Exploring the Quantum Computing Industry

Bubble or investment opportunity?

In this article, I’m excited to share my research and thoughts on the quantum computing industry, as I have been taking a closer look at the sector recently.

I won’t surprise anyone by saying that quantum computing has been one of the hottest sectors in the market recently. With a massive increase in investor interest since November 2024, partially fueled by the unveiling of Google’s quantum computing chip, Willow, in December, the share prices of pure-play quantum computing companies have seen parabolic rises in recent months, with RGTI, IONQ, QBTS, and QUBT up manifold since the beginning of November 2024 (see the chart below).

So, given the already significant investor awareness of the sector and substantial flows into quantum computing stocks, why did I decide to explore the quantum computing space? Well, what sparked my interest were comments from Nvidia’s CEO, Jensen Huang, in January, where he stated that practical quantum computing might be 20 years away. As shown in the chart above, this has led to share price drops in quantum computing companies, with RGTI, IONQ, QBTS and QUBT down by over 30% since the comments. Given the potential of quantum computing to become the next AI, the sell-off has prompted me to explore the industry to see if there are any interesting investment opportunities or if quantum computing is yet another mania, similar to 3D printing, solar, or cannabis stocks.

To quickly outline the structure of this article, I will first provide a basic overview of the science behind quantum computing, followed by a discussion of its importance, potential applications, and key drawbacks. I will then proceed with a brief discussion of the pure-play quantum computing companies, covering their business models and valuations. Before proceeding, I should note that, given the inherent complexity of both the science behind quantum computing and the industry itself, this article is a high-level summary of my research on the subject. For those looking to explore the industry further, while there are a number of solid resources, I would highly recommend reading this industry overview from Martin Shkreli and this analysis article from Stephen Tobin.

With that said, let’s dig in.

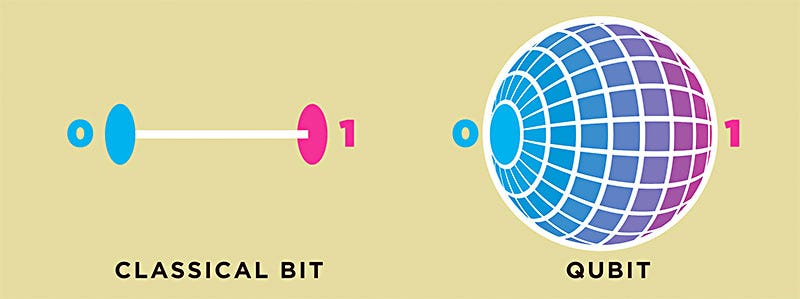

Let’s start with the basic question: What is quantum computing? Well, quantum computing is a type of computing that uses the principles of quantum mechanics to process information in a way that differs from classical computing, which relies on Boolean logic. To explain the difference, let me provide a quick background. While traditional computers store information as binary digits (bits), quantum computers use qubits—the quantum equivalent of bits. The key distinction is that a classical bit can be either 0 or 1, whereas a qubit can exist in a state that is a mixture of 0 and 1 in a certain proportion, a phenomenon known as superposition. One way to think about this is with the example of a sphere. As shown in the chart below, traditional bits represent points on the north and south poles of a sphere. Meanwhile, qubits can exist at any point on the surface of the sphere, representing a superposition of 0 and 1 with certain probabilities. Superposition allows quantum computers to explore many possibilities in parallel: while a classical computer with n bits can perform only n calculations simultaneously, a quantum computer can perform up to 2^n calculations at once.

Another important concept in quantum computing is entanglement. This refers to the phenomenon where two or more qubits become linked in such a way that their states are correlated. When qubits are entangled, measuring the state of one qubit allows you to predict the state of the other, no matter how far apart they are.

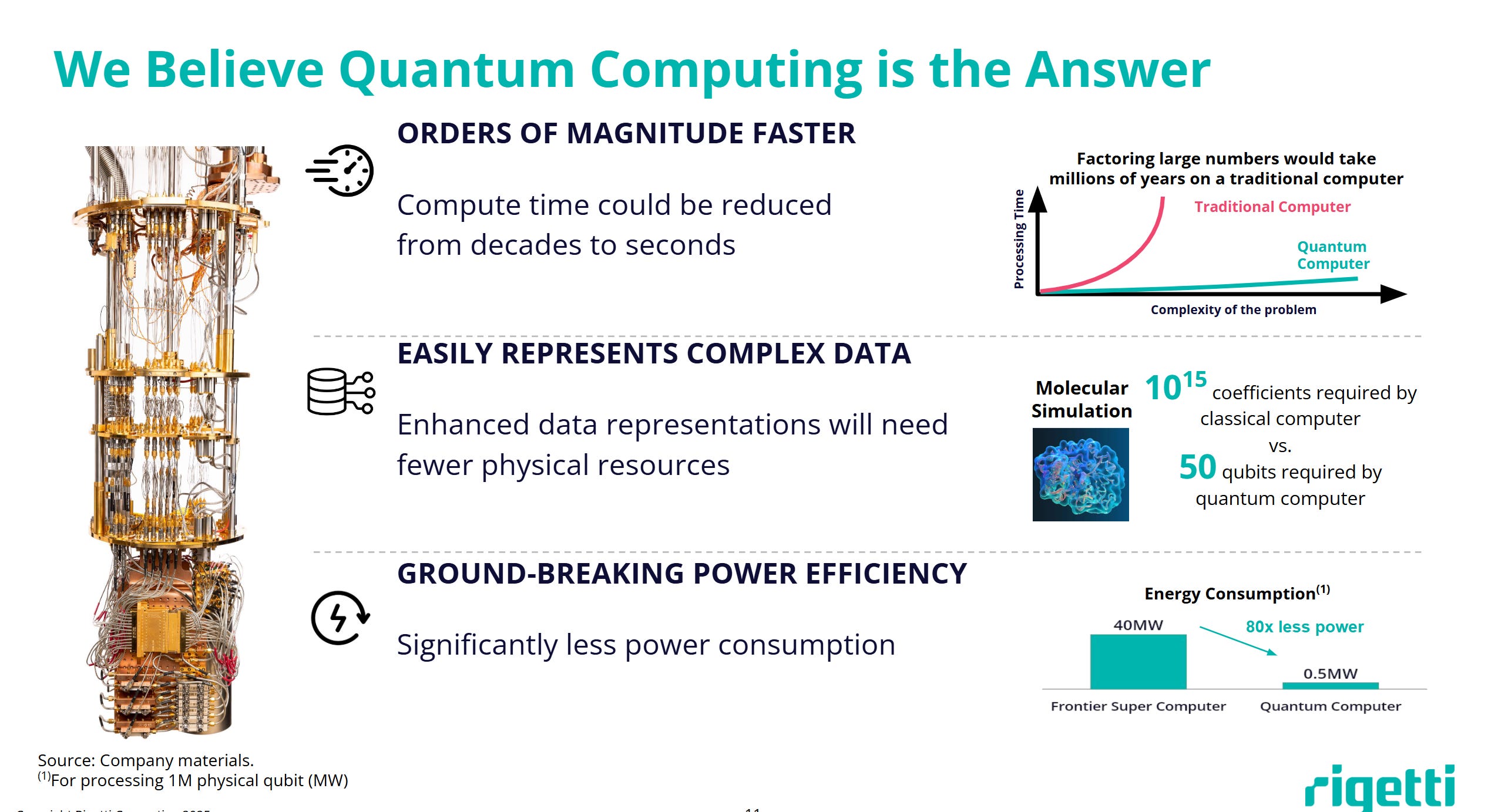

The key takeaway here is that superposition, combined with entanglement, enables quantum computers to boast substantially higher computational power than traditional computers. As illustrated in the slide from RGTI below, quantum computers can drastically reduce compute time compared to traditional computers, all while consuming significantly less power.

Given the superior performance compared to traditional computers, it’s not hard to see why quantum computing is an interesting field. Quantum computing could potentially be applied in a number of areas, including cybersecurity, drug discovery, and supply chain management, among others. There are several areas I would highlight in particular:

One area where quantum computing has the potential to disrupt existing computers is in optimization tasks with a large number of different inputs. Let me use an example from this WSJ article: imagine an airport operator who has to assign planes to specific gates. With just 50 planes and 100 gates, the number of possibilities to assign the planes to gates would amount to 10 to the hundredth power, something no conventional computer could keep track of, unlike a relatively moderate-sized 350-qubit quantum computer.

Another potentially significant application is in drug discovery. As discussed in this article, quantum computers could simulate molecular interactions between drug compounds and biological systems—something that cannot be performed by classical computers due to the exponential scaling of particle interactions. Another area where simulation might be used is in battery chemistry, given that simulating material properties at the atomic level is incredibly compute-intensive for classical machines.

Considering these and other potential applications, the market for quantum computing could be massive. IONQ has highlighted that the market for quantum computing hardware and software providers might reach $170bn by 2040 (see the slide below), while QBTS expects quantum computing’s TAM to range between $450bn and $850bn over the next 15-30 years.

So, that’s the quick bullish case for the quantum computing industry. I think it’s reasonable to state that quantum computing is a promising technology, with a number of potentially revolutionary and disruptive applications. Assuming the market for quantum computing can only partially reach companies' long-term targets, the industry would see massive growth in the coming years and decades.

At this point, a reasonable question you might ask is this: "Given the advantages of quantum computing over traditional computing and the number of potential real-world use cases, why aren’t quantum computers already used on a commercial scale or more widely?"

And this question would be valid: Quantum computing is currently in its infancy and is far from commercial-scale use. To illustrate how early we are in the quantum computing development, I would highlight that the combined qubits of the 10 most powerful quantum computers stand at less than 10,000, with the most powerful computer from IBM boasting 1,121 qubits (see here). I should note that this includes over 7,000 qubits from D-Wave’s quantum annealer, which is not considered a "real" quantum computer, as it can only perform a very specific function—optimization tasks. Nonetheless, even including the 7,000+ qubits and considering that fewer than 200 quantum computers are likely deployed globally, the currently existing qubits are far from sufficient for commercial-scale applications. Here, I would point you to a 2022 study from Microsoft, which suggests that “hundreds of thousands to millions of physical qubits are needed to achieve practical quantum advantage,” with a similar sentiment shared publicly by Jensen Huang.

Several aspects explain why this is the case. As discussed by Martin Shkreli, for a quantum algorithm to display speed/efficiency advantages over traditional algorithms, the quantum computer must have much more than a handful of qubits, considering that current computing technologies are already robust for relatively less demanding tasks. Another aspect here is that the qubits mentioned earlier refer to physical qubits, as opposed to logical qubits, which are created by encoding multiple physical qubits (potentially 1,000 to 1) to detect and fix computational errors. This means that current quantum computers have a significantly lower number of logical qubits. So, I think it’s safe to say that the current quantum computing capacity is far from sufficient for real-world applications.

When can we expect large-scale, commercial quantum computing to be reached? Commentary from tech industry players suggests that this may be multiple years or even decades away. Aside from the comments from Nvidia’s CEO, both Bill Gates and Meta’s Mark Zuckerberg have expressed a similar sentiment, with Zuckerberg stating that quantum computing is “still quite a ways off from being a truly practical paradigm.” While Google is more optimistic, it does not expect to see its quantum systems reach full, commercial scale until the end of the decade. Here, I would note that, given its involvement in quantum computer development, Google clearly has a stake in this race and might be incentivized to put forward optimistic targets. In any case, I think it’s safe to conclude that real-world applications are still far off, and we are unlikely to see large-scale, commercial applications until at least 2030.

Why are some of the most prominent people in the industry so conservative regarding the timeline for commercial-scale use of quantum computers? To explain this, I will briefly revisit the technology behind quantum computing. The key issue is that qubits are extremely sensitive to the environment—any slight disturbance, such as temperature changes or electromagnetic fields, can cause qubits to lose their quantum state, leading to computation failure. So, it’s crucial to isolate the system from any outside factors to ensure qubits remain stable long enough to perform calculations while also allowing information to flow in and out of the system. The most popular way quantum computers achieve this is through the use of superconductors, i.e., materials that allow the flow of electrons with zero resistance and thus maintain qubit stability. The problem, however, is that superconductors require temperatures near absolute zero. This necessitates specialized refrigeration systems, rare gas isotopes (helium-3 and helium-4), and significant power consumption. Given this, coupled with the fact that quantum computers require precious metals (e.g., gold), it is not surprising that quantum computers are highly expensive. As highlighted in this article, a single qubit might cost around $10k. Another approach to quantum computing, the trapped-ion approach, does not require cooling since ions are held at room temperature. However, this method still requires specialized and expensive equipment, including low-pressure vacuums and lasers. As an indication of how costly this approach is, I would highlight that the price of IONQ’s trapped-ion quantum computers has been estimated to range between $5m and $10m.

Aside from the high cost of building and running quantum computers, I would note that quantum computers require entirely new software and algorithms compared to those run on classical computers. While several algorithms for quantum computing have already been created, including Shor’s (for factoring) and Grover’s (for search), many real-world problems (e.g., in the fields of optimization and drug discovery) do not yet have efficient quantum algorithms.

So, between the high cost of building and running quantum computers, along with the need for new software and algorithms, it’s not hard to see why quantum computing is still in its infancy and has yet to take off.

At this point, I have established that while quantum computing is a potentially promising technology, it’s still in its early stages with respect to wide-scale commercial use. Nonetheless, the key question from an investment perspective is what the market has already priced in. After all, even if the technology is in the very early stages, if we are not paying much for the growth optionality, a bet on quantum computing companies might be sensible.

This brings me to a discussion of quantum computing companies. I would divide public companies operating in the quantum computing industry into several categories:

Pure-play quantum computing companies: RGTI, IONQ, QBTS, and QUBT.

Large, much more diversified quantum computing players: IBM, Alphabet, Microsoft, Amazon, etc.

Quantum computing component/material suppliers. This includes semiconductor manufacturers (e.g., Intel), cryogenics companies (e.g., Linde), and photonics companies (e.g., Hamamatsu Photonics).

The companies in the second and third buckets are large and highly diversified, with quantum computing representing only an insignificant portion of their businesses currently, meaning that they are not ideal for playing the quantum computing industry. As for the industry ETF, Defiance Quantum ETF, pure-play quantum computing companies represent only a tiny fraction of its net assets. For these reasons, I will focus on the first bucket: pure-play quantum computing companies. Below are brief overviews of the four companies.

Rigetti Computing (RGTI). RGTI produces quantum computers, including the quantum processors that power the computers, which are manufactured in the company’s wafer fabrication facility. Similar to IBM and Google, RGTI uses the superconducting approach to quantum computing. The company has deployed 17 of its quantum computing systems so far. Its product lineup includes the latest quantum computing system, the 84-qubit Ankaa-3. The company generates the majority of its revenue from technology development contracts with government agencies and research institutions, including an IDIQ contract with the US Air Force Research Lab announced in September 2023. RGTI’s revenue has been in the range of $12m to $13m over the last two fiscal years. While revenues are expected to remain minimal for the next 3 to 5 years, over the long term, management expects sales to increase as the QPUs are commercialized. Aside from QPU sales, management expects the company to generate recurring revenue from providing cloud-based access to quantum computing for customers. From a liquidity perspective, RGTI boasted a net cash position of $80m as of September 2023, compared to c. $17m in recent-quarter operating losses.

IONQ (IONQ). IONQ produces/sells quantum computers built using trapped-ion technology and provides access to quantum computing for customers via the cloud. The company has so far sold 10 quantum computing systems. IONQ’s latest generation product, Forte, boasts 35 qubits. Revenues have grown significantly, from $11m in 2022 to $22m in 2023, and $37m on a TTM basis, driven largely by several government contracts, including from the US Air Force Research Contract ($55m announced in September 2023, $21m in January 2025) and the Applied Research Laboratory for Intelligence and Security ($6m in August 2024). The company boasted a net cash position of $366m compared to a $53m loss from operations reported in Q3 2024.

D-Wave Quantum (QBTS). D-Wave Quantum produces a special type of quantum computer, a quantum annealer. Unlike the computers produced by RGTI and IONQ, the annealers are focused specifically on solving large optimization problems. QBTS’s product lineup includes Advantage 2, the most powerful quantum computer with over 7k qubits. QBTS has been the first pure-play quantum computing company to commercialize its offerings, generating revenues from commercial customers, largely by providing access to quantum computing via the cloud. In February, QBTS announced the sale of its first quantum computer. The company’s revenues have ranged from $6m to $8m during 2021–2023. Pro-forma for the recent $150m equity raise, QBTS has a net cash position of $178m as of December 2024, compared to c. $20m in recent quarterly operating losses.

Quantum Computing (QUBT). Unlike the three other pure-play QC companies, I think it’s fair to describe QUBT as a shady company or even an outright fraud. This is a minimal/no-revenue company that has undergone multiple pivots, including from a beverage distributor to a quantum software business to a quantum computing hardware company. Most recently, in 2023, amid the Nvidia/semiconductor chip mania, QUBT declared plans to establish a quantum photonic chip foundry. For more background on the company, I highly recommend reading two short reports published by Iceberg Research (here and here) detailing the company’s shady history, including the non-existent foundry and faking revenues via contracts with undisclosed third parties.

So, do these companies present attractive investments at the current stock price levels? Considering QUBT’s minimal revenues/history, it’s reasonable to immediately exclude the stock as a potential investment. As for the remaining companies, it’s clear that the market is pricing in substantial growth in the coming years, with all three stocks trading at egregious 100x+ 2025E revenue multiples. Despite the significant potential growth runway for each company, I believe these valuations are too generous. Let me illustrate this point by evaluating the companies’ revenues going forward:

IONQ’s management expects sales to “approach” $1bn in revenues by 2030, implying a roughly 8x EV/revenue multiple. Assuming the company reaches this $1bn target by 2030, this would suggest a 73% CAGR from 2023 through 2030.

While QBTS’s management has not provided a medium-term revenue target, they have stated that the TAM for combinatorial optimization problems (best suited for quantum annealers produced by the company) attributable to hardware, software, and service providers might reach $100m-$250m in 3-5 years. Optimistically assuming QBTS could capture 50% of this market, this would imply a roughly 10x EV/revenue multiple.

As for RGTI, the company’s management has estimated that the annual revenue for quantum computing providers might stand at $1bn-$2bn by 2030. If RGTI can capture 20% of the total industry revenues (which might be optimistic given significant competition in the superconducting quantum computing sub-sector), this would imply that the company is currently trading at a 10x EV/2030 revenue multiple.

Now, I must note that the companies’ revenue/TAM targets are imprecise, and it’s certainly possible that the companies might either exceed or fall well short of them. Given that the industry is in its infancy, it’s hard to determine how the competitive environment will play out. One key question here is which quantum computing approach (superconducting, trapped ion, etc.) will establish itself as the widespread market standard and become dominant or if different approaches will capture certain niches of the market. The recent breakthrough of molecular qubits (see here) highlights how nascent the field is and how rapidly it is evolving, making it hard to conclude which approach will come out on top. Another question is my lack of understanding of companies’ competitive advantages vs competitors within the same approaches, such as RGTI vs IBM, Google, and other superconducting approach-focused competitors. The point I am trying to get at here is that it is highly uncertain what portions of the market the pure-play quantum computing players will eventually be able to capture.

Having said that, I think it’s reasonable to conclude that pure-play quantum computing companies are generously valued by the market, with significant growth already priced in. And I think management teams seem to agree that these companies might be valued at excessively high levels currently. For one, during a recent interview, RGTI’s CEO noted the hype surrounding quantum computing stocks, implying that market expectations might be excessive (see the quote below). As another indication that the companies might be overvalued, I would point to the recent equity raises performed by several companies below or in line with the current stock price levels. This includes QBTS ($150m worth of stock sold at $6.1/share in January) and RGTI ($100m worth of stock sold at $2/share in November).

Particularly because of the hype that is going on in the quantum computing space and some erroneous statements are being made, including by people in the industry, we have to tamp down some expectations.

[…]

So I have to tell them [investors] that it's still not the time to talk about sales and sales growth because we are still very much in the technology development mode. We have to get the technology perfected before we can start seeing real material difference in sales.

So, I would be very hard-pressed to describe the sector as undervalued or fairly valued currently, as the optimistic outlook is already incorporated into the stock valuations. With limited margin of safety, I am staying on the sidelines from the long perspective. Given the arguments outlined above, might these stocks be decent short candidates? While that might well be the case, considering that these are small-cap stocks operating in a hyped-up sector with already high short interest, I think it’s too risky to play the sector from a short perspective.

This caps off my dive into the quantum computing industry. To quickly summarize, quantum computing has a number of potentially interesting applications and thus large potential. Nonetheless, the technology is currently in its infancy and is unlikely to reach commercial-stage likely until 2030. With pure-play QC companies currently trading at egregious valuations, for now, I am inclined to stay on the sidelines but will be following developments in the sector.

There is an old saying in the investment world that everyone seems to forget: "An innovative company is not necessarily a good investment." Time will tell.

IBM is a real company with a long track record. Watson solved Jeopardy and Healthcare. At a PE in the mid 20s it is similar to GOOG and cheaper than these expensive lottery tickets. My AI summary actually suggest they don't suck at quantum. But then again they don't need to have clients yet. https://chatgpt.com/share/67b7e5e1-c224-800e-b0ff-240f810783fd