In this post, I’m sharing quick updates on two portfolio names (SMLP and PPSI) as I am back from holidays I was on for the last couple of weeks. I intend to publish an article with updates on a couple more portfolio positions (6736-T and ARE-TO) tomorrow.

Summit Midstream Partners (SMLP) — initial post here, last update here

The C-Corp conversion is progressing as expected, as SMLP’s unitholders have recently approved the reorganization during a special meeting. The conversion is anticipated to be completed on August 1.

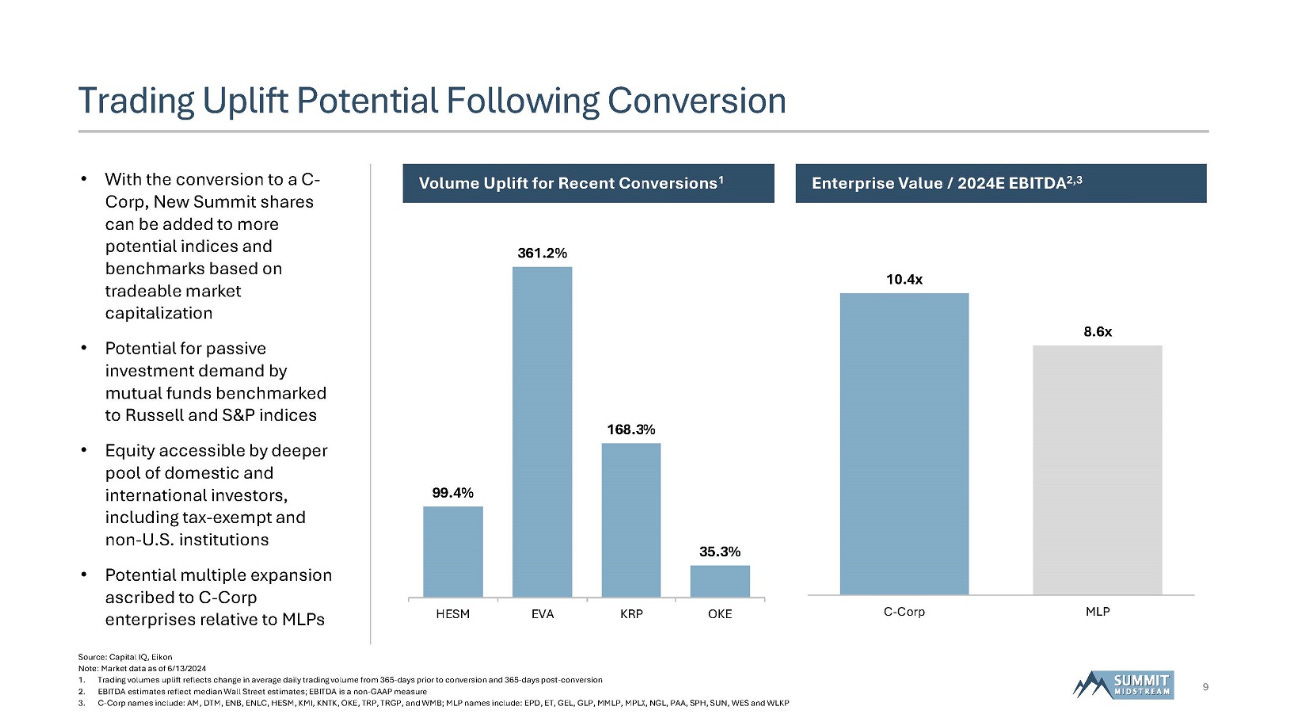

As you might recall from my previous update on SMLP, the conversion, among a number of benefits for the company and its unitholders, will likely lead to increased trading liquidity and potential index inclusion. Both of these would put upward pressure on the stock price (e.g., see the slide from SMLP’s recent investor presentation below).

Despite the looming near-term catalyst, SMLP's share price has barely budged, and the stock remains cheap, trading at only 6.6x 2024E midpoint EBITDA. This compares to 8x+ multiples where the company’s peers are currently trading and where SMLP has recently divested several of its assets. Meanwhile, comparable industry transactions have been completed at 10x+ EBITDA multiples.

I’d expect the reorganization, once completed, to catalyze a stock price re-rating closer to peer multiples. Given SMLP’s significant debt burden, even a relatively minor half-a-turn re-rating on an EV/EBITDA basis would imply a 23% upside from the current stock price levels.

One potential point of pushback here might be the reference to CLMT, another MLP that has recently completed a C-Corp conversion. While CLMT shares jumped on the day the conversion was approved in mid-July, the stock has been annihilated since then, falling by 30% over the last couple of weeks. However, the move can be explained by several factors, including falling renewable diesel industry margins as well as the increased odds of Trump getting elected and potentially revoking the existing subsidies for clean energy. While renewable diesel margins are irrelevant for SMLP, it might be argued that a Trump presidency could in fact be a positive for the company as it could potentially lead to higher O&G exploration and production activity, eventually resulting in a higher number of new well connections for SMLP. So I do not think that CLMT is relevant as a reference point for stock performance after C-Corp conversion. Moreover, as discussed in my deep dive into SMLP, there are a number of precedents (e.g., Hess Midstream C-Corp and large private equity players Blackstone, Apollo, and KKR) suggesting that an upward stock re-rating is likely after the conversion is completed.

Aside from an update on the ongoing C-Corp conversion, over the last couple of weeks, SMLP has made progress on the debt refinancing front, repurchasing the majority of its senior secured notes due 2026 ($785m total outstanding amount as of Mar’24 vs $1044 total debt) by issuing senior secured notes due 2029 ($575m).

With most of the near/medium-term maturing debt refinanced, this puts SMLP one step closer to another potential catalyst, dividend reinstatement. The other hurdles are the achievement of the company’s target leverage ratio (3.5x vs 3.9x as of Mar’24) and the payment of $36m accrued distributions on the preferred stock required to initiate a common unit distribution. Given continuing cash flow generation, I’d expect these to be satisfied/resolved in the coming quarters, paving the way for dividend reinstatement which would help lure in a dividend-focused investor base.

I will be awaiting SMLP’s Q2’24 earnings, likely to be released in early August, for any commentary on the potential dividend reinstatement as well as to refresh the company’s valuation. For now, I continue to think that SMLP presents a compelling setup and have maintained my position.

Pioneer Power Solutions (PPSI) — initial post here, last update here

For a quick recap, PPSI is an electrical power management product manufacturer, which presents a way to bet on the expected EV infrastructure growth. The company is trading at a 14x P/E while displaying 48-51% revenue growth during 2022-2023, with a further 30% guided for 2024. The company’s key products include the mature, cash-generative e-Bloc product line (switchgear systems) and the still unprofitable e-Boost (portable fast-charging units for EVs).

PPSI continues to record significant new contract wins. After announcing several new orders for its e-Boost product line (covered here), earlier this month PPSI announced new e-Bloc purchase orders totaling $7.2m. The orders will be delivered to a variety of clients, including “one of the largest solar power generation developers in the US” ($0.7m), a Southern Californian utility ($3.4m), and “one of the largest distributed generation developers in the US” ($1.9m). The majority of the deliveries are expected in H1’25.

While the company’s management has not provided an updated revenue guidance, the order seems to be pretty sizable. For reference, PPSI generated approximately $30m in revenues from its e-Bloc segment in 2023, while management’s FY24 guidance implies approximately $42m-$44m in e-Bloc revenues. So it seems that the order will provide a significant boost to the company’s topline growth in 2025.

This is clearly a positive development, highlighting that the previously announced contract wins (e.g., $12m in 2021, $9m, and $6m in 2023) were not isolated occurrences and that management’s indications that the product is gaining traction in the market are justified. I think that this further negates my previous thought that e-Bloc might be a rather commoditized product with large competition and is instead at least partially differentiated from competitors’ products.

PPSI's share price has jumped 8% since the announcement, and the company is currently trading at 14x 2024E P/E. While this is admittedly higher than the 12x multiple at which the company was trading at the time of the initial post, I still think that the investment setup is attractive here. Aside from the simple fact that the previous 2024E EPS guidance does not incorporate the recently announced new contract wins, the valuation multiple still does not seem very demanding for a company that is likely to compound its topline at a 30%+ clip in 2024 and potentially in 2025. As a simplistic illustration of the potential upside here, let’s assume the company achieves its 2024E topline guidance and grows a further 20% in 2025, while generating 25% gross margins on the incremental revenues vs 2023 (broadly in line with 2023 total company gross margin levels). Assuming that incremental gross profits fully fall through to the bottom line, this would imply approximately 0.6 in 2025E EPS vs the current stock price of $4.56/share or a 7.6x P/E multiple.

The reason why I think the opportunity exists, and why the market might be less sanguine on the investment setup, is PPSI’s ongoing issues and a lack of clarity related to financial statement reporting. As a quick reminder, back in June the company revealed that it will have to restate its financials from Q1’22 due to revenue and cost recognition errors. The potential impact on the previously reported revenues and costs has not been detailed. So the market might potentially be concerned about the risk of material negative adjustments to PPSI’s recent-year financials. However, while this is admittedly a risk, my understanding is that the restatement will simply redistribute revenues and costs across different periods.

Given the recent positive updates on the operational front and potential substantial upside, I still like the setup and will continue holding PPSI in my portfolio. I will be awaiting any announcements from the company related to the restatement of historical financials as well as FY23 and Q1’24 reports.