MGPI Research Notes

Insights on the industry, valuation and key risks

Today, I am sharing my additional thoughts and research on MGP Ingredients (MGPI), an idea added to the Idea Hive portfolio in mid-May.

For those unfamiliar with the investment thesis, MGP Ingredients is a spirit distiller that offers an interesting way to bet on the decline in American whiskey prices. Increasing demand for whiskey over the last decade, combined with a further Covid-induced demand boost, has driven American whiskey supply to unprecedented levels. However, it seems that the industry has recently been coming off a historic supercycle, as indicated by declining American whiskey prices. There seems to be plenty of room for a downward share price re-rating given that MGPI currently trades at multiples above the replacement cost. You can find my initial post here.

This post will focus on the following aspects of the investment thesis, complementing the initial pitch:

A quick overview of MGPI’s business segments.

A deeper look at the Covid-induced boost for the American whiskey industry, including a glance at media/industry reports, MGPI’s management commentary, as well as MGPI performance pre-/post-Covid.

A look at MGPI’s valuation relative to peers.

A discussion of the key risks to the investment thesis, including secularly growing demand for American whiskey and premiumization trends.

TL/DR: Several aspects confirm that the American whiskey industry benefited from a Covid-induced demand boost and is now on the cusp of a negative inflection. With the investment thesis intact, I continue to like this setup and have maintained my position.

Let’s dig in.

Quick Business Overview

MGPI is a producer of premium distilled spirits, branded spirits, and food ingredient solutions. While the company has historically been primarily a third-party supplier of premium food-grade alcohols to American whiskey manufacturers, it has expanded into the higher-margin branded whiskey subsegment with several acquisitions completed in recent years. The company currently operates three segments:

Distilling Solutions (54% of revenues). This segment processes corn and other grains into food-grade alcohol (primarily bourbon, rye, and other whiskeys) and distillery co-products that are subsequently sold to manufacturers of branded spirits. Sales to customers are made both on the spot market and on a contract basis. Aside from food-grade alcohol, the company also provides barreling, warehousing, and blending services.

Branded Spirits (30%). This segment comprises MGPI’s portfolio of primarily American whiskey brands produced in the company’s distilleries and bottling facilities and subsequently sold to distributors. The brands range across a wide spectrum of price categories (ultra-premium, super-premium, premium, mid, and value). MGPI entered the branded spirits business with the large acquisitions of Luxco (Apr’21) and Penelope Bourbon (Jun’23).

Ingredient Solutions (16%). MGPI supplies primarily specialty wheat starches and proteins. These products are sold primarily to food processors and distributors.

Industry Overview

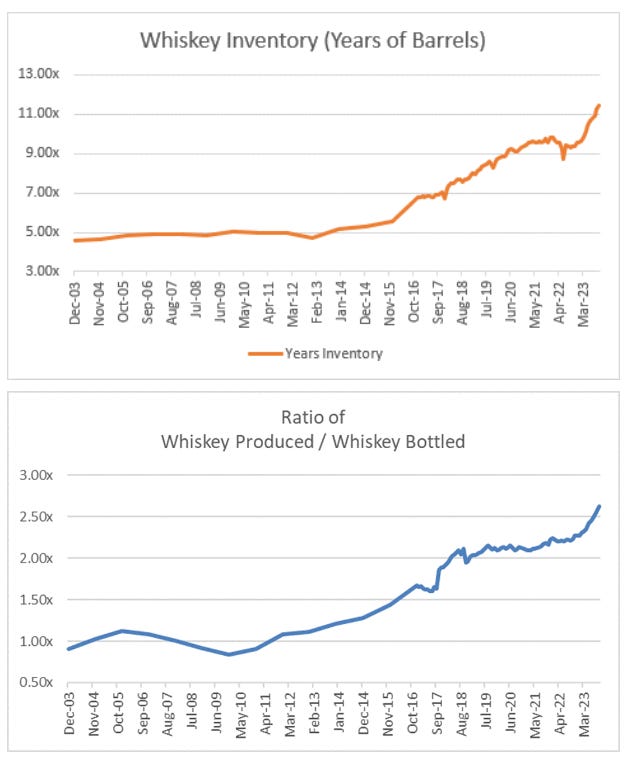

At its core, MGPI is a story of industry oversupply coupled with normalizing demand. VIC write-up author has done a great job of covering the supply situation, outlining unprecedented whiskey supply levels—see several charts from the original write-up below. Recall that the ratio of whiskey produced vs. whiskey bottled needs to be equal to 1 for inventories just to stabilize. Meanwhile, for a number of years prior to the mid-2010s, whiskey inventory regularly stood at around 5 years.

The oversupply risk was highlighted by an analyst during the recent conference call of Brown-Forman, one of MGPI’s competitors in the branded spirits business (see the below exchange). Interestingly, BF’s management hinted that the outlook for the American whiskey industry seems to hinge on expected consumer demand.

Question: And then, Lawson, maybe can you just give us a perspective as you're looking forward, I guess, this year, the category has been soft. Is your expectation in term -- and I'm really more focused on American Whiskey. Is the expectation that the current trends kind of hold for next year? Do you expect that the category to accelerate? And just to tie to that, Lawson, can you talk a little bit about the amount of inventory -- the industry inventory kind of sitting, I guess, aging at this point and whether we're at risk of, like an oversupply situation. We've had that question a couple of times, so it would be great to sort of get your perspective on it.

Answer: […] And then your other question about industry whiskey supply, I've seen a few people write things about that in the last few months. So it's something we track internally and have been for a long, long time as part of our planning processes. And a lot of it has to do with what you think the demand is going to be going forward, obviously. So for a long, long time, whiskey wasn't growing in the United States. It has for the, what, last 12 or 13 years, but we went through that 40-year window or it didn't grow at all. And so supply and demand were kind of equal. I think it depends on what you think the forward-looking demand number is going to be, but it doesn't seem to be that far out of line for us. We actually kind of have a different point of view on that than some of the folks that have written that.

Given that the the demand for American whiskey is a key part of the investment thesis here, I would like to expand on it a bit more, with a focus on elevated demand for whiskey post-Covid.

Put simply, an increase in demand for whiskey during Covid has been driven by higher time spent at home and stimulus money, leaving people with more time and funds to enjoy their hobbies. For more context, see several quotes below from a Reddit thread on the so-called bourbon bubble that are illustrative of the Covid-induced whiskey boom:

First, the pandemic changed things. <…> Basically with more free time and stimulus money, people had more time to get into hobbies, and bourbon was one of them. A manager of a local store told me that whisky sales increased 40% during the pandemic. Now that those conditions have changed, fewer people may discover the hobby. I think the pandemic bump will fade.

[…]

I think the current market is only a reflection of Bourbon being trendy. At some point, it won't be trendy anymore. As a KY native, it's pretty deeply ingrained in the culture. I grew up with it. My Dad has always been a Bourbon guy, and it was love at first sip for me. Bourbon was never 'cool' to me, just a homegrown product I enjoy.

Aside from personal anecdotes, this dynamic has been highlighted in multiple industry reports. For example, this WSJ article from Jan’21 outlined that the US sales of spirits, including whiskey, grew “at the fastest pace in decades” in 2020 as people were splurging on high-end spirits at home since they were unable to spend on concerts, travel, and other forms of live entertainment.

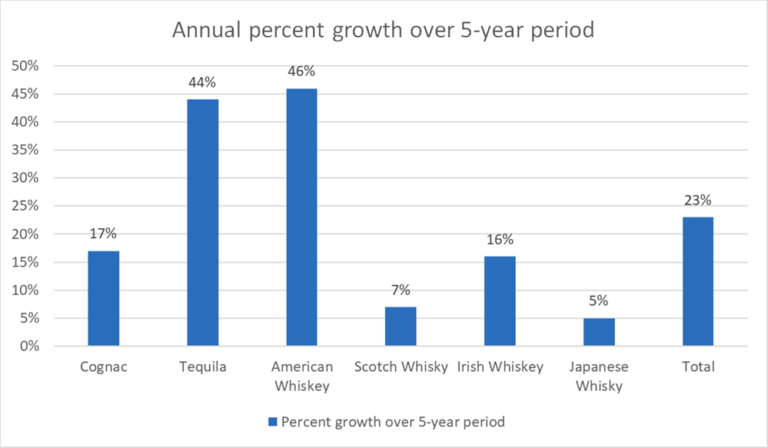

While the rapid growth was seen across the entire spirits category, industry data shows (see the chart below) that the growth of American whiskey sales outpaced all the other major spirit categories during 2017-2022.

The Covid-induced demand boost for American whiskey has been acknowledged by MGPI’s management - see the quote from the Nov’21 conference call below:

So in past quarters, we talked that we thought we were seeing a spike in demand in this particular -- in age, in particular, as a result of COVID. I still think that was contributed to some of the success we've seen.

The demand boost is clearly visible in MGPI’s historical revenues and margins (see the table below). While the company’s Distilling Solutions and Ingredient Solutions segments have historically been choppy growers, their topline growth accelerated with the onset of Covid, with 11-22% and 16-28% growth during 2021-2022 respectively for each segment. Similarly, both segment gross margins jumped materially during 2020-2022 from the stable levels seen during 2016-2019.

As explained by MGPI’s management, the improvement in margins with the onset of Covid has been driven largely by growing aged whiskey sales to an increasing number of customers. See the quote and the slide from November 2021 below.

And what this chart shows, if you look at the left side, that's the number of customers that we've sold to by quarter. And it goes all the way back to Q1 of 2018. And look at what happened starting in Q3 of 2020. So that's the combination of our brown goods customers, which includes new distillate and aged. And then if you look on the right side, you can see the impact that it's had on brown goods sales and then the overall segment of Distillery Products gross margin. And it's a direct correlation, right? This is being driven -- a lot of these sales are being driven by craft customers. So the craft customers business is doing extremely strong business right now. But we've also seen some of the bigger American Whiskey players knock on our door as they're starting to have supply issues with their liquid.

So I think it is safe to conclude that the jump in MGPI’s revenues and margins can largely be attributed to the Covid-induced demand boost.

The next logical question is whether we are already at the turning point in terms of consumer demand for American whiskey. Several aspects indicate that demand might be subsiding and the revenues/profitability of American whiskey producers might be on the decline.

One indication of a negatively inflecting industry is declining whiskey prices. As shown in the graph below from FRED, the producer price index for distilled whiskey and other liquor (excluding brandy) has declined materially by approximately 7% since mid-2023.

The unfavorable industry environment has been highlighted by Brown-Forman. The company has reported falling whiskey sales during several recent quarters, showing a 3% decline in FY24 (April 2024), driven largely by lower sales of Jack Daniel's Tennessee Whiskey (down 6% in FY24). Brown-Forman has highlighted normalizing consumer demand after several years of above-historical trend growth while hinting that distributor inventory levels (reflecting consumer demand) are likely to remain at current levels going forward. See the quotes below.

From Dec’23:

However, over the last couple of months, we have seen a slowdown in consumer spending similar to the trends we're seeing across total distilled spirits and other consumer packaged goods. After 2 years of strong growth, which was above our long-term historical trends, consumer demand for our brands is normalizing on this elevated base.

From Jun’24:

Throughout the year, we've been using the word normalization as we lapped the impact of the supply chain challenges and the rebuilding of inventory in the prior year as well as consumers getting back to historical consumption patterns. We expected our organic results to moderate in fiscal 2024 after 2-plus years of double-digit growth. However, as we move through the year, conditions changed, consumers faced higher inflation and increased interest rates that made them as well as distributors and retailers reconsider when and how they made purchases.

[…]

And then late summer, early fall, it fell sharply, and it caught everyone in our industry, including you all. I think everyone got caught up in it, and was surprised a bit by it. But I really do believe that it's really driven by inflation for the most part and then there was a level of demand that got pulled forward during COVID and that's the consumer element of it that we talked about last quarter, a lot on this conference call, where consumers had an extra bottle or 2 sitting in their cabinet at home and it's taken some time to work through that.

[…]

First, I'll speak to the significant amount of noise, if you will, created by changes in distributor inventories in the U.S. market for our business this fiscal year. We have been sharing with you throughout this fiscal year. In our first half, we cycled against the significant inventory rebuild during the same period last year. As we entered our second half takeaway trends for total distilled spirits and also for our business moved below the historical mid-single-digit range as consumer demand slowed. As consumer takeaway remains below its historical range, retailers have adjusted their inventory levels in response to the slower demand and the higher interest rate environment. Distributor inventory levels were largely at normal levels throughout fiscal 2024 with movement to the low end or just below the normal range in our fourth quarter. While we are on this topic, I will add here that in our outlook, the expectation is that distributor inventory levels will remain consistent with their current levels.

Softening consumer demand has also been highlighted by MGPI’s management - from the February 2024 conference call:

In closing, I would like to add that despite some reported softening within the Branded Spirits industry when compared to the COVID super cycle, we are very optimistic about the long-term health of this industry.

[…]

We get compared to the COVID super cycle, and those are great years for the industry. But if you start looking at what the industry is doing after 20-plus years of solid growth, and yes, it might have slowed a little bit in '22 versus '23, it's still a very, very healthy industry.

Finally, a number of media and analysis articles have underlined the same dynamics. For instance, see an excerpt from a Mises Institute article published in March:

“The phenomenal sales growth we saw during the pandemic was unprecedented and unpredictable but also unsustainable, and now, the spirits market is recalibrating,” Chris Swonger, the president of the Distilled Spirits Council of the United States, said last month. Those stimulus checks could buy a lot of Jack Daniels, or cause the more frugal drinker to pay more for Jack, instead of cheaper brands.

These points seem to confirm that the demand has already begun to normalize, thus supporting the investment thesis.

Valuation

Another important question is: where do we stand from a valuation perspective?

MGPI is currently trading at 9.9x TTM and 8.7x forward EBITDA. Triangulating the appropriate valuation multiple is not straightforward given that the company operates three distinct business segments and lacks publicly listed peers focused primarily on whiskey distilling solutions (as opposed to branded whiskey sales). However, here’s how MGPI’s valuation stacks up against public peers:

The closest, yet much larger, ($21bn market cap) and branded-spirits-focused peer, Brown-Forman (BF-B), is currently trading at 15.6x TTM EBITDA. BF has displayed significantly higher TTM EBITDA margins than MGPI, 36% vs. 24%.

Diageo, a much larger (£73bn market cap) and more diversified branded spirits producer (produces Johnnie Walker, Guinness, etc.), is trading at 12.9x TTM EBITDA. Diageo’s margins stood at 42%.

Pernod Ricard, another branded spirits behemoth (€34bn market cap), is trading at 13.7x TTM EBITDA. Pernod’s margins were at 28%.

Note that these comps are much larger, more diversified, and primarily focused on branded spirits (as opposed to primarily commoditized products for MGPI). So, the peers likely warrant a significant valuation premium to MGPI, suggesting that, at the current levels, MGPI might be valued fairly, if not overly generously.

Risks

One of the key risks for the investment thesis is secularly growing demand for whiskey. As detailed in a number of industry reports (e.g., here), the whiskey market is expected to grow rapidly, at a 12% CAGR during 2023-2033. This is expected to be driven by consumers shifting away from beer and wine, most notably among millennials who seem to be placing a premium on quality. This has been highlighted by MGPI’s management—see the quote from the Sep’22 conference call below:

Question: Okay. Great. So let's start high level. The spirits category has been growing at a strong mid- to high single-digit CAGR for some years now. It'd be helpful to get your view on the sustainability of the category trends, specifically the areas of your focus. And then also, if you've seen any change in demand or sales cadence over the past couple of months.

Answer: Okay. Yes, spirits, in general, what's been going on in the spirits category overall is over the last 10 years, spirits has been taking market share away from beer and wine. So spirits has taken about 10 share points away from beer and wine over the last 10 years. And within spirits, the 2 highest growth categories are American whiskeys and tequila. So that fits very well for both our Distilling Solutions segment on the American whiskey side and in our Branded Spirits business. Our portfolio where we really focus is on our what we call our premium plus brands. And within that, we have a nice portfolio of American whiskey brands as well as tequila brands.*

So we think that the spirits market share gains are taking away from beer and wine, if you will. We think that's going to continue for the foreseeable future. We think the trends that we're seeing in American whiskey growth as well as tequila growth is also going to be sustainable over the next several years. The reason for that is it's really -- you've probably heard the term the cocktail culture is what's really driving the spirits category overall. And the millennial generation is what's driving the cocktail culture, and these trends tend to be generationally linked. So we -- that's why we think that there's a pretty good runway ahead of us still in the spirits category.

So there is a risk that consumer demand for American whiskey will continue growing in the coming years and not turn out to be just a Covid-induced fad. However, what gives some confidence/margin of safety here is the fact that MGPI is largely a commodity service provider as opposed to a branded whiskey producer.

Another uncertainty for the setup is the trend of premiumization, whereby demand for higher-quality, longer-aged bottles increases at the expense of cheaper, less-aged whiskey. See the quote from Brown-Forman’s Sep’22 conference call:

Well, I mean, I think the premiumization trend is not just a COVID thing. I mean it certainly put it on a rocket ship a little bit, but the premiumization trends have been happening for 10 and 20 years in the spirits business. And so, when we think about our innovation pipeline, there is a bit of -- it's not about current economic conditions and what's going to sell in the next quarter. I mean that really doesn't enter into it when you're talking about the Jack Daniel's line extensions for example or first rule of super premium ones in 25 years. And so, these are really long-term plays, ones where we're trying to upscale the consumer a little bit within the Jack Daniel's franchise and let them really appreciate some really upper end of whiskeys. And so that -- those were things that were in the planning for a long time.

However, as argued in the initial post on MGPI, the impact of a growing share of premium-tier whiskey in the market on average aging times is likely to be marginal. With quite generous assumptions (i.e., that super-premium whiskey is aged for 10 years and that the share of super-premium-tier whiskey increases to 25%), the average required aging time would only increase from 4.3 to 5.5 years, still significantly below the current inventory levels.

Odds and Ends

In Nov’23, MGPI announced the retirement of its CEO David Colo. Mr. Colo joined MGPI’s board back in 2015 and has held the CEO role since 2020, orchestrating the company’s expansion into the branded spirits business.

MGPI’s management holds a sizable 36% ownership stake. It is held predominantly by the Lux family, who received their shares of MGPI as part of the 2021 acquisition of Luxco.

One factor that could reinforce the negative whiskey price inflection is the potential reinstatement of EU tariffs on US whiskey imports. First, a quick background: the EU imposed tariffs on US whiskey exports from 2018 to 2021, leading to significantly lower US whiskey exports. The tariff has been suspended since late 2022, with a 50% levy set to take effect in 2024; however, the suspension has recently been extended until Mar’25. There is a risk that the suspension might not be extended another time, particularly in the case of a potential cabinet change in the US. This would be important for the industry given that American whiskey exports account for approximately 25% of total industry revenues, with Europe being one of the key export markets.