Portfolio Idea Playing Out

Latest thoughts on MGPI following a thesis-confirming update.

MGP Ingredients (MGPI) — initial post here, last update here

In this post, I am sharing my quick thoughts on one of my portfolio positions, a short in MGP Ingredients (MGPI), following the recent important Q3’24 update from the company. I believe the update is highly positive for the short thesis and clearly indicates that the idea is starting to play out as expected.

To briefly recap the investment thesis for those unfamiliar, MGPI is primarily a wholesale provider of American whiskey barrels. MGPI offers an interesting way to play the expected downturn in the whiskey industry. Increasing demand for whiskey over the last decade, further amplified by a Covid-induced boost, has driven American whiskey supply to unprecedented levels. However, the industry now appears to be coming off a historic supercycle, as indicated by declining American whiskey prices reported by industry players. The expected industry downturn is likely to lead to a significant decline in the price of wholesale American whiskey barrels, MGPI’s key profit driver.

Yesterday, MGPI reported preliminary Q3 2024 results and provided updated FY 2024 guidance. In the third quarter, MGPI saw significant operational performance deterioration across the board, driven by softer-than-expected trends in company’s alcohol categories and elevated whiskey inventories across the industry.

Here are some of the key operational performance metrics for Q3:

The company expects Q3 2024 sales to decline by 14%, a significant deterioration compared to the 7% growth and flat topline seen in Q2 and Q1, respectively.

Revenues in the key Distilling Solutions segment are expected to decline by 36%, compared to 9% and 2% growth in the last two quarters.

Sales in the remaining Branded Spirit and Ingredient Solutions segments are also anticipated to decline in the quarter, by 6% and 18%, respectively.

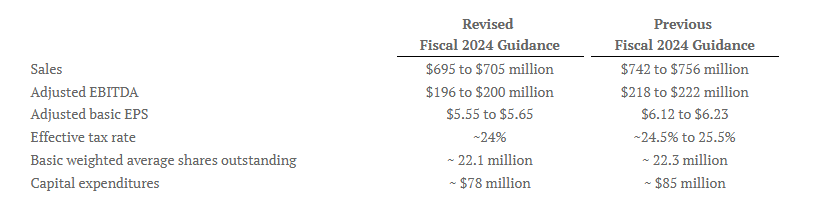

As for the FY 2024 guidance, the company revised its previous outlook downward, with revenues and EBITDA expected to decrease by 7% and 10%, respectively, at the mid-point (see below).

The most interesting aspect was that MGPI’s CEO, for the first time, explicitly highlighted the negative impact of “elevated industry-wide whiskey inventories” on operational performance, while also stating that “these industry headwinds” are likely to “persist at least through the rest of the year”—see the quote below:

We are disappointed with our third quarter results and fourth quarter outlook. Soft alcohol spirits category trends and elevated industry-wide whiskey inventories are putting greater than expected pressure on our brown goods business with a larger impact on our smaller, craft customer base. We expect these industry headwinds to persist at least through the rest of the year and will share details about our 2025 outlook with our fourth quarter 2024 earnings release.”

The Q3 results and revised full-year outlook confirm my earlier contention that the stable or improving operational performance seen in recent quarters—including rapid growth in brown goods volumes in Q2—might have been sustained by previously signed customer contracts at more favorable terms than those signed currently. With the legacy contracts now seemingly rolling off, I would expect the company’s performance to continue deteriorating. The fact that management pre-announced Q3 results—something MGPI has not done in recent years—further confirms that the company is aware of the looming decline in operational performance and that it might continue to worsen.

Another aspect of the press release worth noting is the weak sales growth of just 1% in Q3 for the premium-plus category of the Branded Spirits segment. I have previously highlighted the increasing trend of premiumization (whereby demand for higher-quality, longer-aged bottles rises at the expense of cheaper, less-aged whiskey) as one of the key risks to the investment thesis. Given the significantly slower growth in the premium-plus portfolio compared to 29% in Q2 and 12% in Q1, this suggests the trend might be weakening and thus might negatively impact the performance of the Branded Spirits segment going forward.

So, to sum up, MGPI’s recent announcement confirms that the inflection in the American whiskey industry is finally being reflected in the company’s operational performance. And I would expect MGPI’s performance to continue deteriorating in the coming quarters.

MGPI’s stock was down 20% in after-hours trading. Despite the stock price decline, I believe that the remaining downside is still significant as MGPI is currently trading at multiples above its replacement cost. A potential re-rating from the current EV of $1.5bn to the tangible book value of $0.3bn—still above where MGPI traded before the industry upcycle—would imply a potential downside of 80%+.

I will be waiting for the full Q3 2024 results and the conference call, scheduled for October 31, for more details from management on operational performance and outlook. For now, with the investment thesis intact and large remaining potential downside, I continue to view MGPI as an attractive short opportunity and have maintained my position.

Congrats on a great pick!