Brief Update On SMLP C-Corp Conversion

Latest on SMLP

Summit Midstream Partners (SMLP) — initial post here, last update here

I am sharing a brief update on SMLP as the company has recently released a press release, proxy, and presentation related to the planned C-Corp conversion. You can find links to the filings here: press release, presentation, and proxy.

The key takeaways are as follows:

The shareholder vote to approve the C-Corp conversion has been scheduled for July 18 (record date set to June 7).

The conversion is expected to be completed after shareholder approval, in H2’24.

Aside from these, SMLP’s management provided additional color on the key reasons for the C-Corp conversion, namely increased trading liquidity, potential index inclusion, tax benefits for unitholders, and a simplified business structure with reduced administrative burden.

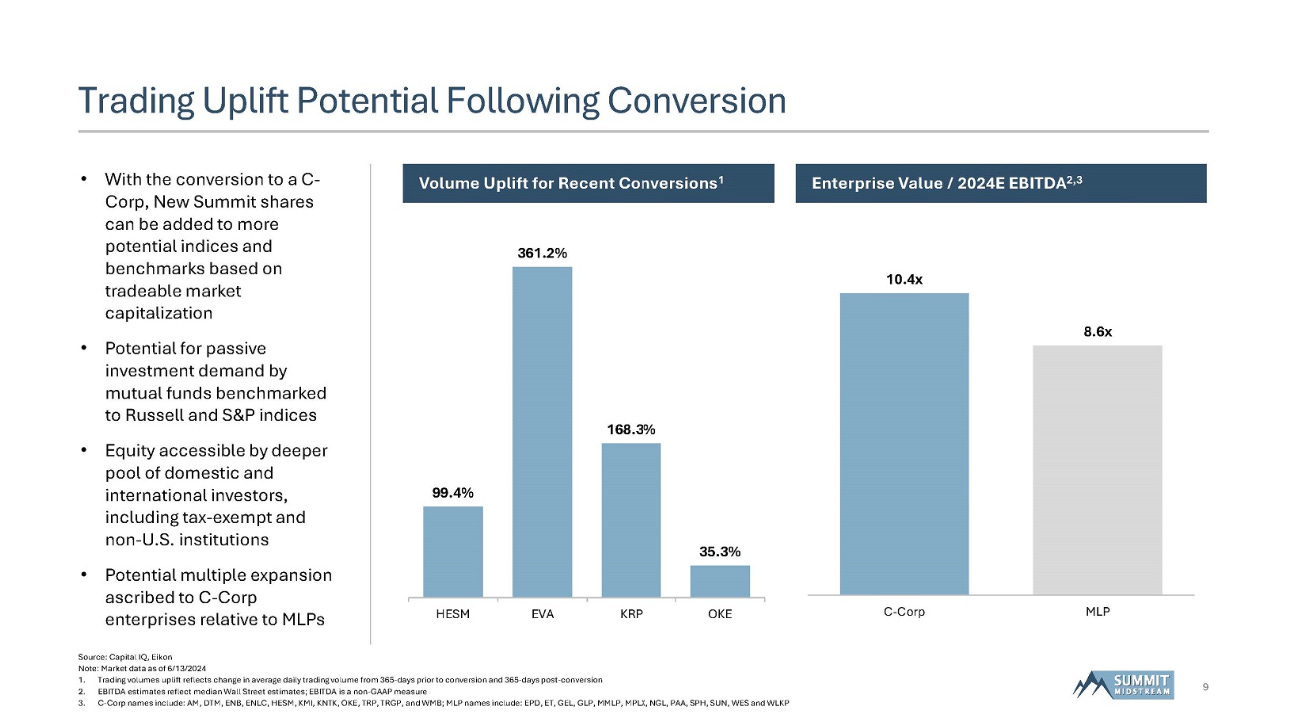

Regarding increased trading liquidity and potential index inclusion, management’s deck contains several interesting charts highlighting the volume uplift in other precedent MLP-to-C-Corp conversions (see the slide below). Three precedent conversions, HESM, EVA, and KRP, have seen 99-361% volume increases, while the trading volumes of the other remaining MLP-turned-C-Corp, OKE, increased by 36%. Company’s presentation also shows that publicly listed C-Corps have been trading at a higher average forward EBITDA multiple (10.4x) versus comparable MLPs (8.6x).

A similar volume and valuation uplift might be likely for SMLP, given the potential index demand after the C-Corp conversion is completed. Management expects potential Russell 2000/3000 inclusion to result in index demand of c. 12% of the float while there is also a possibility of SMLP getting included into other indices down the road, such as the S&P 600 Small Cap index (potential demand for c. 13% of the float).

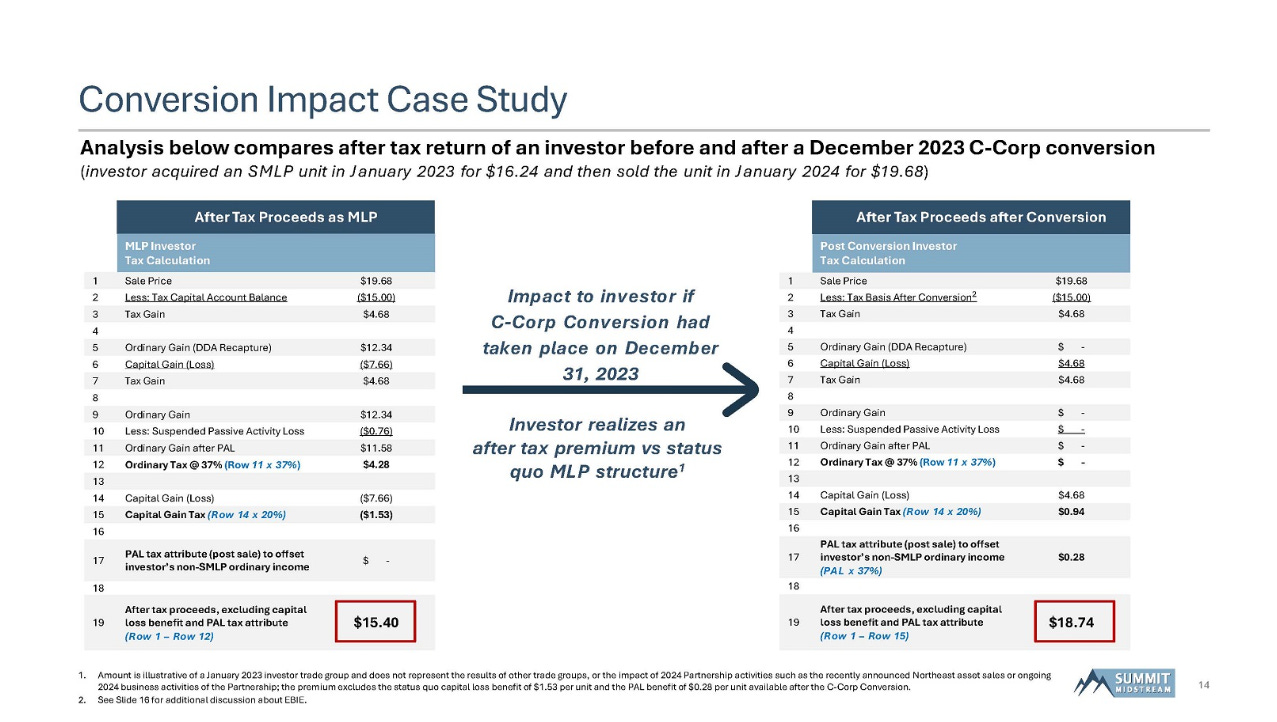

As for the tax benefits for unitholders, the majority of unitholders are expected to have no taxable gain resulting from the proposed exchange. Crucially, the conversion would eliminate the need for unitholders to pay taxes at the individual investor level (as high as a 37% marginal federal income tax rate) as opposed to corporate income taxes at the C-Corp level (21%). As an illustration, the company has highlighted the materially lower tax burden if SMLP were a C-Corp for an investor that hypothetically held SMLP shares from Jan’23 through Jan’24 (see the slide below).

Given these benefits of the conversion, coupled with the expected business simplification, I think that the equity holder vote is largely a formality and any opposition is highly unlikely. While there is a risk that the conversion might not get approved given that non-votes will be registered as opposing votes, it seems minimal given solid shareholder participation in SMLP’s most recent shareholder meeting where 73% of shareholders voted for the appointment of a public accounting firm (see here).

Despite the looming near-term catalyst, SMLP shares have barely budged since the release of the proxy/presentation/press release, and the company remains cheap, trading at only 6.4x 2024E EBITDA (at the mid-point). As noted previously, this is substantially below peers trading at 8x+ multiples and comparable industry transactions completed at 10x+ multiples. I’d expect the pending C-Corp conversion to help bridge some of that gap. Given SMLP’s high leverage, even a relatively insignificant 1-turn increase in the multiple would imply a share price target of $50 (vs. $33.37 currently).

Considering the setup’s attractiveness, I continue to like SMLP and will continue holding the position until further developments.

If the only thing that's considered good news for a business is a change in its tax structure you're reaching. There are other companies with more potential than this one.