Today, I am back with my research and thoughts on Japanese net-nets. This post marks the third and final part of a three-article series covering cheap, cash-rich companies listed in Japan. Given the recent positive corporate governance reforms in the country, I have decided to add a basket of Japanese net-nets to the Idea Hive portfolio.

In the first article, I detailed the rationale behind investing in Japanese net-nets, followed by a discussion of the stock selection criteria and screening process. To summarize briefly: while the Japanese market has historically offered plenty of net-nets, recent corporate governance reforms make Japanese net-nets particularly compelling now. The reforms are already yielding results, as evidenced by improved board compositions, a surge in activist campaigns, and increasing capital returns in the form of dividends and buybacks to equity holders. Although Japanese equities have partially re-rated since these changes began, many opportunities remain, particularly within the subset of the cheapest companies listed in Japan.

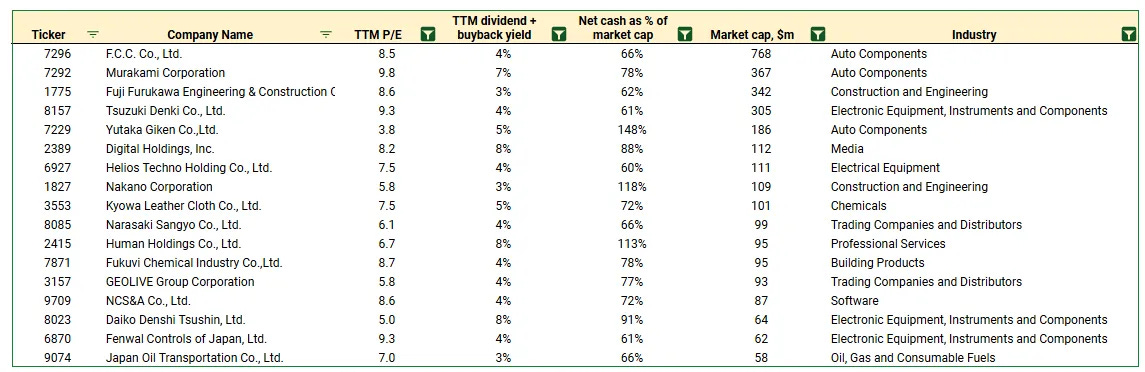

Regarding the selection process, using my screening criteria, I arrived at a list of 17 companies (see the table below).

This naturally leads to the question: “How do we identify which of these net-nets present the most attractive way to play the corporate governance reforms in Japan?” In the second article, I outlined the key criteria for evaluating companies that pass the initial screening round. To summarize briefly, I distilled it down to three key aspects:

A management team with a track record of growing dividends and/or stock buybacks.

A history of consistent growth or a business operating in an industry with secular tailwinds.

A capital-light business model.

To assess how the companies stack up against these criteria, I provided a brief overview of the 17 companies, including a discussion of their businesses, operational performance, and capital allocation.

This brings me to the third and final article, where I will present the Japanese net-nets I’ve decided to incorporate into the Idea Hive portfolio.

Without further ado, here are the four Japanese net-nets I’ve chosen to add to the portfolio:

Murakami Corporation (7292-T)

F.C.C. Co. (7296-T)

Human Holdings Co. (2415-T)

Daiko Denshi Tsushin (8023-T)

Why these companies? Aside from their cheap valuations and large net cash positions, the common theme among these names is the significant improvements in capital allocation seen recently, in the form of increasing dividends and, especially, stock buybacks. While sizable buybacks are not unique to these companies, what sets these four apart is that they have either not pursued repurchases before or have recently ramped up the pace of stock buybacks/dividends significantly. Now, there is a chance that these capital allocation improvements could be one-offs and not indicative of further positive changes. However, I would expect these improvements to be sustainable on average, especially given the growth profiles of these companies.

Below, I provide more detailed overviews of the four companies, covering their businesses, operational performance, capital expenditure profiles, capital allocation, management incentives, and notable risks.

Before diving into these overviews, a few quick notes:

I have allocated equal weight to each position in the basket.

I plan to review the operational performance and latest developments of these companies on a quarterly basis.

Regarding my exit strategy, while I am not setting strict criteria, as a general guideline, I would consider closing the positions (and potentially replacing them with other Japanese net-nets) if valuations exceed 15x forward P/E. I might also consider exiting if there is a significant deterioration in operational performance or capital allocation.

Now, let’s dive in.

Murakami Corporation (7292-T)

Market cap: $383m

Net cash as % of market cap: 83%

P/TBV: 0.6x

Forward P/E: 10.1x

Forward dividend yield: 4%

TTM buyback yield: 2%

Murakami primarily produces automobile components, including rearview, electronic, and concave mirrors. The company holds the largest market share in Japan for automobile rearview mirrors. Murakami also manufactures optical thin-film products (e.g., UV and IR filters) for various end markets. The company operates manufacturing subsidiaries both domestically and internationally, with facilities located in Germany and China. Around 50% of Murakami’s sales are generated in Japan, with the remainder coming from other parts of Asia and North America. A detailed presentation of Murakami’s business is available here.

Murakami has displayed rapid growth in recent years, with a 19% revenue CAGR since FY21 (see the slide below). This growth has been driven by recovering production rates among automobile manufacturers, thanks to the easing of semiconductor shortages that impacted previous years. Management anticipates continued growth, projecting mid-single-digit revenue increases for the current fiscal year. The company operates in a generally secularly growing industry, given increasing regulations mandating the use of advanced driver assistance systems, with minimal risk of disruption from the shift to electric vehicles. So I would expect the growth to continue in the coming years. As for margins, while Murakami’s gross margins have improved from their COVID-era lows, they remain significantly below pre-pandemic levels (15% in FY23 versus c. 19% pre-COVID). This indicates potential for margin improvement in the coming years.

A drawback is that Murakami has historically been a somewhat capital-intensive business. However, the company’s leadership has managed to grow book value per share at an impressive 8% CAGR over the past decade.

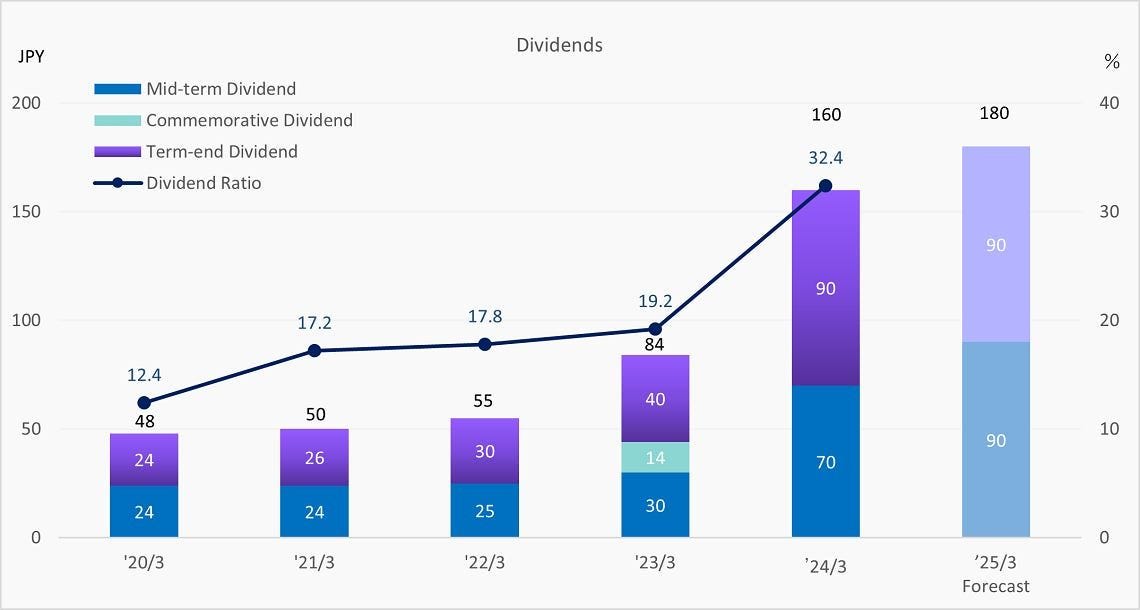

Where Murakami truly stands out is in the significant improvements in shareholder returns seen in recent years. Historically, the company’s dividend payout ratio was relatively low, below 20%. However, this ratio increased substantially to 32% in FY24 (see the chart below). Management plans to pay a slightly higher dividend of ¥180 per share (4% yield) in the current fiscal year. But perhaps even more notable is Murakami’s significant ramp-up in stock buybacks. In FY23, the company repurchased 4% of its current market cap. While Murakami has completed stock repurchases in recent years, this marks a sharp increase from c. 1% of the market cap repurchased in the two preceding fiscal years and even smaller buybacks in earlier periods. This uptick in buybacks suggests improving capital allocation, supported in part by improving operational performance.

An interesting angle is the presence of Dalton Investments, a prominent Japan-focused activist investor, on Murakami’s shareholder register. Dalton, through its Nippon Active Value Fund, holds a 5% stake in the company. Dalton has a track record of successful activist campaigns in Japan, including at Sakai Ovex (where a proposed buyout led to a higher bid from management) and Shinsei Bank (which announced a large stock buyback after activist pressure). So, it’s reasonable to conclude that Murakami’s recent capital allocation improvements have been partially driven by activist pressure. This gives some confidence that the recent capital improvements in Murakami might continue in the coming years.

Murakami’s president and CEO holds a 13% stake in the company (as of March 2024), indicating well-aligned incentives. The CEO, who is a member of Murakami’s founding family, has been in the role since 2008.

F.C.C. Co (7296-T)

Market cap: $987m

Net cash as % of market cap: 50%

P/TBV: 0.8x

Forward P/E: 12.2x

Forward dividend yield: 7%

TTM buyback yield: 1%

F.C.C. (referred to as FCC) is a manufacturer of clutches, primarily for automobiles (55% of revenue) and motorcycles (45%). The company’s customers include well-known car and motorcycle manufacturers, most notably Honda. The vast majority of its revenue comes from overseas markets, with 43% generated in the U.S., followed by 13% in India and 12% in Indonesia. FCC holds a dominant 67% share of India’s motorcycle clutch market. The company operates manufacturing facilities in Japan and internationally, including in the U.S., Mexico, Thailand, India, and Indonesia.

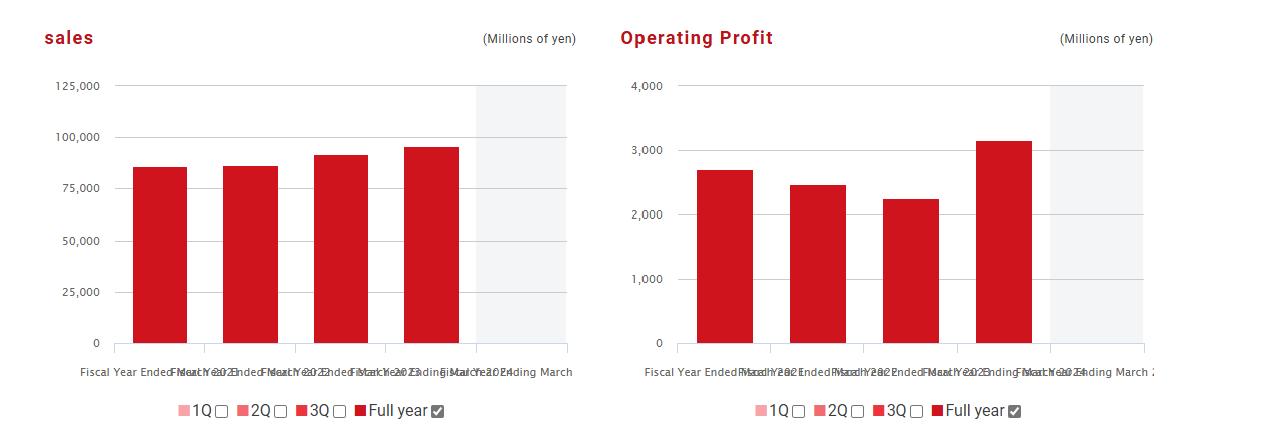

After declining during the COVID period, FCC’s revenue has grown rapidly since 2021, with double-digit growth over the last three fiscal years. This expansion has been driven by strong demand for motorcycle clutches in India and Indonesia, while the automobile business has benefited from rising demand in North America, despite headwinds from the shift to EVs (which do not require clutches).

What might the company’s growth look like going forward? FCC’s automobile clutch business could reasonably be described as secularly declining, given its exposure to the North American market, so significant growth in this segment is unlikely. As for the motorcycle clutch segment, although electric scooter sales have been growing rapidly in emerging markets like India, this growth has slowed over the past year, and the vast majority of newly sold motorcycles still use clutches. FCC’s management expects flat revenue growth in FY25 and FY26, with headwinds in the automobile segment offset by continued strong demand for motorcycle clutches in India and Indonesia. I would note that the company has planned significant growth investments in new product areas, including electric components and power units (see the chart below).

FCC has historically been a somewhat capital-intensive business, although the company’s book value per share has steadily grown in recent years (with the exception of FY20).

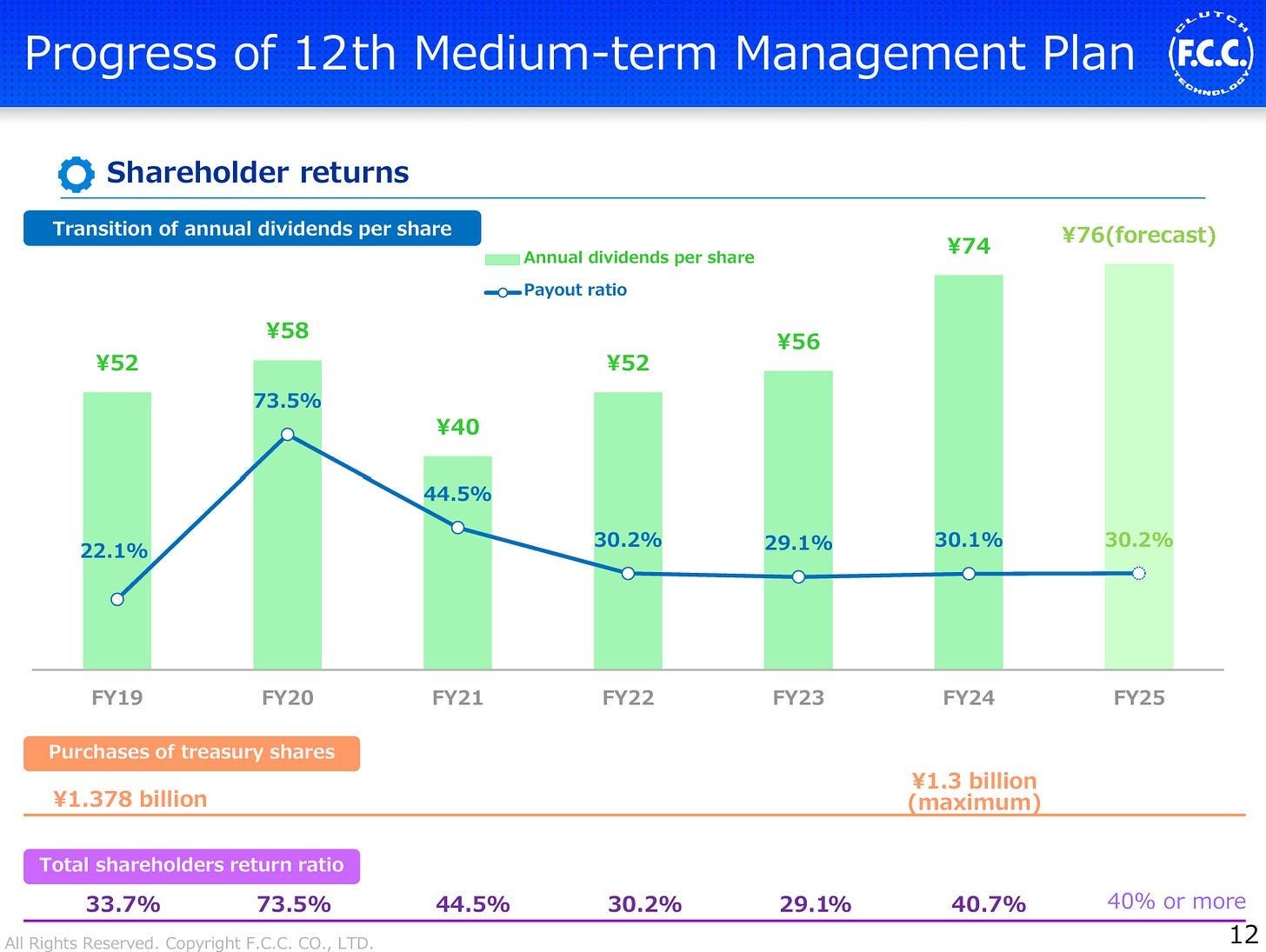

What makes FCC most interesting are the substantial recent improvements in capital allocation. In recent years, FCC has consistently paid out around 30% of its net income as dividends (see the chart below). The dividend is expected to grow significantly in the current fiscal year, to ¥202 per share, or a 7% yield, following a major recent revision to the dividend forecast. In addition to dividend growth, FCC is noteworthy for its decision to initiate stock buybacks in FY24, repurchasing 1% of the current market cap. Given that FCC last completed stock buybacks in FY19, this recent increase in buybacks may signal positive changes in its capital allocation policy. So, while FCC's share price has jumped significantly since the recent FY25 dividend revision, I think that FCC remains attractive given its still significant dividend yield and potential for further improvements in shareholder returns.

None of FCC’s directors holds a stake larger than 1% in the company. FCC’s current CEO has held several executive positions at the company since 2009 before assuming the CEO role in 2020.

Human Holdings Co (2415-T)

Market cap: $95m

Net cash as % of market cap: 126%

P/TBV: 1x

Forward P/E: 6.7x

Forward dividend yield: 5%

TTM buyback yield: 3%

Human Holdings operates in the human resources, education, nursing care, and other sectors in Japan. The company’s key Human Resources segment (c. 60% of revenue) primarily comprises temporary staffing services, mainly for clerical work in construction, manufacturing, and other industries. In the second-largest Education segment (around 30% of revenue), the company provides specialized training and language courses, among other services. While Human Holdings ranks behind larger competitors in the two key segments, it is regarded as a leading player in certain niche markets, such as nail art instructor training and Japanese language teacher training.

Human Holdings nicely fits two of my key selection criteria: a solid growth profile and low business reinvestment needs. The company boasts a strong track record of consistent growth over the past decade, with a 6% revenue CAGR since FY12. This growth has been largely driven by the ongoing trend of increasing demand for recruitment outsourcing in Japan (e.g., see here). Another key trend is the growing demand for foreign labor due to Japan’s shrinking domestic workforce. Given these tailwinds, growth in the HR segment is likely to continue. Company’s management expects revenue growth by FY26 to be largely driven by the expansion of its recently launched DX Solutions business, which provides permanent hiring services for IT engineers. Regarding the Education segment, as highlighted in this research report, domestic demand for reskilling among adults is rising, so I would expect the segment to continue growing as well. Human Holdings’ management expects total revenue growth of 4% in FY24. As for margins, while the company’s gross margins have improved somewhat in the last fiscal year, they remain below pre-COVID levels (25% versus 27-28%), indicating potential for further margin improvement.

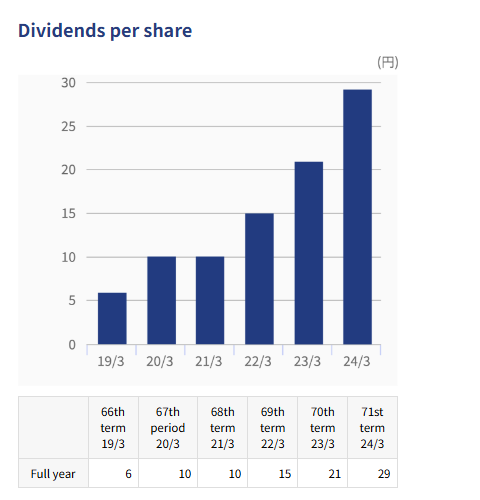

Similar to Murakami and FCC, what makes Human Holdings most attractive is the significant capital allocation improvements. The company’s management recently raised the dividend substantially, increasing it from ¥27-31 per share over the preceding three years to ¥62.5 per share in FY23. Management expects a dividend of ¥64 per share (5% yield) in the current fiscal year. The company has also initiated stock buybacks, repurchasing 3% of the current market cap in FY23. So, it is reasonable to state that there have been significant improvements in capital allocation recently.

A major positive is that the Human Holdings founder family, which includes the company’s current CEO, holds a sizable 24% stake in the company, indicating well-aligned incentives.

Daiko Denshi Tsushin (8023-T)

Market cap: $71m

Net cash as % of market cap: 92%

P/TBV: 1x

Forward P/E: 7.5x

Forward dividend yield: 4%

TTM buyback yield: 2%

Daiko Denshi Tsushin is an IT services provider that operates in two segments: Solutions Services (approximately 75% of revenue) and ICT Devices (25%). The Solutions Services business comprises network infrastructure, software development, and other services. In the ICT Devices segment, the company sells information communications equipment (e.g., from Fujitsu) and provides related services. Daiko Denshi has the largest exposure to two key end markets: the manufacturing and distribution/services industries.

Daiko Denshi is a capital-light business with a solid track record of historical growth, except for a revenue decline following a COVID-induced boost in ICT equipment demand in FY19. Revenue growth in recent years has been driven by growing customer demand for updating corporate IT systems, benefiting Daiko’s key Solutions Services segment. Given the expected growth in IT services outsourcing demand in the coming years (see here), one could reasonably conclude that the industry is secularly growing, and thus Daiko’s growth is likely to continue.

One of my concerns regarding Daiko is the company's significant margin increase in recent years. Daiko’s gross margins have been steadily rising, currently at 26% compared to around 20% pre-pandemic. This improvement seems to be partially driven by 1) the growth of Solutions Services relative to ICT Devices in the revenue mix and 2) an increasing share of services using the company’s own products in the Solutions Services segment. While I am uncertain whether these margins are sustainable, some margin normalization is likely. I would note that management has projected a significant 24% decline in operating income for the current fiscal year (compared to a 6% revenue decline). Nonetheless, considering the company’s inexpensive valuation, even a potential significant decline in gross margins to, say, FY19-FY20 levels of 23%, would still leave the company trading at an undemanding multiple.

Although Daiko Denshi Tsushin’s management has been increasing the dividend in recent years (see the chart below), the dividend payout ratios remain relatively low, below 30%. Nonetheless, what makes Daiko interesting—similarly to the other three companies—from a capital allocation perspective is the significant ramp-up in the pace of stock buybacks over the past couple of years. In FY23, the company repurchased 5% of its current market cap. Coupled with the 3% dividend yield, this brings the total FY23 capital return yield to an impressive 8%.

Daiko’s management holds a minimal ownership stake, with no director or executive holding more than 2% of outstanding shares. The company’s shareholder base includes one of its major suppliers, Fujitsu (14%), and the company’s employee stock ownership association (4%).

Conclusion

This concludes the article series on Japanese net-nets. I believe that the basket of Japanese net-nets provides a compelling opportunity to gain exposure to the expected corporate governance improvements in Japan. While there is no guarantee that all the companies in the basket will pursue significant improvements in capital allocation in the coming years (thus catalyzing share price re-ratings), I would expect the basket as a whole to perform well over the medium term.

Re: Human Holdings Co (2415-T)

I do not understand why company has also sizeable debt (per IBKR), given how much cash does it have ...

Do you have an idea?