Actionable Investment Ideas #17

Actionable Investment Ideas #17

Includes HOLI, CRH, COIN (short), MLP and SXP:TO

In this newsletter, I share the most intriguing investment ideas I've come across in the past week from a variety of sources, including Value Investors Club, various investing blogs, hedge fund letters, and more. I aim to present you with concise and easily digestible investment idea summaries that quickly capture the essence of the thesis.

This week's newsletter includes:

Hollysys Automation Technologies (HOLI) - Prolonged takeover saga coming to an end.

CRH (CRH) - A cheap bet on US infrastructure tailwinds.

Short Idea: Coinbase (COIN) - Cryptocurrency exchange likely to face significant competitive pressures.

Maui Land & Pineapple Company (MLP) - Hawaii land owner trading at a wide discount to NAV.

Supremex (SXP:TO) - Cheap envelope manufacturer at a cyclical trough.

Thank you very much for reading and subscribing to my newsletter. I hope you'll find Idea Hive to be a valuable tool for your investment research. If you do, I'd appreciate it if you could share the newsletter with your friends and colleagues.

Hollysys Automation Technologies (HOLI, $1.4bn)

This idea was posted on the Special Situation Investments blog by my friend Dalius. Currently, Dalius is running a Black Friday special offer and you can sign up for one-month free trial. I am a sub and can recommend it.

Now onto the investment idea.

Hollysys Automation Technologies is a Chinese US-listed company that provides automation control system solutions. The company looks likely to get sold in short order. After recently launching a formal sale process, the company has received several takeover bids. These include acquisition proposals from its two co-COOs at $25/share, a buyer consortium led by Recco Control Technology at $26.5/share, and Chinese PE firm Ascendent Capital Partners at $26/share. Hollysys has recently said that the sale process is progressing well, with certain bidders proceeding to confirmatory due diligence and negotiating definitive agreements. The company expects to be in a position to execute a merger agreement by mid-December.

The spread to the highest bid currently stands at a quite wide 14%. The market is understandably cautious about whether a transaction will eventually materialize here. Over the last several years, the company has been in the midst of a prolonged takeover saga, but the company sale eventually failed to come to fruition.

However, it seems that this time the outcome will be different. The recent strategic review comes in response to pushback from a large group of equity holders fed up with the prolonged buyout saga. Management will likely have a hard time wiggling out of the company sale. Hollysys' board has recently confirmed that it will hold a special meeting to vote on activist board nominees. The vote could give the activists (own 46% of outstanding shares) a majority control of the board. The activist group includes some reputable names including Oasis Management which is one of the most prominent Asian activist hedge funds. So it seems that even if the sale of the company does not materialize shortly, Hollysys would likely get sold after the equity holder meeting.

Full HOLI write-up on Special Situation Investments.

CRH (CRH, $44.1bn)

CRH is one of the largest construction material companies across the US and Europe. It specializes in producing essential materials such as aggregates, cement, and asphalt.

The company offers the opportunity to ride the wave of increased investment in US infrastructure. Recent unprecedented government spending programs, including IRA, IIJA, and CHIPS, are set to inject significant funds into infrastructure projects. Experts predict a remarkable 19%+ annual growth in spending across various non-residential construction sectors until 2030.

CRH seems to be the best choice for capitalizing on the industry tailwinds. As one of the largest building materials businesses in North America, CRH may be the single largest beneficiary of the spending bills. For example, c. $350bn in IIJA funds is earmarked for the construction of highways whereas CRH is the top road paver in the US. CRH will also disproportionately benefit from $200bn+ in major onshoring-related commercial projects.

But the current valuation does not align with these dynamics. CRH is trading at 12x 2024 P/E and 7x EV/EBITDA. This is way below the peer group trading at 18-28x and 10-15x multiples respectively. Such valuation discount seems unjustified. CRH is the best-in-class operator, demonstrating much lower leverage, better cash flow conversion, and higher returns on invested capital compared to peers.

Why does the opportunity exist? One of the explanations is that CRH, primarily a North American business, was relisted from the London Stock Exchange to the NYSE only a couple of months ago. This is likely to attract more investors over the next year, prompting a reevaluation of the stock closer to US peer valuations rather than being stuck with European comp valuations. Additional stock price boost could come from CRH's inclusion in major US-based indices like the S&P 500. This is expected after the company files its 2023 annual report around Mar’24.

CRH has historically traded at 20-30x NTM P/E. Valuing the company at the lower end of this range would suggest a price target of $120/share or a 93% upside.

Full CRH write-up from Voss Capital.

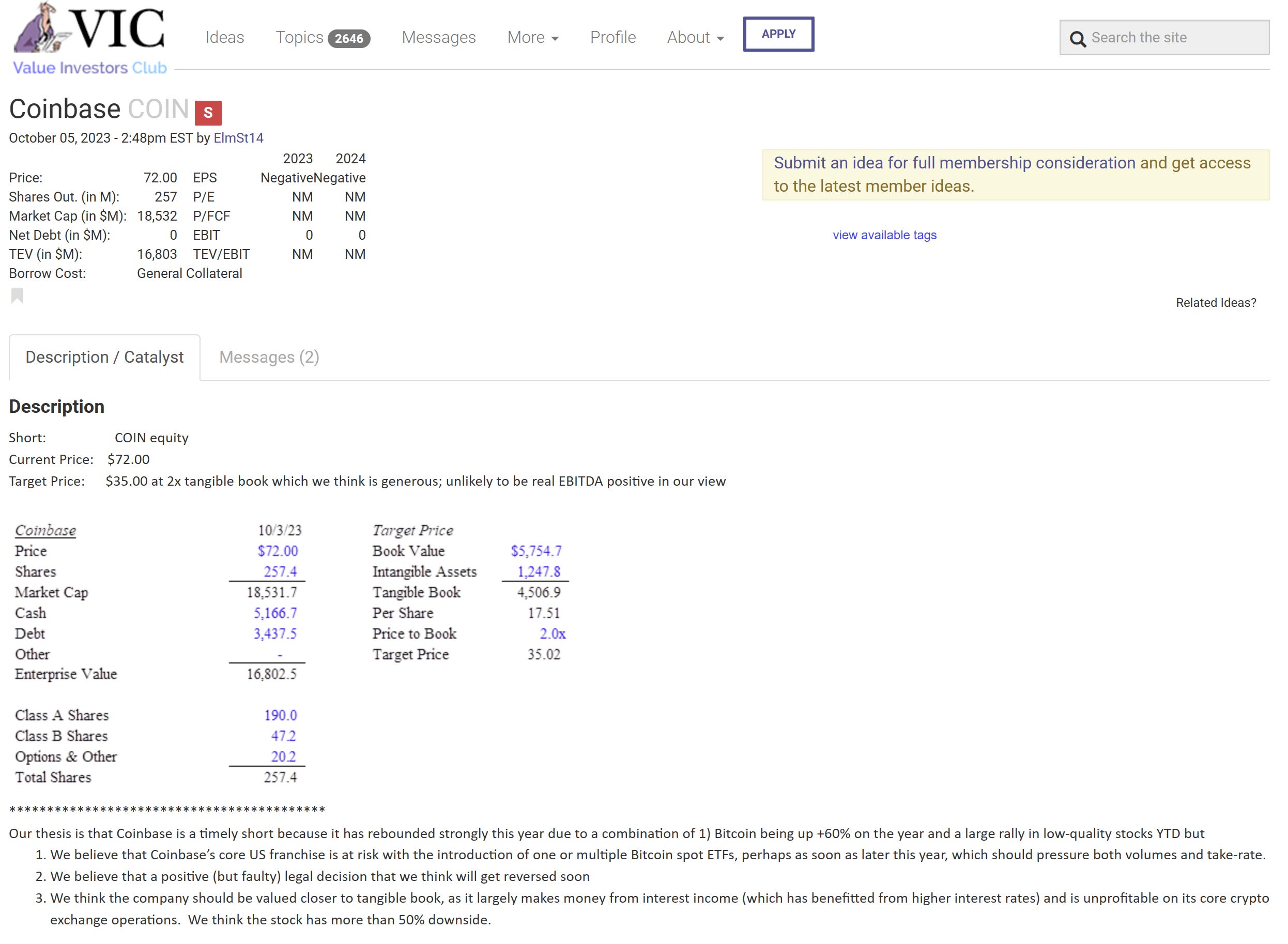

Short Idea: Coinbase Global (COIN, $23.0bn)

Cryptocurrency exchange Coinbase currently offers a timely short opportunity.

Company’s topline and profitability are likely to worsen with the expected introduction of spot bitcoin ETFs. After many years of fighting, a judge has recently ruled against SEC’s denial of these vehicles. Since then, dozens of funds, including the largest asset managers, have been planning to launch their spot bitcoin ETFs.

The potential introduction of multiple ETFs would pressure Coinbase consumer trading segment’s market share and take rates. This seems inevitable as spot bitcoin ETFs will boast much lower fees while providing ease of trading. Consumer trading segment currently accounts for nearly half of company’s total revenues. Coinbase will pick up substantial institutional volumes, however, those volumes will come with much lower take rates (0.02% vs 2.2% consumer take rates). So it seems that overall revenues will decline substantially.

There is another potential downside catalyst here. Recently, a judge ruled favorably to Coinbase in a lawsuit that is related to company’s ongoing litigation against SEC. But the ruling now seems likely to get overturned given evident flaws that have already been pointed out by another judge. If this occurs, Coinbase would likely give back the massive stock price gains made upon the initial ruling.

Coinbase is unprofitable and generates earnings primarily from interest income. So valuing the company on book value seems to be appropriate. At a generous 2x tangible book value multiple, the company would be worth $34/share or over 70% below the current share price.

Full COIN write-up on Value Investors Club (free guest account is required).

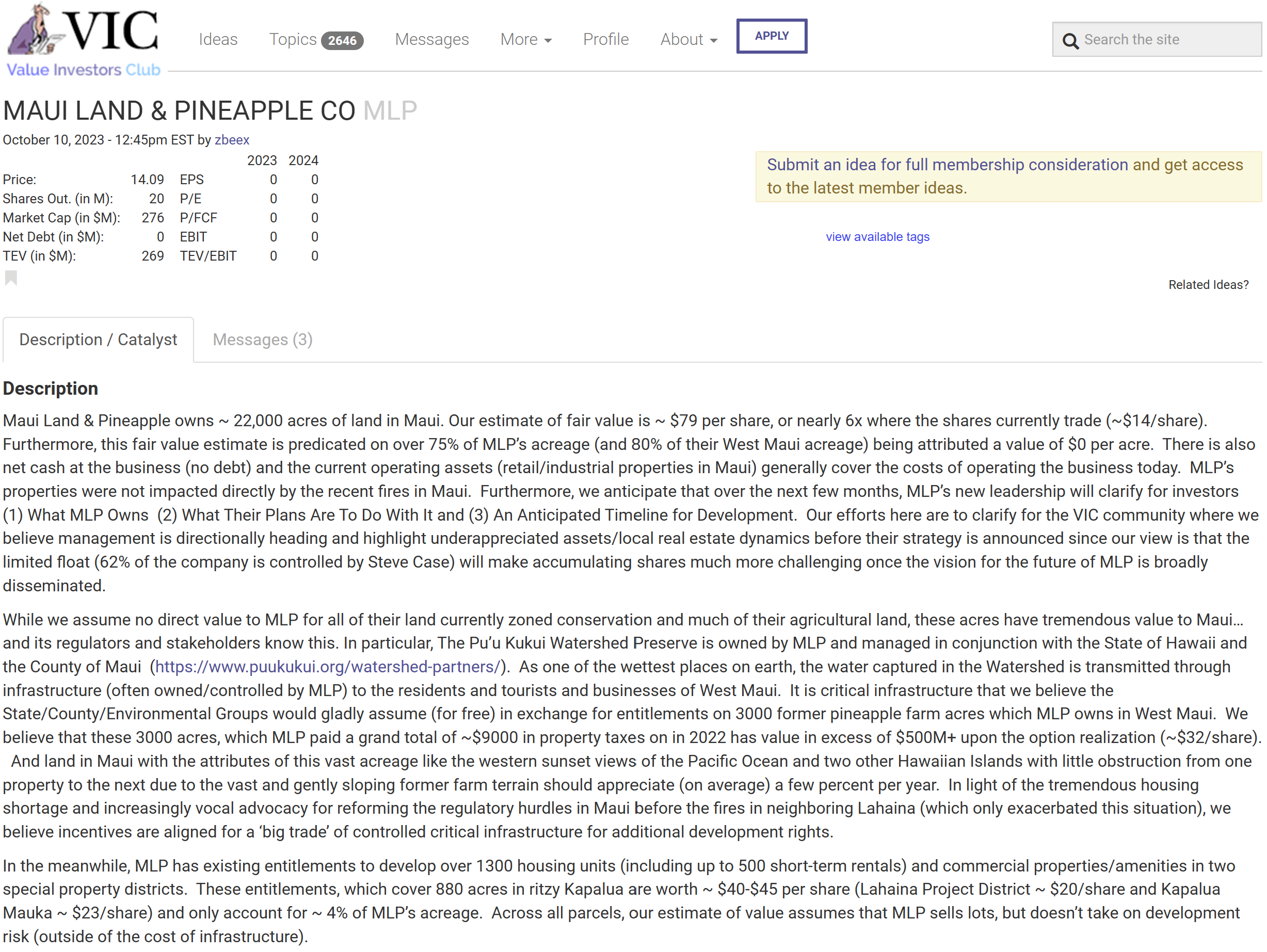

Maui Land & Pineapple Company (MLP, $293m)

Maui Land & Pineapple owns ~ 22,000 acres of land in the Hawaiian island of Maui. Company’s assets primarily comprise conservation zone land (75% of acreage), agricultural land (14%) and land with entitlements to develop housing/commercial properties (4%).

Maui Land & Pineapple is currently trading at a very wide discount to its estimated NAV. The existing entitlements alone are likely worth $40-$45/share vs the current price of $14.93/share. And there is likely to be significant additional value in the company’s conservation zone land and much of the agricultural land. Maui Land owns critical infrastructure within these areas. So it is possible that the Hawaii state could agree to assume this land in exchange for a large of number of entitlements in West Maui. These could potentially be worth an additional $32+/share.

The opportunity exists as company’s assets have historically been underappreciated by the market due to a prolonged restructuring period from 2009 until 2022. It was a result of poorly timed and structured real estate investments as well as modest operating cash flows.

However, Maui Land’s major shareholder/director Steve Case (owns 62%) has recently implemented a number of management changes. Over the last 18 months, Case has brought on an A-class management team with significant experience in real estate development. So it seems that the company is likely to finally proceed into the asset development stage. The stock is expected to re-rate once the asset development strategy is formally announced.

Full MLP write-up on Value Investors Club (free guest account is required).

Supremex (SXP:TO, C$97m)

Supremex is a Canadian company that manufactures envelopes and provides packaging services.

Supremex has suffered from the so-called Covid whiplash effect. Company’s customers over-ordered in 2021-2022 due to worries about product availability. Heightened demand, coupled with price increases, drove record profitability. The company generated C$1.09 in 2022 earnings per share compared to the current share price of C$3.75.

As supply chain concerns began to ease, Supremex's customers found themselves over-supplied and reduced their orders. This has negatively impacted Supremex's earnings, with the company generating C$0.87 in earnings per share over the last twelve months. Deteriorating profitability led to a massive sell-off, sending the stock down over 50% from its peak in Feb’23.

However, inventory de-stocking appears to be close to bottoming. Management has highlighted that conditions in both the envelope and packaging segments are improving. So it seems that revenues and earnings should rebound in the upcoming quarters.

The market typically values cyclical stocks at higher multiples during lows and lower multiples at peaks. If a fair multiple for Supremex on mid-cycle earnings is 8-10x, investors might expect shares to trade at 6-7x earnings at cyclical peaks and 12-13x earnings at the lows. And yet, Supremex shares are trading at just 6x annualized depressed Q3 earnings.

With the expected rebound in volumes in packaging and steady performance in envelopes, the company is likely to generate C$0.75 in earnings per share and C$1.01 in free cash flow per share by mid-2024.

Why does this opportunity exist? Aside from potential tax-loss selling, the mispricing might be explained by the company's return to stodgy mature manufacturer status after a moment of stardom.

Full SXP:TO write-up from Alluvial Capital.

Thanks! Again, some very interesting businesses. Maui Land & Pineapple Company (MLP) caught my attention, maybe because I love Hawaii and Maui☺️

Coinbasw long