New Portfolio Name — ENAV.MI

Undervalued regulated monopoly on the cusp of cash flow generation inflection

In this newsletter, I share summaries of attractive investment ideas sourced from the Value Investors Club and incorporated into my personal portfolio. These summaries will be complemented by regular updates on key developments impacting investment theses. My aim with Idea Hive is to document my portfolio management process while enabling readers to quickly grasp and follow attractive investment opportunities.

Today, I am back with a new portfolio idea: ENAV (ENAV.MI). ENAV was written up on VIC in February. You can find the full write-up here.

Just a quick note before diving into the idea: I am planning to share the last starting portfolio position in the coming days. While I will continue to occasionally add new ideas to the Idea Hive portfolio after that, you can expect the blog to be more focused on updates and additional research on the existing portfolio names.

Now, onto the investment idea.

ENAV (ENAV.MI)

Elevator Pitch: Undervalued high-quality regulated monopoly on the cusp of cash flow generation inflection.

Current Price: €3.93

Target Price: €5.21+

ENAV is a €2.2bn market cap company that operates a perpetual concession to provide air traffic control services in Italy. The company generates fees whenever an airplane flies over Italian airspace and/or takes off or lands at an Italian airport.

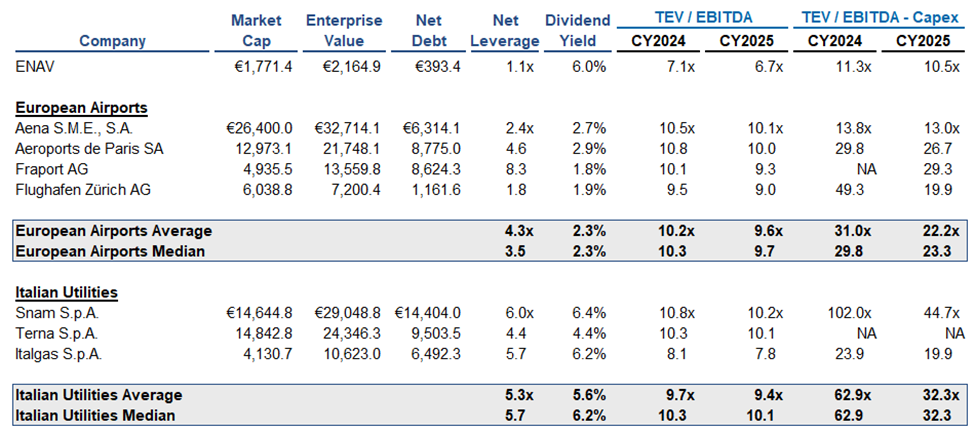

At the current share price, ENAV is trading at c. 7x 2024 EBITDA, adjusted for the cash owed to the company by airlines due to declines in traffic since COVID-19. This is an undemanding valuation for a high-quality business—a regulated monopoly that generates contractual cash flows and boasts 25%+ EBITDA margins. The current valuation is also substantially below the c. 10x average multiple at which other European airport concession operators and Italian utility companies trade.

The crux of the investment thesis, and the reason for the opportunity, is that ENAV’s convoluted accounting has obscured the true economics of the business, with a mismatch between the company’s cash flows and IFRS earnings. The company’s cash flow generation has lagged IFRS earnings in recent years due to lower than expected traffic because of COVID-19 and higher than expected inflation. However, the key aspect here is that ENAV is contractually set to be reimbursed for these impacts via higher rates in the coming years, which is expected to drive a material improvement in cash flow generation.

Let’s unpack this in a bit more detail.

ENAV receives fees from the regulator Eurocontrol after the regulator collects them from airlines on behalf of ENAV. The rates that airlines have to pay to Eurocontrol (and, in turn, ENAV) are reset every five years, based largely on inflation and traffic forecasts. Importantly, there are traffic and inflation risk-sharing mechanisms whereby any significant divergences from traffic and inflation forecasts are largely/fully reimbursed by airlines. See excerpts from the VIC write-up below:

Any traffic divergence vs. the forecast above or below 2% is absorbed 100% by ENAV. The next 8% up or down is absorbed 70% by the airlines and 30% by ENAV. Anything below or above 10% is fully reimbursed either by the airlines or ENAV (if traffic exceeds 10% of forecast). Stated another way, ENAV’s service units are guaranteed not to exceed or 4.4% greater than forecasted or, in a downside case, decline more than 4.4%.

[…]

To the extent inflation is above expectations, ENAV is compensated by airlines via the same balance mechanism as the traffic risk sharing. There is ~€5mm of inflation balance created for every 100bps that actual inflation exceeds what was projected at the beginning of the regulatory period. In addition, this inflation balance stacks / carries over each year throughout the regulatory period (i.e., €35mm of inflation balance created in ’22 is carried over to ’23 and an additional €19mm of inflation balance created in ’23 is added on top so the total inflation balance for ’23 is €54mm).

Over the last four years, ENAV’s cash generation has been negatively impacted by 1) lower than expected traffic due to COVID-19 in 2020-2021 and 2) higher than expected inflation during 2022-2023. These factors have not had a massive impact on ENAV’s reported EBITDA (see table below) as the company recognizes income from the traffic risk-sharing mechanism in the year of the shortfall. However, the company’s cash flow generation plummeted, with FCF declining from €187m-€249m during 2018-2019 to negative €217m-€225m in 2020-2021. ENAV’s FCF has since then partially recovered, with €139m-€167m displayed in 2022-2023, but still remains significantly below pre-COVID levels.

However, given the existing risk-sharing mechanisms, the company now seems to be spring-loaded for a cash flow generation inflection in the coming years:

Due to the traffic risk-sharing mechanism, ENAV has recorded significant COVID-related balance accruals (see table above). As of Q4’23, the company is entitled to €585m in non-taxable COVID-related accruals, with €510m expected to be paid over the next five years. This translates to €140m of annual incremental cash flow through 2027, compared to 2020-2022 levered free cash flow of €72m-€160m (excluding balance sheet accruals).

As for the higher than expected inflation, ENAV is expected to receive an additional €35m in 2024 and €58m in 2025 due to the existing inflation escalators.

Combined, these are expected to drive ENAV’s normalized 2025 EBITDA and FCF to €295m and €287m, respectively.

With these estimates, ENAV is currently trading at c. 6x normalized 2025E EBITDA/FCF. ENAV has historically traded at an average 8.8x EV/NTM EBITDA multiple prior to Covid. The current valuation is also substantially below Italian utilities and European airport concession operators trading at c. 8-10x 2025E EBITDA and 22-32x 2025E EBITDA-Capex multiples (see table below). Applying a more reasonable 9x 2025E EBITDA multiple would imply a share price target of €5.21/share or a 33% upside.