Japanese Net-Net Basket: Part 1

The case for investing in Japanese net-nets + an overview of selection criteria and screening

In this post, I am sharing my research and thoughts on Japanese net-nets. This article marks the first part of a multi-part series covering cheap, cash-rich companies listed in Japan.

What sparked my interest in this area are the recent positive corporate governance reforms in Japan. While Japanese equities have generally soared since the reforms were announced, I believe plenty of opportunities remain, particularly within the subsegment of the cheapest companies listed in Japan. To gain exposure to this theme, I have decided to add a basket of five Japanese net-nets to the Idea Hive portfolio.

This article covers the rationale behind investing in Japanese net-nets in more detail, followed by a discussion of the stock selection criteria and screening process. The second part will include a brief overview of companies that fit the selection criteria, while the third article will provide more detailed analysis of the five companies I have added to my portfolio. However, I should note that this structure is not fixed and may change as the series progresses.

Now, let’s dive right in.

Why Japanese Net-Nets?

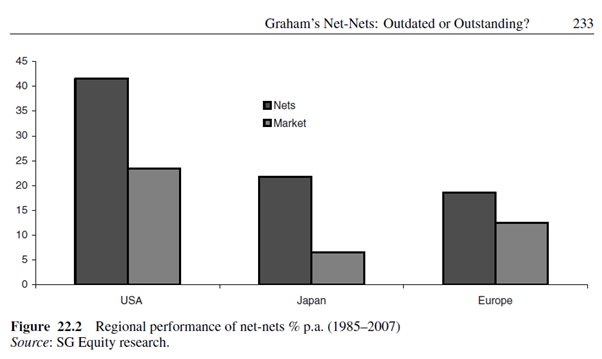

So, what makes net-nets interesting? As a value investor, I have always been fascinated by Benjamin Graham’s net-net strategy due to its strong historical performance. For a quick definition, net-nets are companies trading below their net current asset value (which is equal to current assets minus total liabilities). As shown in the chart below, the net-net strategy outperformed the broader market by a wide margin in major developed markets during 1985–2007. This solid performance extends beyond that period, as the net-net strategy generated 29% annualized returns from 1970 to 1983. While I haven’t come across similar data for more recent periods, given the rapid growth of the US stock market since the Global Financial Crisis, it’s likely that the net-net strategy has slightly underperformed the market. Nonetheless, to illustrate the still-respectable performance of net-nets over the last decade, I could point to the impressive 19% CAGR achieved by this net-net portfolio between 2014 and 2022. So, I think it’s reasonable to state that net-nets generally tend to perform well over longer periods of time.

As for why Japanese net-nets specifically, there are significantly more profitable net-nets in Japan compared to Europe and the U.S. If you run a TIKR screener for companies trading below 0.5x P/TBV (as a very rough proxy for net-nets), you will see over 400 companies in each the U.S. and Japanese markets. However, after filtering out unprofitable companies, the picture changes dramatically, with around 300 companies fitting the criteria in Japan compared to only about 100 in the U.S. While not all of these companies are net-nets, this exercise directionally illustrates that net-nets with profitable operating businesses are much more plentiful in the Japanese stock market compared to the U.S. market (where a significant portion of net-nets are failed, cash-burning biopharmas).

Now, you could correctly point out that this is not a new theme, as the Japanese market has been full of cheap companies for decades. To illustrate this, I would refer you to the chart below, which shows that the Japanese market’s average P/B ratio has been significantly lower than the average P/B of other markets. Another chart below shows that a significant portion of Japanese companies, typically between 30% and 80% (with the exception of 2005–2007), have historically traded below their book values. This compares to only about 3% of S&P 500 companies currently trading below book value.

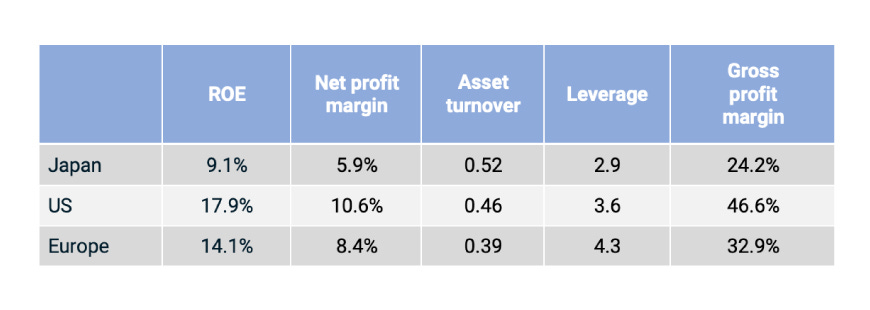

Japanese stocks have generally been cheap for a very good reason: subpar corporate governance, characterized by cash hoarding and the widespread practice of cross-shareholdings in other publicly listed companies, among other aspects. Without going into too much detail, I would note that this subpar corporate governance has been partially driven by the keiretsu structure, whereby a network of interlinked corporations was centered around a major bank. This structure resulted in weak oversight of management, limited shareholder activism, and a prioritization of the group over profitability. The key point here is that subpar corporate governance has led to lower ROEs (see the table with data as of 2024 below), as well as lower dividend payout ratios and a slower pace of stock buybacks.

So, the key question when considering investing in Japanese net-nets is this: can we expect corporate governance in Japanese companies to improve significantly in the coming years?

To answer this question, let me start by saying that, over the last decade, the Japanese government has taken measures to help improve corporate governance in domestic companies. Under Prime Minister Shinzo Abe, Japan introduced the Stewardship Code in 2014 and the Corporate Governance Code in 2015, aimed at promoting “transparency, accountability, and shareholder engagement.” These initiatives have had some positive impact. As discussed in this article, both Japanese company stock performance and profitability saw significant improvement from 2013 through mid-2022.

However, what makes a bet on improving corporate governance in Japan more intriguing are the more recent rounds of corporate governance reforms:

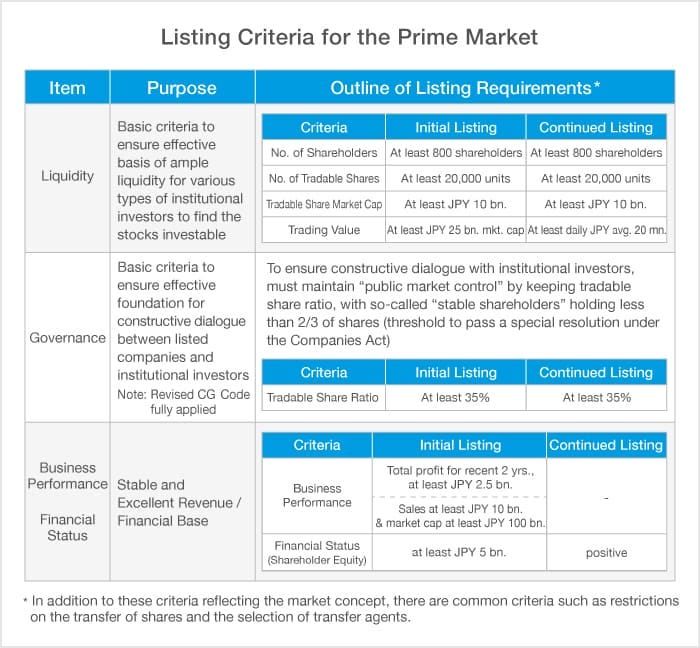

In April 2022, the Tokyo Stock Exchange changed its listing structure, grouping companies into three markets: Prime, Standard, and Growth. As part of the new structure, companies needed to meet certain criteria to qualify for the listings, including liquidity and corporate governance. For example, see below the criteria for obtaining and/or maintaining a listing on the Prime market.

In early 2023, the Tokyo Stock Exchange requested that companies trading on the Prime and Standard markets take “action to implement management that is conscious of cost of capital and stock price.” As part of this request, the TSE stated that companies trading below book value should develop capital improvement plans and subsequently disclose how they intend to make those improvements.

In January 2024, the TSE began publishing a list of companies that have announced the status of their actions related to corporate governance. Concurrently, the Tokyo Stock Exchange also issued a list of underperforming companies that have not complied with the TSE's requests.

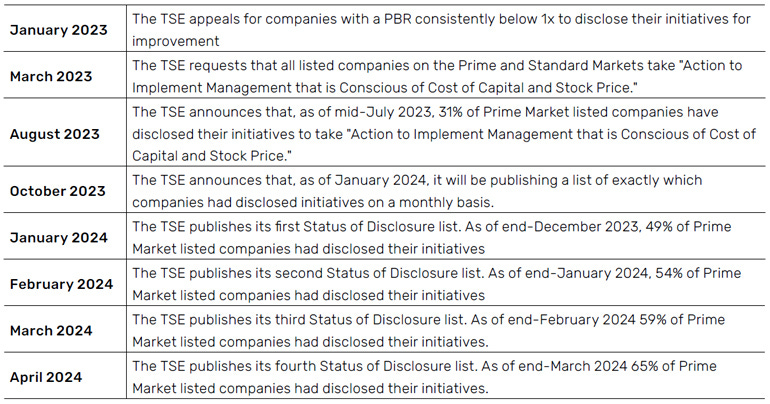

Below is a timeline from Man Group, covering the TSE’s corporate governance-related initiatives since early 2023. The point I am trying to emphasize here is that the TSE appears committed to corporate governance improvement, and this is not simply a ‘box-ticking exercise,’ as also noted by Man Group.

The corporate governance-related initiatives are already bearing fruit. As shown in the chart below, the number of Japanese firms that have disclosed initiatives to improve their corporate governance has steadily grown since mid-2023. According to this Reuters article, as of this month, 79% of companies listed on the Prime market have already disclosed plans to improve corporate governance.

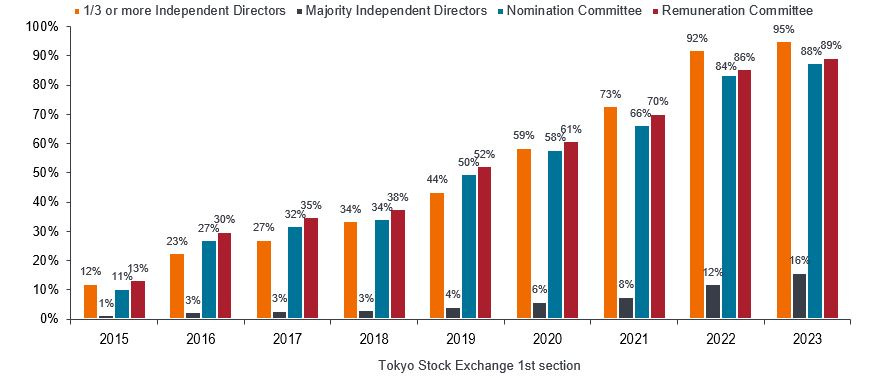

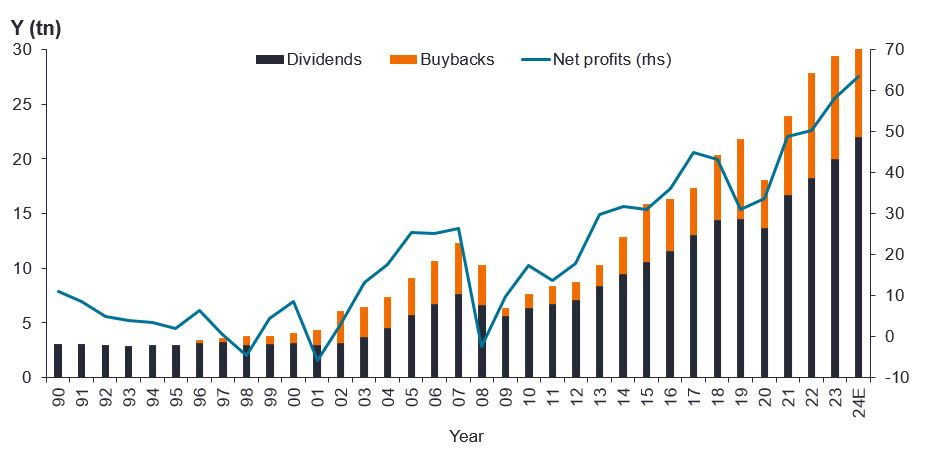

Positive changes are already visible in companies' board compositions. I would point you to the chart below, which shows the increasing number of independent directors on company boards. As another indication of improving corporate governance, see the chart showing that capital returns in the form of buybacks and dividends have exceeded the net profits generated by companies in recent years—something not typically seen over the last decade. This suggests that some companies have been increasingly allocating a portion of their cash piles toward dividends and/or stock buybacks.

Another trend I would point to is that corporate governance-related initiatives have sparked a surge in shareholder activism in Japan. As discussed in this article, the number of activist campaigns in Japan in H1 2024 reached 38, compared to 28 in all of 2023 and similar levels seen in 2021–2022. The number of recent campaigns is also substantially above the average levels seen during 2013–2019 (see the chart from Monash Business School below; note that the figures are for full years).

The impact of these dynamics is, not surprisingly, starting to be reflected in Japanese company valuations. I would like to point you to this data showing that the average P/B multiples for Prime and Standard market-listed companies have increased noticeably in 2023. Meanwhile, the chart below shows that the number of Nikkei companies trading below book value has decreased markedly from 2022 to 2024.

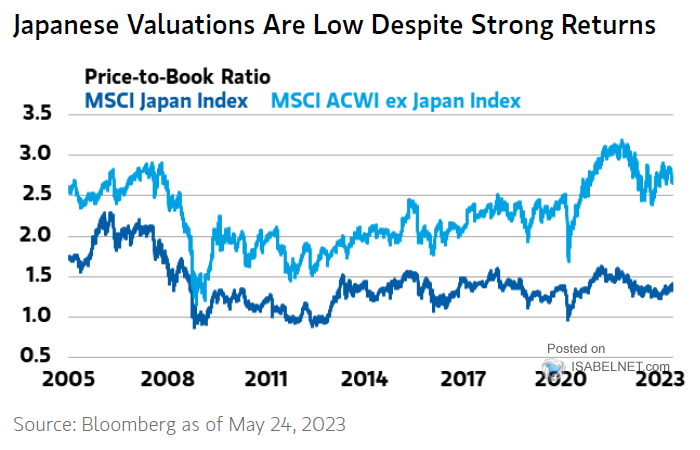

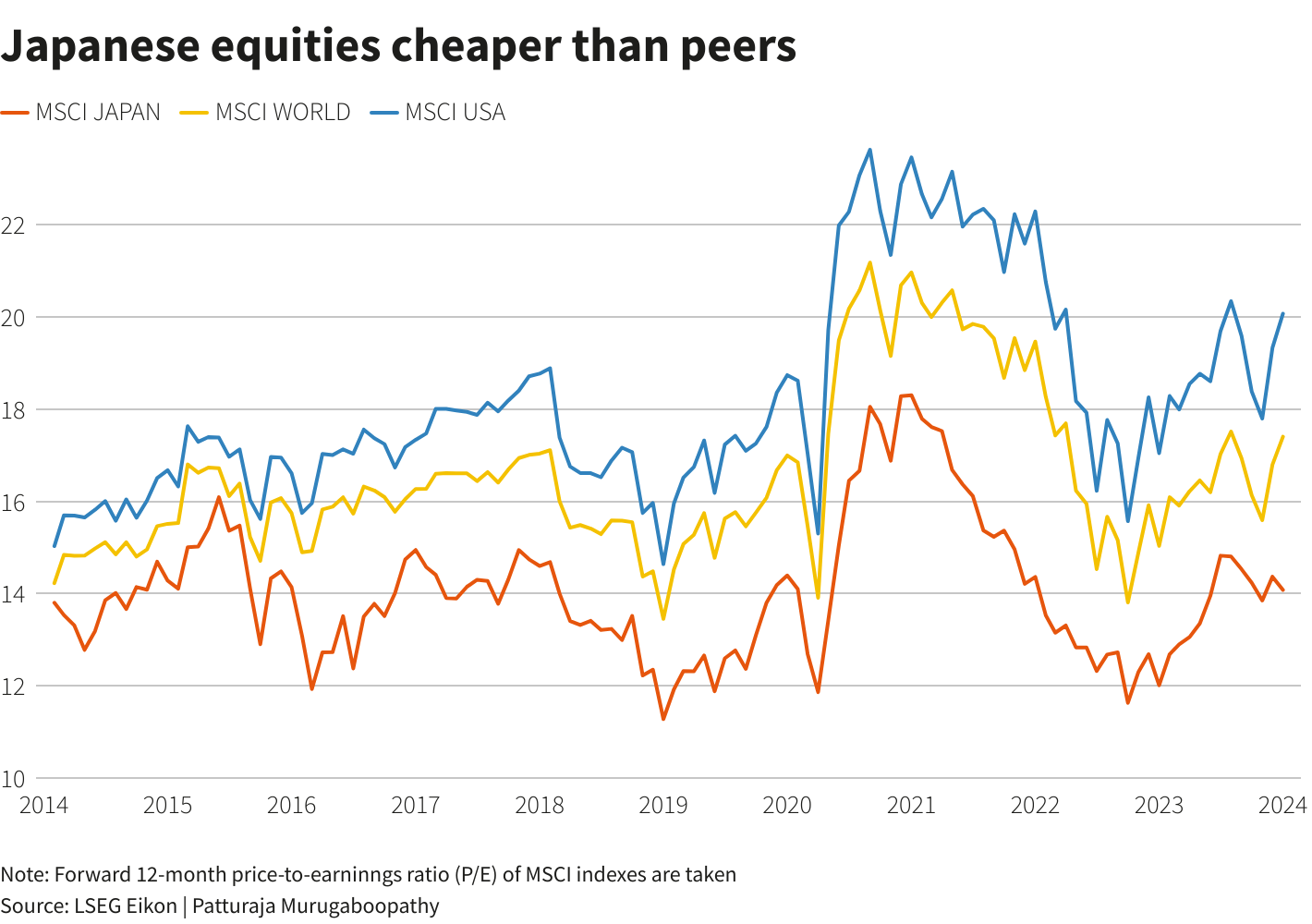

However, I must highlight that, despite some share price re-rating, the Japanese market remains inexpensive. To illustrate this, let me note that: 1) the number of profitable net-nets in Japan is significantly higher than in other developed markets, and 2) Japanese equities continue to significantly lag behind U.S. and global indexes over the last decade (see the chart below). So, it could be argued that the market has generally not fully priced in the potential impact of the corporate governance reforms, suggesting that many attractive investment opportunities in the market remain.

So, that’s the case for investing in Japanese net-nets. I believe that a basket of Japanese net-nets provides an interesting way to bet on continuing improvements in corporate governance in Japan. Given the TSE’s commitment and pressure to enhance corporate governance, I would expect companies to increasingly pursue value-realizing actions, such as divestitures of cross-shareholdings, higher dividend payout ratios, and greater investor communication. While there is no certainty that significant corporate governance improvements will eventually occur on a wider scale, considering the downside protection offered by companies’ large net cash positions, I think the risk/reward is compelling.

Selection Criteria and Screening

So, how do we decide which among the plethora of cheap Japanese companies are worth investing in? Here are the criteria I am using to compile a list of the most attractive basket candidates:

P/NCAV is below 1.2x. While companies trading above 1x P/NCAV are not technically net-nets, I have increased the P/NCAV threshold to 1.2x to arrive at a larger list of companies for further selection.

Cash is over 50% of the market cap. This criterion is used to filter out companies whose current assets consist largely of less liquid working capital assets, including accounts receivable and inventories, rather than cash and short-term investments.

TTM P/E is less than 10x. Given some uncertainty regarding the timeline for when companies might pursue significant value-realizing actions, I am screening for companies that are profitable and cheap based on the performance of their operating businesses.

Combined dividend and stock buyback yield above 3% on a TTM basis. Considering that the average combined dividend and buyback yield on the TSE has recently stood at around 3%, this criterion filters out companies with below-average capital returns to equity holders over the last 12 months.

Market cap is between $40m and $2bn.

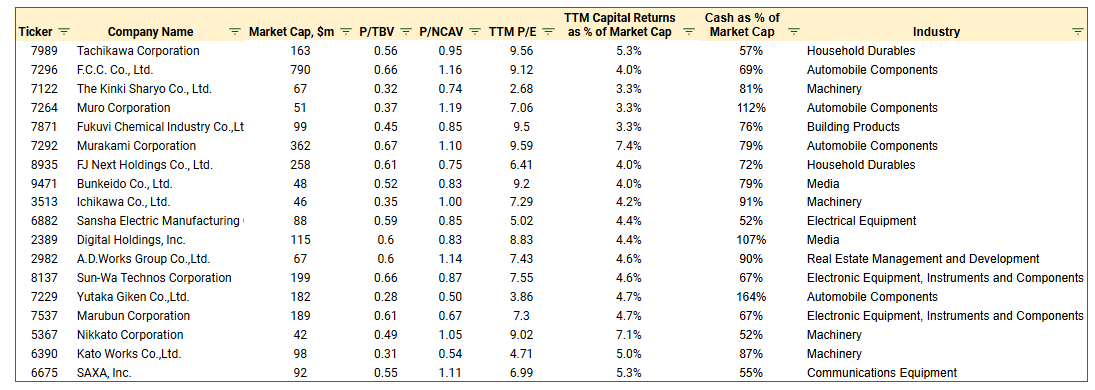

With these criteria, I arrive at a list of 37 companies using TIKR screener.

For the second screening round, I filter out companies with no English filings or an English IR page with financial data. This shrinks the pool to 18 basket candidates (see the table below). These companies fit my screening criteria and will be evaluated qualitatively.

Conclusion

This wraps up the first part of the article series on Japanese net-nets. To quickly summarize, I believe that a basket of Japanese net-nets offers a compelling investment opportunity given the recent corporate governance policy changes in Japan. While there is no certainty that significant capital allocation improvements will occur on average, considering the companies’ cheapness and large net cash positions, I think the risk/reward is compelling.

I intend to return with a brief overview and my thoughts on the 18 basket candidates in the second article, likely in the coming weeks.

Great piece thanks! If it's possible to look at free cash flow as well as profit that might be a helpful addition. I look forward to the next instalment!

Nice. Have owned NCS&A for a year now. Think it is quite well positioned.