Important Update on STKL

Additional research and thoughts on STKL

SunOpta (STKL) — initial post here

In this post, I am sharing my research and thoughts on SunOpta (STKL) and the broader plant-based milk space, as I have been taking a deeper look into the industry recently. My research confirms that plant-based milk prices have been declining and, thus, I think it is likely that we will see a deterioration in STKL’s margins and growth in the coming quarters.

But let’s take a step back. Fundamentally, STKL presents a way to bet on the expected downturn in the plant-based milk industry. While the market was historically under-supplied, explosive growth in plant-based milk demand during the pandemic prompted a significant supply increase from plant-based milk producers. The crux of the investment thesis is that, given the production capacity increase coupled with normalizing demand, the supply is expected to finally outstrip demand. This is likely to lead to lower prices and, thus, negatively impact producers’ growth and margins.

So the key question to ask here is, ‘Will/when will the pricing decline occur (or has pricing already inflected)?’.

Well, pricing is naturally a function of demand and supply. I will cover these in turn before assessing recent pricing dynamics.

Demand

Let’s start with demand.

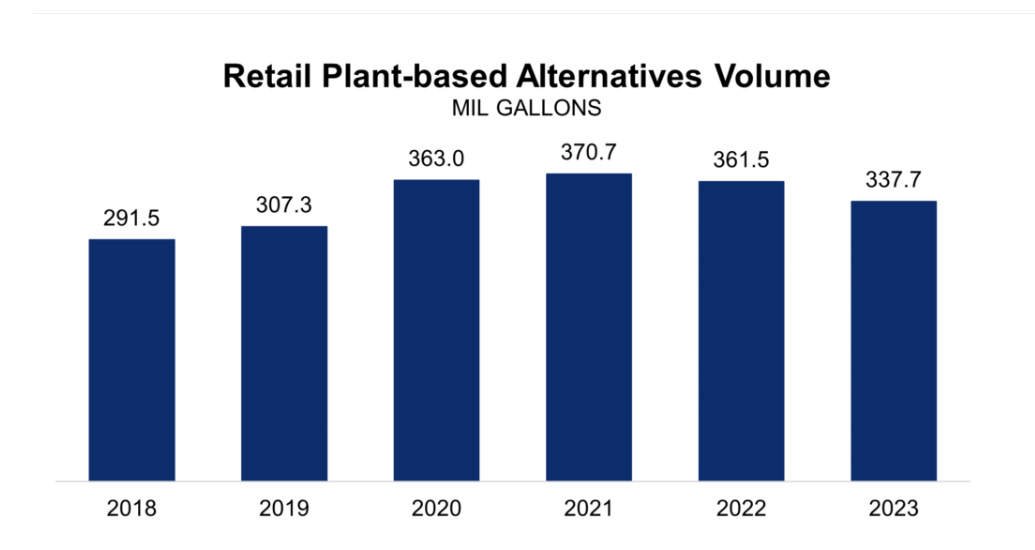

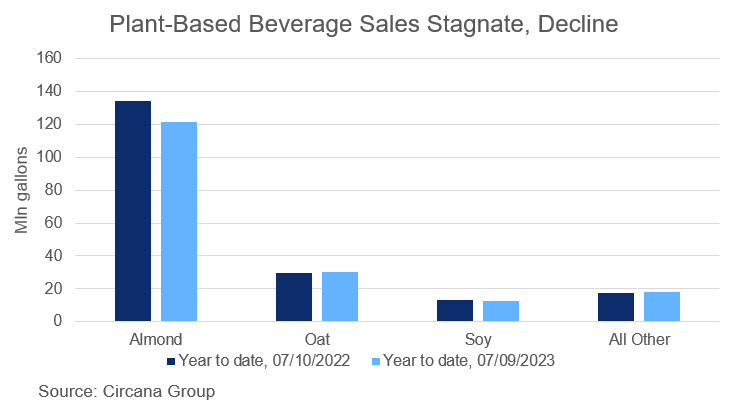

A look at recent-year plant-based milk retail demand volume data (see the chart below) clearly shows that demand peaked in 2021 and has since steadily declined, with a 7% volume decrease in 2023. This has been driven primarily by falling sales in the dominant almond milk sub-segment, while sales of oat, soy, and other plant-based milks have generally been flat (see the second chart below). This data suggests that the boost in plant-based milk demand during COVID was largely driven by the pandemic and that now the fad now appears to be subsiding.

While predicting future demand for plant-based milk is inherently difficult, given that it is a relatively new product with a relatively insignificant market share (<7%) and household penetration (53%), one could argue that there might be further growth runway. Note that the market share and household penetration are substantially below traditional dairy milk, which boasts 90% market share and 90%+ household penetration.

However, a counter-argument is that the falling demand for plant-based milk in recent years seems to have benefited traditional dairy milk. While total US milk retail sales have been declining over the last decade, they picked up in 2023, with dairy milk market share increasing from 89.9% in 2022 to 90.3%. Moreover, lactose-free milk sales have been on a steady uptrend in recent years (see the chart below), highlighting the increasing consumer preference towards shifting to lactose-free rather than plant-based milks.

Taking these points into account, it might be reasonable to conclude on a high level that the demand growth (in volumes) is likely to be minimal in the coming years. This suggests that using the 338 million gallons (or 1,278 million liters), the retail plant-based milk volume in 2023, as the normalized demand volume estimate is appropriate.

Supply

With the rough demand estimate on hand, the other key piece of the puzzle is figuring out how tight the market is from a supply perspective.

My research suggests that three key industry players, SunOpta, Oatly, and Califia Farms, alone cover approximately 80% of the estimated industry demand:

SunOpta — 600m liters. STKL operates four manufacturing facilities, including three legacy facilities (located in Minnesota, Pennsylvania, and California) and the Midlothian, Texas, facility, opened in 2023. Back in 2022, STKL highlighted that the company’s three older manufacturing facilities could produce "over 500 million liters per year" (see here, p. 55). As for the Midlothian plant, two lines are already operational, and the third one is ramping up and is likely to be at near-full production shortly (management previously guided for full production in mid-2024). While the company has not provided the production capacity for the Midlothian facility, I estimate that the plant will be able to produce 100 million liters annually when production by the third line has ramped up. This might be overly conservative, given that the plant boasts a square footage of 285k compared to approximately 600k for the three remaining facilities.

Oatly — 300m liters. OTLY operates two facilities located in Ogden, Utah, and Millville, New Jersey. At the time of its opening in 2019, the Millville facility produced approximately 34m liters annually, but the production capacity has since then been expanded and currently appears to be at 75m, based on several reports (here and here). Meanwhile, the Ogden facility had a capacity of 167m liters as of 2021. However, Oatly has since expanded the capacity of the plant to 225m liters.

Califia Farms — 100m liters. Back in 2017, Califia expanded its key manufacturing plant in Bakersfield, California, to 100k square feet, noting that the facility had a capacity of 400 bottles per minute. With reasonable assumptions (i.e., 40 oz average bottle, 16 hours per day, 300 days per year), this would imply a production capacity of approximately 100m liters.

The next logical question is, ‘What is the production capacity of the remaining players, including Chobani and Danone?’. The plant-based milk production capacity data of these producers have not been publicly disclosed, so it is admittedly more difficult to come up with an estimate.

However, one way of triangulating the unaccounted production capacity is to consider the market share of the remaining industry players. STKL’s management has highlighted that the size of the shelf-stable plant-based milk industry is approximately $1bn, which would imply a 50% market share held by STKL based on the company’s revenues from the plant-based beverages segment. Meanwhile, OTLY generated $224m in FY23 North America revenues, while Califia Farms’ estimated annual revenues are c. $80m. So, together, these three players hold around 80% of the market. Assuming the remaining 20% of the demand is fully supplied by the other producers would imply remaining production capacity of c. 256m liters. Adding this to the supply of STKL, OTLY and Califia Farms would imply total capacity of 1,256m liters versus industry demand of 1,278m liters. While this clearly is not a perfect way of figuring out industry supply, I think it is directionally indicative of the market being close to equilibrium.

Crucially, several aspects indicate that the supply might increase going forward:

Last year, Oatly completed an additional expansion of the Millville, New Jersey, plant, and production has been ramping up since (see the quote from the Mar’23 conference call). The expansion was expected to increase OTLY’s North American production capacity “by over 30%,” implying approximately 100m incremental supply. Given a lack of updates from the company on the expansion since early last year, it is possible that the production has already fully ramped up and thus the industry is already in oversupply.

Also, our Millville, New Jersey plant has added an additional oat-based production line which once it's fully ramped, will double Millville's oat-based production and increase America's capacity by over 30%. This capacity expansion is enabled by our strategic alliance with a local hybrid manufacturing partner.

SunOpta’s management has outlined intentions to open additional lines (4 and 5) in the recently opened Midlothian, Texas, facility within the facility’s current footprint (see the slide from Apr’23 below). STKL has also hinted that additional lines (6-8) would be opened when/if the facility is expanded. While the potential increase in production capacity has not been specified, the potential facility expansion would increase the square footage by 150k square feet compared to the current size of 285k, implying a substantial potential capacity increase.

Early last year, Danone announced a $65m expansion of its West Jacksonville facility, expected to be completed over “the next two years.” Aside from traditional dairy milk and ready-to-drink coffee products, the expansion was also related to the production of Danone’s plant-based creamers.

So it seems that the market is likely to become oversupplied over the near/medium term, if it is not already. An interesting aspect suggesting that the market might already be tight from a supply perspective is the fact that Oatly has recently decided to discontinue the construction of its facility in Fort Worth, Texas (production capacity of 150m liters). The construction of the facility was previously announced in 2021.

Pricing

The fact that the industry might already be at a tipping point is reflected in plant-based milk pricing. As shown in the chart below, the pricing for the two largest players, STKL and OTLY, has mostly declined throughout 2023 before entering negative territory in Q1’24.

Similar pricing dynamics have been highlighted by STKL’s other competitor Danone which earlier this year stated the following:

We went a bit too far in terms of pricing last year. We need to price correct that and to be again competitive versus competition. We did that at the back end of the Q4.

The recent weakness in pricing has been driven largely by the deteriorating performance of the retail (i.e. tracked) sales channel due to increasing competition. In Nov’23, STKL’s CEO stated that “many of our customers have forecasted further declines in 2024 as it relates to the SKUs that they sell into the retail channel.” At the time, the CEO also noted that he expects competition in the retail channel to intensify in 2024, with expected higher promotional activity. See also this exchange from STKL’s Q1’24 conference call:

Question: It sounds like the growth was broad-based, but I'm curious, as you communicated that prices have come down a little bit. I mean, have you seen any improvement in the track channels?

Answer: Ryan, I appreciate the question on tracked channels. We have seen -- I wouldn't say go so far as to say we've seen improvement in the tracked channels. You see a little bit of volatility. You see a little bit of promotion.

At the same time, however, STKL has tried to downplay the weakness in the retail channel by highlighting the strong growth in the foodservice (i.e., coffee shop) channel - see several quotes illustrating this below.

From Q1’24 conference call:

Remember, we have a really diverse revenue stream. Channels are diverse, customers diverse, products are diverse. I mean our foodservice channel grew 11% in the quarter. Our top three customers, each of them grew over 10% plus in the quarter. So, we've got a lot of diversity. And I think that's one thing that we've gained confidence in.

From Q2’23 conference call:

I mean, we're definitely seeing more bifurcation in performance between foodservice and retail. I think it's possible the consumer is just less price sensitive when they're in a coffee shop ordering their favorite drink versus in a grocery store where they have a basket of items, they need to purchase to feed themselves and their family. And so maybe there's just more price sensitivity in a retail environment than there is at the drive-thru for your morning oat milk latte. But that is definitely something we're seeing. And we haven't seen any signs of a slowdown, as I mentioned, where we do have good visibility into the data in foodservice, we're seeing low double-digit growth.

Strong performance in the foodservice channel has also been highlighted by OTLY - see this exchange from Q1’24 conference call below:

Question: It's encouraging to see your share gains in the US and Europe, also encouraging to see progress within oat milk as a category in these regions. I just wanted to dig a little deeper into what you're seeing in plant-based milk in general that's leading it to be, I guess, somewhat flattish in Europe as you reported it and down low single digits in the US? Are there any concerns you have about the category? And what do you believe needs to happen for the category? And I'm talking just broad plant-based milk to expand again at a fairly rapid pace in these regions.

Answer: Listen, no, we're pleased with what we see, right? But this is the way in which we would like you to think about it, which is, let us not take scan data at sales value to judge how the category is developing. Scan data is not fully representative of the total category growth. Two very important facts that underpin that can. Number one, there is a growing defecation between plant-based drinks, the oat mill category and the Oatly brands, and you picked up on that. Oat milk continues to outgrow plant-based in general and Oatly outgrows both categories consistently. And we continue to see the gain -- the share gains in both regions. So that is something that is growing, it's a growing trend.

And second of all, for the non-measured channels in Foodservice, as we have been working consistently for quarters now, you will remember, both Europe growing above 20% and the US growing above 35% about -- outside our largest customer are the proof that the category is in good growth. So as you say, we are -- and as you saw, we are very selective in the way we drive growth in the food service channel, balancing growth and margin. So, what we're doing at the moment instead of figuring out what to do according to scan data, we're head down, controlling the controllable. Just like we said we would quarters ago, gaining distribution, driving strong velocities, introducing gray new products for new occasions and investing more and consistently behind the brand. So besides driving disproportionate foodservice growth and launching in new markets, right, in a very disciplined and asset-light manner. So the way we see this is that what we're doing is working, and there's more to come.

Why is this important? Well, STKL’s management has highlighted that the foodservice channel is “at least 4x larger” than the tracked (i.e., retail) channels and is “the most important driver of volume” for the company. This would suggest that the performance of the foodservice channel might more than offset the weaker retail performance and thus lead to improved pricing or at least slow down pricing declines.

However, given the tapering pricing for the key industry players despite solid foodservice channel growth, I do not think this is or will be the case. It seems that STKL’s management might be trying to paint too rosy a picture here, obscuring the underlying pricing deterioration by overstating the importance and size of the foodservice channel. While STKL has not disclosed the share of revenues generated from the coffee shops channel, peer OTLY generates c. 36% of its sales from foodservice (see here, p. 15). This, coupled with the hard evidence of declining pricing, suggests that a substantial portion of STKL’s sales are likely generated from the retail channel where producers have been facing increasing price pressure.

Conclusion

My additional research suggests that the plant-based milk industry is likely close to tipping from under-supplied to over-supplied, indicating that the investment thesis is intact. With STKL trading at 13x TTM EBITDA, despite its struggles with profitability and cash flow generation and a choppy history of growth, I continue to like the setup and have maintained the short position.