class Blue Creek asset, which will dramatically improve HCC’s cash flow generation due to both incremental production volumes and declining growth capital expenditures.

While HCC’s share price barely budged upon the earnings release, the stock has risen nearly 20% over the past week, partly driven by the election news in the U.S.

To determine whether the setup remains attractive, we need to assess where we stand from a valuation perspective. As shown in the table below, using my previously estimated $235/short ton normalized mid-cycle price, the company is likely to generate c. $400m in normalized EBITDA less maintenance capex, implying a 9x multiple. While this valuation might not seem low, I would note that my assumed price realization relative to the benchmark, 86%, is lower than that seen in recent quarters (e.g., 93% in Q3). Another important point is that my calculation does not include any contribution from Blue Creek. I would again refer to the slide above, which shows that at my estimated mid-cycle met coal price levels, Blue Creek could generate around $320m in free cash flow, lowering the ‘EV/EBITDA-maintenance capex’ multiple to around 5x. So, while HCC is not as cheap as it was when I incorporated the idea to the portfolio, I still believe that HCC’s valuation remains attractive.

With the investment thesis intact and significant further headroom for stock price re-rating, I continue to like the setup and have maintained my position in HCC.

Another great article! Thanks for sharing.

Thanks for your sharing. Would you kindly share more about supporting evidence for the dynamics for 90th percentile marginal cost being the met coal price support ? Much appreciated.