Cheap, Well-Managed O&G Producer on the Cusp of an Inflection

Revealing my latest portfolio addition

Today, I am back with a new portfolio idea: International Petroleum Corporation (IPCO-TO). I think IPCO presents a compelling opportunity to invest in a cheap O&G producer with interesting growth optionality — a large, development-stage asset expected to go online in 2026 — for which investors are currently paying little. With the anticipated significant ramp-up in production and a substantial decline in growth capex, we are likely to see a major inflection in the company’s free cash flow generation in the coming years. While there are plenty of O&G exploration and production companies trading at undemanding multiples with potentially large growth assets, what makes IPCO stand out is that the company’s major shareholder-operator is the prominent Lundin family. The family boasts an impressive value creation track record within IPCO and the broader industry, including completing value-accretive acquisitions, delivering on large development projects, and pursuing regular share buybacks. Even if higher free cash flow generation doesn’t lead to a re-rating of the stock, I would expect management to continue pursuing significant stock repurchases, creating upward pressure on the share price.

IPCO initially caught my attention during the recent RV Capital investor conference, which featured a discussion with IPCO’s CEO, Will Lundin. The investment thesis has also been laid out nicely in RV Capital’s H1’24 investor letter. I would highly recommend checking out both the conference discussion and RV Capital’s pitch for those interested in the setup.

Now, let’s dive into the investment idea.

International Petroleum Corporation (IPCO-TO)

Elevator pitch: A cheap, well-managed O&G producer on the cusp of a cash flow generation inflection.

Current price: C$18.89

Target price: C$27+

International Petroleum Corporation is an O&G producer with operational assets in Canada, Malaysia, and France. The vast majority, over 85%, of the company’s production comes from assets located in Canada, with a 60/40 production split between crude oil and natural gas within the Canadian assets (see the slide below). Most of IPCO’s operational assets are low-decline, displaying consistent production over the recent years, with 2024 production at 47k barrels of oil equivalent per day (boepd, see the slide below).

The company’s key growth asset is Blackrod, a development-stage oil sands project located in Alberta, Canada. IPCO launched phase 1 of the commercial drilling program in 2023, with first oil expected in late 2026 and production anticipated to reach around 30k boepd by 2028. Management has stated that it intends to spend c. $850m in capex for phase 1 development. IPCO has the option to potentially pursue further development at Blackrod, with regulatory approvals secured for up to 80k boepd of production.

IPCO presents an attractive way to invest in the energy space, given the company's cheap valuation. At current stock price levels, IPCO is trading at 5.5x 2024 EBITDA and 7.7x FCF (excluding Blackrod capex). I think these are undemanding multiples, considering that the company operates long reserve life and low-decline assets. To illustrate long reserve life, IPCO boasts a 2P (proved + probable) reserve life index of 31 years. This is substantially above the 19 and 16 years for Canada-focused public comps WCP-TO and VRN-TO, respectively, which are trading at comparable/higher 12x and 8x TTM P/FCF multiples. As for the decline rates, IPCO has displayed annual reserve decline rates of 10-15%. As shown in the chart below (from this article), IPCO’s annual reserve decline rates are on the lower end of producers operating in Southeast Alberta (where a significant portion of IPCO’s assets are located) and are below the average decline rates of 17-23% for these producers as of 2022. I would also highlight that the reserve decline rates of VRN and WCP have been higher, at 15-35% and 24%, respectively.

IPCO is also cheap based on the estimated value of the company’s reserves. The stock is currently trading at a 46% discount to the NAV ($3.1bn) which represents the after-tax NPV-10 of the company’s 2P reserves as of Dec’24. I would note that the NPV was estimated using a Brent oil price of $75/bbl in 2025 and $80 in 2026/2027 (so broadly in line with current levels), with the price increasing by 2% annually thereafter.

But what makes IPCO most interesting is that these valuations—based on earnings/cash flow and NAV—assign limited value to IPCO’s key growth asset, Blackrod. From an earnings/cash flow perspective, IPCO’s management expects Blackrod to have a WTI break-even level of $50/bbl, with production at 30k boepd. Assuming FCF conversion in line with 2024, this would imply that, at current oil prices, the company could generate over $160m in incremental annual FCF from Blackrod once phase 1 fully ramps up (compared to $216m in total 2024 FCF). Adjusted for the anticipated ~30% decline in base asset production until Blackrod reaches the 30k boepd production target, the company is likely to produce c. $300m in total normalized annual FCF, implying a 5.5x P/FCF multiple. And this FCF estimate might be too conservative—while it aligns with the average annual free cash flow implied by management’s 2025-2029 FCF forecast (at $75/bbl oil price levels), Blackrod likely won’t reach peak phase 1 production until 2027–2028.

As for the valuation on a net asset value basis, while a significant portion of IPCO’s NAV is comprised of Blackrod 2P reserves, the NAV does not include the project’s contingent resources. And these are massive: Blackrod’s contingent resources stood at 1025m boe as of Dec’24, compared to 493m boe in IPCO’s 2P reserves. Assuming the company can successfully convert just 10%—or 103m boe—of the contingent resources into 2P reserves down the road (compared to 216m boe converted in 2022 and 40m boe in 2024), this would boost 2P reserves by around 20%, significantly extending the company’s reserve life index.

Now, let me note that I do not have high conviction on whether 1) Blackrod production and break-even levels can reach management’s targets, and 2) the company can successfully explore the contingent resources to convert a part of them into 2P reserves. Nonetheless, given the current undemanding valuation of IPCO’s base business, I think it’s reasonable to state that investors are paying little for the Blackrod growth optionality.

What could be the potential upside here? I think a useful framework is the SOTP approach, valuing Blackrod and the base business separately. IPCO’s management has highlighted that the NPV-10 of Blackrod is $1.4bn as of Jan’25, or 75% of company’s current EV. Now, the NPV-10 figure is admittedly hard to verify for outsiders, so to be conservative, you could simply value the Blackrod project at cost (c. $600m in capex spent so far), implicitly assuming that the company has not and will not create any value with the asset development. In this scenario, the remaining base business would be valued at $1263m, or 3.8x 2024 EBITDA and 4.9x 2024 FCF ex-Blackrod capex. A potential re-rating to a more reasonable, yet still undemanding, 8x FCF would imply a share price target of around C$27/share, or a 40%+ upside.

So, that’s a quick overview of the IPCO investment thesis. If I had to summarize it in a couple of sentences, it would be this: IPCO is cheap from several angles, while investors are currently paying little for the Blackrod growth optionality. With conservative assumptions, there might be a 40%+ upside from the current stock price levels.

At this point, reasonable pushback against the investment thesis you might have could go along these lines: ‘There are plenty of O&G companies trading at undemanding multiples with significant growth assets. The problem, however, is that the industry is well-known for management teams that 1) are promotional, with super bullish outlooks implying multi-bagger upside, and 2) have sub-par capital allocation track records, including pursuing value-destructive acquisitions. So, whenever investing in such setups, there are risks that 1) the growth asset might not be developed successfully or reach management’s production/break-even level/capex expectations, and 2) even if the asset development is successful, management might waste generated cash, for instance, on value-destructive acquisitions. So, what makes IPCO different, and why is this not the regular O&G company and not the usual ‘putting dollar in the ground’ situation?’

Well, I think there are two aspects that separate IPCO from the rest of the pack: namely, the Lundin family’s value creation track record and RV Capital’s involvement.

Let’s start with what I consider the key aspect — the Lundin family’s track record. For some background, the Lundin family is the major shareholder of IPCO, holding 34% of outstanding shares and controlling two board seats, including the CEO’s role. The Lundin family boasts an impressive track record as an owner-operator in a number of O&G companies. I would highlight the family’s solid history with IPCO’s former parent company, Lundin Petroleum (later renamed Lundin Energy). After the public listing in 2001 at SEK 3/share, the company’s share price rose over the ensuing decades, before Lundin Petroleum was eventually acquired by Aker BP in 2022 at SEK 400/share, delivering a 175x return to equity holders who held onto the stock during that period. Here, I would note that several former Lundin Petroleum management team members have joined IPCO, including Lundin Energy’s CEO (now IPCO’s chairman) and CFO (a board member), among several other former Lundin Energy executives.

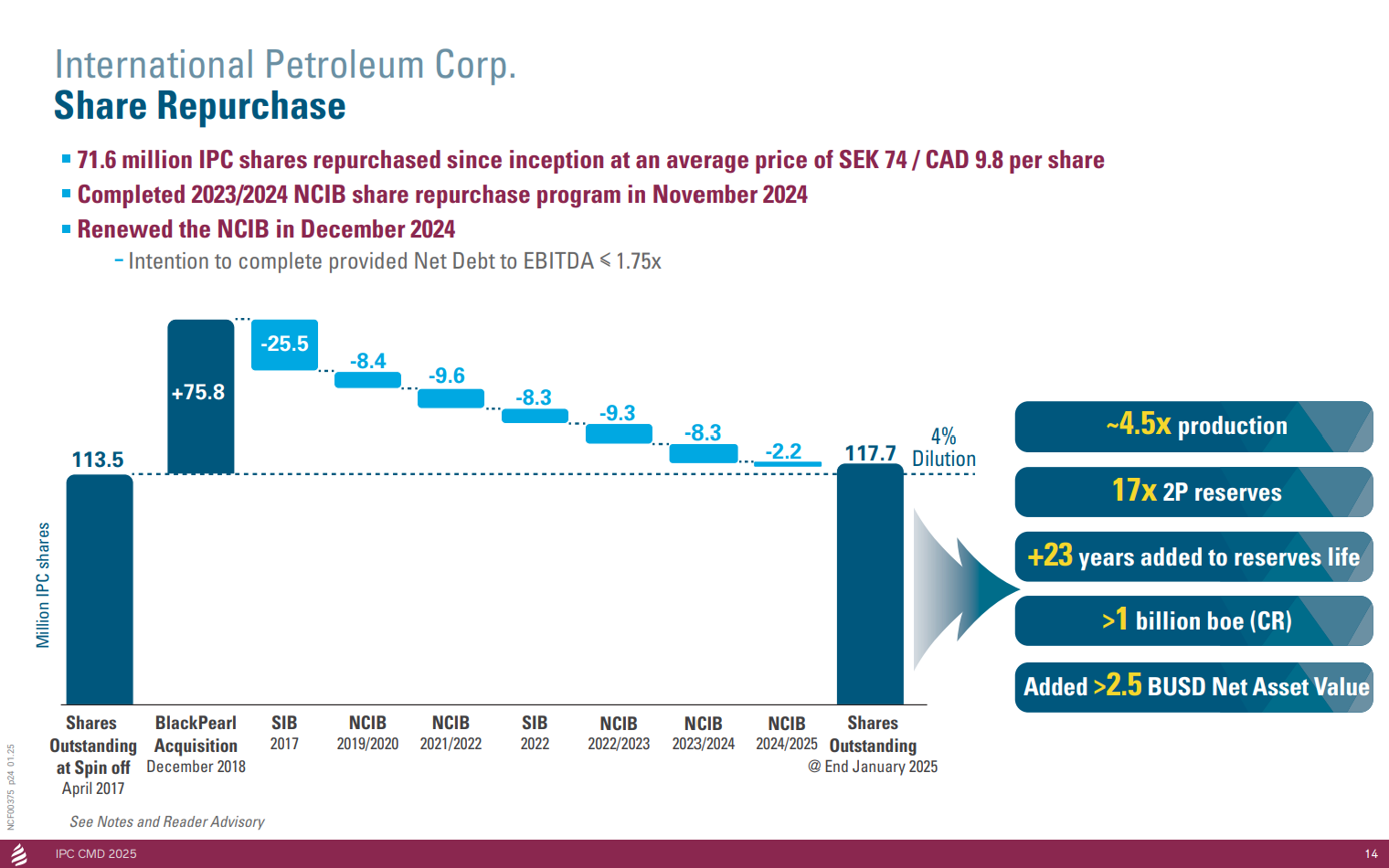

And the management team has successfully re-created Lundin Petroleum’s success at IPCO, as reflected in the 3.5x share price increase since its spin-off in 2017. How did the leadership achieve this? The key aspect here is that IPCO’s management has displayed solid capital allocation, with value-accretive acquisitions and regular buybacks. Since the spin-off, IPCO has completed five acquisitions, boosting company’s production and reserves by 4.5x and 17x, respectively. Management has highlighted that the company has already generated $1060m in FCF from the acquisitions, compared to a $938m total acquisition price, with NAV contribution at over $2.7bn (see another slide below). To illustrate management’s shrewdness in pursuing M&A, I would highlight the acquisitions of Suffield and BlackPearl Resources (which owned the Blackrod asset), announced in 2017 and 2018. Given the depressed oil/gas price environment and a forced seller in the case of Suffield, IPCO acquired the assets at a substantial discount to their NPVs. What is equally impressive is that, as shown in the slide above, IPCO’s management has been consistently buying back stock. Since 2017, the company has repurchased 71m shares, or 37% of its outstanding shares, right after the 2018 stock-for-stock acquisition of BlackPearl Resources, at an average price around 50% below current levels.

So, I think it’s fair to say that IPCO’s management is laser-focused on shareholder value, suggesting that we are unlikely to see any value-destructive acquisitions while the company will continue to buy back shares.

But an equally important aspect, given the ongoing Blackrod development, is management’s track record in successfully developing large O&G assets. As shown in the slide below, the Lundin family companies have, over the years, successfully explored and brought into production a number of large projects.

Here, I would like to elaborate on the Johan Sverdrup oil field, as I think it’s an interesting case study of the Lundin family’s track record and the market’s skepticism regarding the asset’s development. For a quick background, Johan Sverdrup was one of the largest oil discoveries in the Norwegian Continental Shelf in decades, made by Lundin Petroleum back in 2010. Subsequently, in 2015, together with partners/stakeholders, including the operator Equinor, the phase 1 development of the field was announced, with first oil expected in 2019. Similar to Blackrod, the asset’s potential impact on Lundin Petroleum’s performance was seemingly underappreciated by the market. While Lundin Petroleum’s stock price gradually rose from 2015 through 2017, the market was slow to appropriately value the looming production and FCF inflection (the field would nearly double the company’s production), with the company trading at a low-single-digit multiple of Johan Sverdrup’s EBITDA contribution alone. As the market became increasingly aware of the production and cash flow generation given ongoing development progress, Lundin Petroleum’s stock re-rated to significantly higher levels in 2018-2019 (about 3x higher compared to 2015). The phase 1 development was eventually completed in 2019, ahead of schedule and below budget.

Now, I must note that the Johan Sverdrup precedent is not directly comparable to the ongoing Blackrod development. While the Johan Sverdrup field was multiple times larger than Blackrod, it was located in a different geography, and Lundin Petroleum was not the asset’s operator. Nonetheless, I think this illustrates the Lundin family’s track record of delivering on large, transformative growth projects.

Let’s now quickly discuss another aspect that makes IPCO more attractive than a typical O&G producer: the presence of RV Capital on the shareholder register. RV Capital, run by prominent investor Rob Vinall, boasts an impressive track record, with its Business Owner Fund compounding at a 16.6% CAGR (after fees) since inception in 2008, as of Dec’24. As highlighted in the fund’s H1’24 letter, IPCO marks the fund’s first investment in an O&G company. While Rob has noted that he has long considered the O&G sector interesting, what kept him on the sidelines was the lack of “good long-term owners and managers.” Given the historical performance and selectiveness of RV Capital, I believe the fund’s presence is a significant positive, confirming that IPCO is not just a typical O&G name but one with a solid and highly motivated management team.

So, that’s an overview of the investment thesis. What follows is a quick overview of several noteworthy risks.

Operational issues/delays/cost overruns at Blackrod. One of the key risks to the setup is potential issues in Blackrod development, leading to delays and/or cost overruns. While there’s clearly development risk, I would note that Blackrod development has been progressing successfully so far. IPCO has already completed several pilot programs at Blackrod (drilling initiated in 2011, 2013, and 2019), including building/modifying a pilot facility to test the SAGD technology. Management has noted that the pilot programs have been successful, with initial production rates from the third pilot drilling program being “very positive” and “running ahead of expectation.” More recently, IPCO’s management has highlighted that the facility construction and drilling have seen good progress, with the development going according to plan (see the quote from the Q3’24 conference below).

The facility construction continues to see good progress. As you can see on the picture at the bottom left-hand side of the slide, an aerial shot of the plot plan. You can see a lot of activity and moving parts there. We have a lot of packaged equipment that's been delivered to site and over 300 pieces of equipment have been ordered.

So the procurement is well on track here and moving up to the top right-hand picture of the slide, you can see one of the inlet degassers, so one of our process modules being delivered to site. And further on in the pictures below that, the tank farms pretty much fully erected at this point in time. We have pipe rack modules being delivered to site and things continue to ramp up as well on the civil work side with the access road being largely completed at this point in time. Some piling works is still taking place in anticipation of modules to be delivered within the central processing facility area.

On the drilling side, we're advancing at a great rate here. We're still on the second super pad here where we're drilling 16 well pairs. Our first production pad, which is 14 well pairs at Pad B is largely finished. And now the second super pad is about 50% complete, which is 16 well pairs. So that continues to progress in line, if not ahead of expectation.

And looking at the schedule now for Blackrod, again, it's all coming together this year with the peak investment program, touched on the civil works and the road works largely being completed at this point in time. The facilities work scope continues to move in accordance with plan, detailed sequencing of events and turning around the equipment from the fabrication shop to site is key to the success of the overall build of this project. And the drilling continues to go well. Our midstream pipelines are also progressing and tracking along as expected. So we're expecting to be commissioning during the winter period of 2025, 2026 with first steam to follow around Q1 of 2026 and first oil expected later on in 2026.

Another aspect is that the Lundin family has experience in successfully developing similar assets. Here, I would highlight IPCO’s similar (in terms of thermal recovery method) Onion Lake development project, where phase 1 was completed in 2015. The project was developed by BlackPearl Resources (subsequently acquired by IPCO), with the Lundin family being a major shareholder in BPR before the acquisition.

As for potential capex overruns, these are admittedly a risk. I would highlight that in 2022 IPCO’s management expected phase 1 development to cost $540m (see Q2’22 conference call) before subsequently revising it to $850m. However, the increase has been largely explained by ensuing broader cost inflation. Given that the $850m phase 1 capex guidance has remained unchanged since early 2023 and that the majority of capex has already been spent, it seems that any significant cost overruns are unlikely.

Oil and natural gas price volatility. Another key risk is the potential oil and gas price volatility. While this is hard to predict, at the current what I’d call depressed oil price levels, as noted above, IPCO is set to generate ample cash flows in the coming years. Management’s 2025-2029 FCF guidance (which includes Blackrod growth capex) suggests the company is likely to generate more than half of the current market cap/EV in FCF over these five years. Given that most of this cash is likely to be returned to equity holders in the form of stock buybacks and potentially dividends, I think it’s fair to say that investors are getting a cheap option on any further cash flows to be generated by the company.

Too optimistic NAV estimate. As discussed above, IPCO’s NAV extends beyond proved (1P) reserves by incorporating probable/proved undeveloped reserves into the NAV, which might be overly optimistic. If the NAV were estimated using solely proved resources, the NPV-10 would come out at $2.4bn, implying a materially lower 22% discount to NAV. Nonetheless, given that the company’s historical cumulative production has consistently exceeded proved reserves, I believe including IPCO’s 2P reserves in the NAV is reasonable.

Great analysis!