A Deeper Dive Into AMPY

Research and thoughts on valuation, potential catalysts and management

Amplify Energy (AMPY) — initial post here

In this post, I’m sharing my research and thoughts on Amplify Energy (AMPY) as I have been recently taking a deeper look into this portfolio name.

To recap the investment thesis briefly, AMPY is an oil and gas producer that presents an attractive way to invest in the energy space. The company is currently trading at c. 5x EBITDA and 10x FCF. These are undemanding multiples for an O&G company with low-decline and long-reserve-life assets, which have consistently generated cash flow in recent years. The company is also trading c. 50% below the estimated value of its proven developed reserves. Besides the cheapness based on current production/proven reserves, AMPY’s cash generation might be on the cusp of inflection given the recent development of its key world-class oilfield asset, Beta. New well drilling at Beta, if successful, could create incremental value multiples above the current share price.

There are several key questions that I think are crucial in determining the attractiveness of AMPY as an investment opportunity:

How cheap is the company compared to its peers? While AMPY seems inexpensive on EV/EBITDA, P/FCF, and ‘EV/PD PV-10’ multiples, it is important to consider the company’s valuation in the context of the broader O&G space.

How does the underlying value get realized? The key to answering this question is to explore the potential catalysts, primarily Beta’s development as well as potential segment divestitures and/or a company sale.

Can investors rely on management to realize the underlying value? Assessing management’s track record of steering the company/allocating capital and incentives is important to determine the likelihood of the expected catalysts materializing.

I will explore these questions in turn.

TL/DR: I continue to think that AMPY presents an attractive investment opportunity, especially after yesterday’s sell-off without any announcements from the company. While the company does not seem cheap in the context of the broader industry, what I think separates AMPY is the number and significance of potential catalysts, most notably the Beta development. While there are admittedly spots on management’s track record, the company has generally demonstrated solid capital allocation and has handled the recent year headwinds decently.

Now, let’s dig in.

Valuation

As a quick background before diving into valuation, below are the company’s key assets. AMPY boasts c. 13 years of reserve-to-production life and an estimated 6% proven developed resource decline rate over the next ten years. Oil represents approximately 43% of total production.

Without going into a detailed overview of each asset, I think that the chart below displaying historical production volumes nicely illustrates that these are generally stable and low-decline assets. One asset that might jump out when looking at the chart is Beta, as its production dropped sharply in 2022. This is explained by the oil spill that occurred back in late 2021, leading to a halt in production. However, Beta has since returned to production, and volumes in recent quarters have already exceeded pre-spill levels.

With that brief backdrop, let’s turn to relative valuation. At the current prices, AMPY is trading at 4.6x TTM EBITDA, 9.8x TTM FCF, and 0.52x ‘EV/PD PV-10’.

How does this compare to publicly-listed peers? Well, I will note upfront that relative valuations based on peer multiples are not straightforward given that AMPY is a mash-up of a number of geographically dispersed assets. Having said that, on an ‘EV/PD PV-10’ basis AMPY is trading slightly above similar-sized comps BRY and REI but at a significant discount to larger peers CRGY and VTLE (see the table below). I think that this valuation is roughly fair:

Given similar reserve life but lower annual PDP reserve decline rate and leverage compared to BRY and REI, I think that AMPY deserves a small valuation premium over these two comps.

As for CRGY and VTLE, while AMPY boasts a higher reserve life, lower PDP decline rate, and a similar oil/natural gas/NGL production mix, comps’ much larger size and focus on the Permian Basin (where AMPY does not operate) suggest that they might be reasonably valued at higher multiples.

On an EV/EBITDA and P/FCF basis, meanwhile, AMPY is currently trading above its comps trading at 2.9x-3.6x EBITDA and 3.4x-8.3x FCF multiples (see the table below). This valuation might partially reflect the fact that AMPY’s TTM operational performance does not include full contribution from Beta (which went back online in mid-2023). Nonetheless, even on a forward basis AMPY trades at still relatively high 3.8x EBITDA and 8.1 FCF. While the comps do not provide 2024E EBITDA/FCF guidance, I think it is reasonable to conclude that AMPY is currently valued quite heftily by the market on these multiples relative to peers.

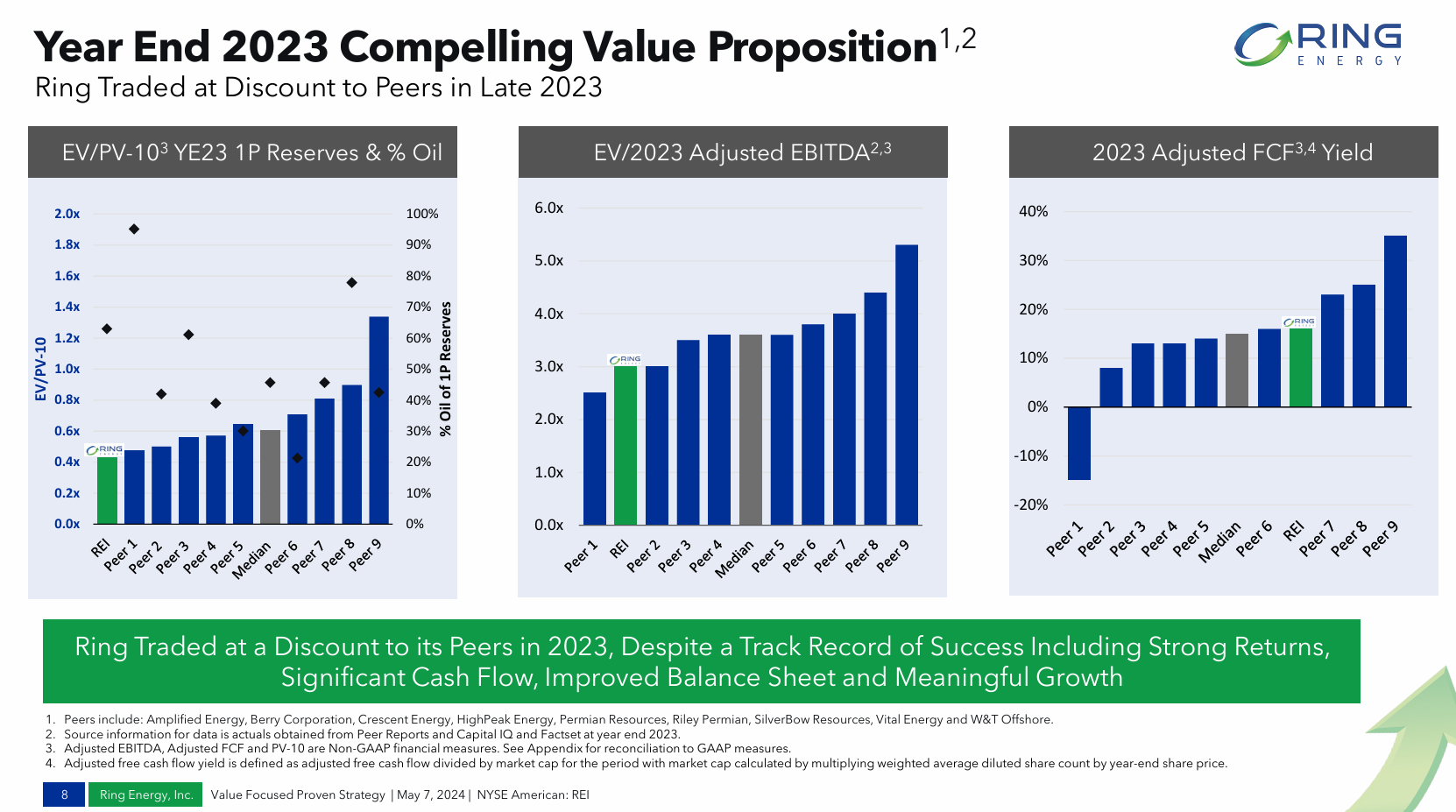

A nice illustration of valuations across the industry is the May 2024 investor presentation published by REI, displaying peer valuation multiples (see the slide below). The presentation is admittedly a bit dated and uses 2023 financial metrics; however, it directionally illustrates the point that AMPY is currently trading close to the higher end of peer EV/EBITDA and P/FCF valuation ranges and close to median on an ‘EV/’PD PV-10’ basis.

Source: Ring Energy Investor Presentation, May 2024.

As for the recent industry transactions involving AMPY’s publicly-listed comps, there are several recent reference points:

In May, SBOW (operates assets primarily in the Eagle Ford Shale in Texas) announced that it is getting acquired by peer CRGY at 3.3x TTM and 2.6x 2024E EBITDA and 7.6x TTM FCF. On an ‘EV/PD PV-10’ basis, the transaction has valued the target at a 0.8x multiple.

In June, DEC announced an acquisition of natural gas assets in Eastern Texas for $100 million or 3.8x estimated forward EBITDA. The transaction valued the assets at their PD PV-20 valuation (0.65x PD PV-10).

Just last week, VTLE, in tandem with NOG, announced an acquisition of Point Energy Partners’ assets in the Delaware Basin. The transaction valued the assets at 2.4x forward EBITDA.

These datapoints confirm that AMPY is not cheap on a relative basis and might in fact be seen as valued on the expensive side among its peers.

Catalysts

Now, you might be thinking: "Why invest in AMPY as a way to play the O&G space if the company is not cheap compared to its peers/there are plenty of other companies trading at even lower multiples?"

Well, one key aspect that I think separates AMPY is the number and significance of potential catalysts that could unlock the underlying value, most notably the Beta development program, which might lead to significantly improved cash flow generation in a couple of years. Besides the Beta development, other potential catalysts include potential segment divestitures and/or the sale of the company.

Let's go through these potential catalysts one by one.

Starting with Beta. You might recall from my initial post that the Beta development comprises two projects: 1) facility upgrades and 2) new well drilling.

The facility upgrades include ongoing electrification and emission reduction projects at Beta's facilities since 2023. Two of the three phases of the upgrades have been completed, with the final stage expected to be completed in H2’24. The capital expenditures related to the project stood at $10m in 2023, with a further $15m expected to be invested in 2024. Cost savings are estimated at $6m-$8m in 2024, which is significant considering that AMPY generated $29m in TTM FCF.

While the facility upgrades are likely to incrementally boost AMPY’s FCF generation, probably a much more significant part of Beta’s development from a cash generation perspective might be the new well drilling program initiated this year. AMPY expects to drill 4 new wells in 2024 (for a total capex of $20m-$24m), with the option of further drilling if the program proves successful. The new well drilling at Beta is particularly interesting due to the impressive estimated unit economics, with IRRs expected to be "in excess of 100%" (see the quote from the Mar’24 conference call below). Production per well is expected to reach 350 bpd in the first year, followed by 205 bpd in the second year.

At Beta, following an in-depth technical review of the undeveloped potential in the field, we're pursuing a full well development program in 2024, with the first well having been spud earlier this week. At current prices, the development program is forecast to generate attractive IRRs in excess of 100% and payback periods of less than 1 year.

It is not hard to gauge the size of the opportunity. Assuming the company achieves $20m in first-year revenues from four well drilling (lower end of management’s guidance) and $12m in the second year (proportional to the first-year production based on the guided volumes), the two-year incremental FCF would stand at $8m-$12m. With the company potentially expanding its drilling to 12 wells per year (maximum capacity allowed by the current infrastructure), we might be potentially looking at $100m+ in incremental annual FCF several years down the road. Applying any conservative multiple to this FCF would likely imply a multi-bagger upside from the current stock price levels. This is obviously speculative/uncertain at this point since the new wells are yet to be drilled and produce first oil, but what I am suggesting here is that AMPY’s current valuation seems to assign minimal value to the optionality of Beta’s development proving successful.

Now, one of the key questions here is, "Will Beta’s new well drilling be successful?"

While I am by no means an expert in the field, the odds of a successful drilling outcome might be solid. One positive is that the company has previously highlighted that it has already completed drilling in the Beta field as recently as 2015, with IRRs exceeding 200% (see this presentation from 2019, p. 18). Moreover, during the latest earnings release, AMPY’s management stated that it is “encouraged by the data in the drilling logs, which supports the hydrocarbon potential of the target formation” (see also the quote from the most recent conference call below). Given that the presence of oil has been confirmed and that the infrastructure is in place, it appears the only risks here are potentially higher than expected capital expenditures and/or delays rather the drilling failing to produce any oil.

In conjunction with the cost savings being realized by the large facility project at Beta, we also anticipate substantial production growth as a result of our 2024 development program. The company spud the A45 well from the Ellen platform in March and successfully reached the objective formation. Amplify's formation logs reinforce the company's views that the target interval has a high oil saturation and is expected to deliver excellent results.

Moving on to another potential catalyst, the potential divestitures of AMPY’s assets. Back in Nov’23, the company launched a sale process for the Bairoil asset (located in Wyoming). During the latest conference call, management stated that the monetization is expected to be completed “over the summer,” with an update “potentially in advance of the next [earnings] call” (see the quote below).

So that process will take place basically -- we're kind of wrapping up kind of -- or middle of, towards the end of [ data run ] to this point, bids will be due towards the end of May. There's traditionally a first round, second round, and then you'll negotiate a PSA. And obviously, we've got the added complication of the fact that we're doing kind of a dual process with a monetization structure as well. So we anticipate this will happen over the summer and potentially in advance of the next call. And so we'll obviously update the market at the appropriate time. But that is coming soon.

While it is not clear if the asset sale will materialize, potential monetization would likely result in significant net proceeds. Assuming Bairoil is valued at 50% of its PD PV-10 value (in line with where AMPY is valued on an ‘EV/PD PV-10’ basis) would imply $76m in potential transaction proceeds. This would allow AMPY to pay down the majority of its debt ($112m net debt as of Mar’24) and/or pay out a large special dividend/buyback shares, something management kind of hinted at as potential options during the latest conference call (see the quote below).

With respect to the strategic initiatives highlighted on our previous calls, the Bairoil marketing process is progressing as expected. As a reminder, we are exploring complete divestiture of the asset as well as considering alternative financing structures with the goal of maximizing shareholder value. A successful Bairoil monetization will accelerate our ability to reduce debt outstanding and to evaluate return of capital options.

The sale of other assets is also a possibility, including the company’s 8% interest in the Eagle Ford asset located in Texas. Worth highlighting that the recent merger between SBOW and CRGY combined both companies' assets located primarily in the Eagle Ford Basin. During the merger conference call, the companies highlighted (see the quote below) that they have completed a number of acquisitions in the basin over the recent years and see plenty of opportunities for further consolidation in the basin. So I would not be surprised to see either party or another industry player scoop up the Eagle Ford asset/AMPY’s interest.

The combined business has executed 12 Eagle Ford acquisitions over the last 3 years, totaling more than $4 billion of total transaction value. Pro forma for this transaction, Crescent will be the second largest operator in the basin alongside ConocoPhillips and EOG. Nevertheless, the Eagle Ford remains one of the most fragmented basins in the Lower 48 with substantial opportunity for further growth.

And so the Eagle Ford is a great basin. It's the second most productive basin onshore in the U.S. It's the least consolidated. So huge opportunity there. And we hope to be able to find more things to do. But I think the great thing is we've got lots of great stuff to do if we do nothing. And when we do something, we feel really strongly about value creation around it.

After potentially successful Beta drilling and Bairoil/other asset divestitures, the end game might revolve around the potential sale of the company. In its current form, AMPY is a mash-up of geographically dispersed assets and is simply too tiny to benefit from the economies of scale (leading to higher G&A per barrel of production) that larger comps do. For reference, AMPY’s G&A expenses stood at $10m in Q1’24, which is significant compared to the company’s FCF ($29m on a TTM basis) and market cap ($285m). While at the moment the potential sale angle is purely speculative, given the potential synergies for the acquirer, coupled with industry consolidation trends (see here and here), I’d expect AMPY to garner significant interest were it to launch a sale process.

Management’s Track Record

Let’s now turn to what I consider an equally important part of the investment thesis: management’s track record of shareholder value creation, capital allocation, and incentives. I think this aspect is important for several reasons, including to gain conviction in management’s estimates for Beta’s new well drilling and have confidence in capital allocation going forward (e.g., if/when an asset divestiture is completed).

As a quick background, AMPY was formed after a merger of equals between Amplify Energy and Midstates Petroleum Company completed back in 2019. AMPY’s current CEO and chairman have both held executive/director roles with the AMPY’s predecessor company since 2017. So while there have been changes to the management team/board of directors over recent years (e.g., the current CEO was previously the CFO during 2018-2021 before assuming the CEO role), it seems reasonable to attribute company’s recent-year actions to the current management team.

I will start with the negatives, as there are admittedly several spots on management’s track record:

Management has run several divestiture/monetization processes that failed to result in any transactions. The most notable example is the company’s stake in Eagle Ford, for which the company launched a divestiture process back in 2017, but it failed to result in an asset sale. The company eventually pursued a new development program with the asset during 2018-2019. Subsequently, in 2022, AMPY again announced that it was marketing its stake in the asset, but no transaction was ultimately announced.

The company has a history of failed drilling results. Back in 2017, AMPY initiated new well drilling at its East Texas asset. However, after drilling several new wells during 2017-2018, the company eventually suspended the drilling program due to results that were “below [company’s] expectations.” AMPY spent c. $50m on capex during 2017 for East Texas new well drilling.

These aspects might point to several potential risks, including 1) management not being able to sell Bairoil assets despite the ongoing sale process and 2) failure in Beta’s new well drilling program.

However, there are some counterarguments that address these points. The Eagle Ford divestiture process announced in 2022 was likely intended to receive cash to pay down debt to satisfy the credit agreement. However, with a rise in natural gas and oil prices and subsequent borrowing base redetermination, the company no longer needed to sell the asset which explains why the divestiture was eventually called off. Another aspect here is that AMPY has historically disposed of several of its assets, including South Texas properties (for c. $18m) and Anadarko Basin assets ($54m), both sold in 2018. This shows that management has been willing and able to dispose of multiple separate assets.

As for the East Texas failed drilling program, while it is clearly a negative on management’s track record, I do not think that this failure is indicative of potentially unfavorable results in the ongoing Beta new well drilling program. The key aspects here are that Beta is a separate asset located in a completely different formation and the fact that the presence of oil in Beta has already been confirmed.

Moving on to the positive aspects, what gives some confidence in the management team is the company’s solid capital allocation displayed over recent years. Prior to Covid and the subsequent Beta oil spill, the company had been focused on G&A expense reduction and used free cash flow/divestiture proceeds to deleverage the company. As an illustration of these, G&A expenses decreased from $29m in 2017 to $24m in 2018 while net debt has been reduced from $371m as of Nov’17 to $274m as of Feb’20. See the quote from the Mar’19 conference call below:

There are several key examples of our accomplishments this year aligned with our strategy. We reduced G&A to align our overhead with our forward strategy with 2 workforce reductions: one in January of 2018 and the other in January of this year. All in, we have cut our G&A approximately in half since late 2017. We rationalized our portfolio with the sale of our Anadarko Basin producing properties in early 2018, with net proceeds of approximately $54 million.

In the meantime, the company had been paying out substantial capital returns, including a large tender (for c. 12% of outstanding shares) completed in 2018 as well as substantial dividends ($16m paid out in 2019) and stock buybacks ($26m worth of stock bought back in 2019). Management’s focus on capital returns is nicely illustrated by this quote from the company in 2021:

We were a return of capital story… before it was in vogue with everybody back in 2018 and 2019.

The situation changed with the subsequent headwinds of Covid (leading to a decline in oil and natural gas prices) and, later, the Beta oil spill (negatively impacting production volumes) These factors forced the company to cut capital returns, with no dividends and minimal buybacks completed since 2019. However, the company has since then focused on deleveraging, driven partially by the receipt of $95m Beta oil spill-related insurance proceeds and Beta returning to production in 2023. Company’s net debt has been reduced from $274m as of Feb’20 to $112m as of Mar’24. Given these points, coupled with the fact that the company has not completed any acquisitions over recent years (aside from the merger in equals announced in 2019), it could be argued that AMPY handled the recent-year headwinds decently.

So it seems that the risk of value-destructive actions, such as expensive M&A, is low, and generated cash and/or any divestiture proceeds are more likely to be used towards continuing debt reduction and potential capital returns.

Would management be willing to sell the company? Well, communication with management by a number of investors (e.g., Chris DeMuth Jr., see here) indicates that management understands the rationale behind selling the company and might eventually be willing to launch a sale process. Having said that, leadership has admittedly tiny ownership, with c. 1% stake in the company, and is compensated generously, with the CEO pocketing $2.4m in 2023 total compensation. Change-of-control payouts are also relatively insignificant (e.g., $4.6m for the CEO), suggesting that management is not incentivized to initiate a company sale process. So I would not count on the company sale as the likely catalyst here and would consider it speculative at this point.

Conclusion

While AMPY is not cheap among its peers, what makes the investment opportunity attractive is the number and significance of potential catalysts, most notably the Beta development. There are several questions/spots on AMPY management’s track record, but the company has generally demonstrated solid capital allocation and has handled the recent-year headwinds pretty well. I continue to think that AMPY presents an attractive investment opportunity and have maintained my position. I will be waiting for Q2’24 results (to be released in on August 7) for updates on the Bairoil divestiture process, Beta’s development, and to refresh the valuation.

This a tired idea